US-JAPAN: Select Comments From Trump-Takaichi Press Spray

Mar-19 16:14

US President Donald Trump is meeting with Japanese Prime Minister Sanae Takaichi in the Oval Office....

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Large Mar'26 10Y Sale

Feb-17 16:13

- -15,344 TYH6 113-05.5, sell through 113-06 post time bid at 1054:22ET, DV01 $1.02M

- The 10Y contract trades 113-04.5 last (-1)

US STOCKS: Early Support Reversed: Energy & Materials Sectors Underperforming

Feb-17 16:09

- US equity indexes reversed early gains Tuesday, Energy and Materials sector shares leading the decline as crude oil and gold prices fell.

- Currently, the DJIA trades down 40.33 points (-0.08%) at 49461.55, S&P E-Mini Futures down 7.75 points (-0.11%) at 6842, Nasdaq down 43.3 points (-0.2%) at 22499.84.

- Crude prices retreated after Reuters reporting comments from Iranian Foreign Minister Abbas Araghchi following the conclusion of a second round of indirect nuclear talks with the US in Geneva, Switzerland. Araghchi said, "We've reached an understanding on main principles with the US."

- US$ bouncing to one week highs partially cited for the broad decline in Gold (in addition to a short term pause in Asia demand with China markets closed for the Lunar New Years holiday's this week) weighed on mining stocks in the first half.

- On the positive side, bank and insurance company shares buoyed the Financial sector for the most part, tempered by weaker financial services shares as Bitcoin fell more than 2.25% in early trade.

- Reminder, while the latest corporate earnings cycle is in it's final stretch (over 75% complete), a handful of companies are expected to report after today's close: Celanese Corp, Republic Services, Devon Energy Corp, Palo Alto Networks, Toll Brothers Inc, Caesars Entertainment and Kenvue Inc.

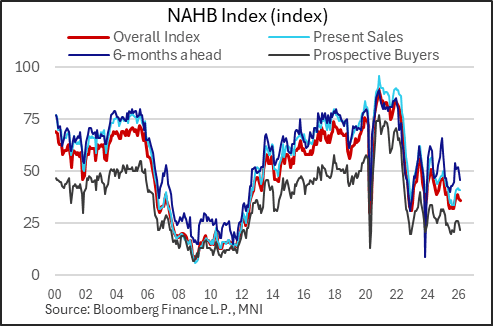

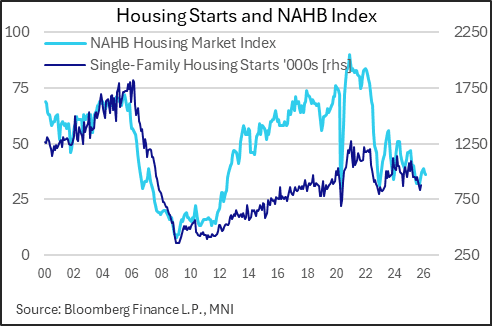

US DATA: Softening Homebuilder Sentiment Bodes Ill For Housing Start Recovery

Feb-17 16:05

For a second consecutive month in February, homebuilder sentiment as measured by the National Association of Homebuilders/Wells Fargo Housing Market Index (HMI) unexpectedly declined. The pullback to 36 from 37 prior (38 consensus) marked a 5-month low and the 2nd straight decline suggests any nascent momentum in homebuilder sentiment has halted (the NAHB had risen in each of the 4 months prior to January).

- The present sales gauge was steady at 41 but prospective buyer traffic dipped to a 5-month low 22 (24 prior, and around the all-time low), with future sales also dropping to a 5-month worst 46 (49 prior). There was no improvement in activity in any of the US regions (3 of 4 declined, with the South steady at zero).

- The NAHB characterizes the data as showing "Signs of Market Cooling", and points out that the latest survey shows "36% of builders cut prices in February, down from 40% in January. While this marks the lowest incidence of price-cutting since last May (34%), the average price reduction remains at 6%. The use of sales incentives was 65% in February, unchanged from January, and marking the 11th consecutive month this share has exceeded 60%."

- In other words, weak affordability amid high house prices and still-elevated mortgage rates, combined with still-high new home supply in terms of months of sales, continues to put pressure on builders to provide incentives.

- 2026 so far has thus seen a setback in confidence amid a residential real estate market that showed signs of thawing in the latter months of 2025, with sales picking up amid a dip in mortgage rates. The NAHB survey reflects single-family home construction sentiment and the pullback here suggests that housing starts/residential construction momentum will remain limited.

Related bullets

Related by topic

Geo-Political

Japan

US

Energy Data

Gasoil

Oil Positioning

OPEC

Gasoline

Diesel

US Natgas

TTF ICE

Asia LNG

Asia

Gas Positioning