UKRAINE: Russian & Ukrainian Negotiators In Davos For Talks w/US Officials

Earlier today, Reuters reported that Russian presidential envoy Kiril Dmitriev will attend the World Economic Forum annual meeting in Davos, Switzerland, to hold talks with senior US officials regarding a peace plan for Ukraine. US President Donald Trump is set to address the meeting on Wednesday, 21 January, and will travel with a 'large delegation' that could well include special envoy Steve Witkoff and his son-in-law Jared Kushner, the two individuals who have been most involved in the talks with Russian and Ukrainian negotiators on a prospective peace plan.

- Ukrainian President Volodymyr Zelenskyy is set to travel to Davos for talks as well, following the discussions in Miami, Florida, over the weekend involving Witkoff, Kushner, National Defence and Security Council (NSDC) Secretary Rustem Umerov, and the new head of Zelenskyy's office, Kyrylo Budanov. Following the talks, Umerov said, "We discussed the economic development and prosperity plan, as well as security guarantees for Ukraine, focusing on practical mechanisms for their implementation".

- Umerov said that the US-Ukraine talks would continue in Davos. At present, these talks will remain below leader level, with a Trump-Zelenskyy bilateral not on the agenda currently.

- The FT reports the 'Board of Peace' set up by Trump to oversee the Gaza ceasefire could be expanded to account for other conflicts/flashpoints, including Ukraine and Venezuela. However, concern about a widened mandate among Western and Arab leaders could scupper these plans. Invitations believed to have been sent to Russian President Vladimir Putin and Belarusian President Alexander Lukashenko could result in a boycott from European leaders.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (H6) Marked Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.160 @ 15:32 GMT Dec 19

- SUP 1: 95.120 - Low Dec 10

- SUP 2: 95.087 - 2.0% Lower Bollinger Band

- SUP 3: 94.276 - 1.0% 10-dma envelope

Aussie 10-yr futures remain well toward the bottom of the recent range, having taken out all major support levels in the process. With 95.275 cleared, prices are pushing to new contract lows, opening vol-band support through 95.087 and into 94.276. Any recoveries need to break back above 95.900 to signal near-term bullish traction.

AUDUSD TECHS: Corrective Phase Still In Play

- RES 4: 0.6759 High Oct 11 ‘24

- RES 3: 0.6723 High Oct 21 ‘24

- RES 2: 0.6707 High Sep 17 and a key resistance

- RES 1: 0.6661/86 High Dec 16 / 10

- PRICE: 0.6608 @ 15:56 GMT Dec 19

- SUP 1: 0.6593 Low Dec 18

- SUP 2: 0.6566 50-day EMA

- SUP 3: 0.6517 Low Nov 27

- SUP 4: 0.6466/21 Low Nov 26 / 21

The trend condition in AUDUSD remains bullish and the latest pullback appears corrective. The move down is allowing a recent overbought condition to unwind. Support at the 20-day EMA, at 0.6598, has been pierced. The 50-day average is at 0.6566. The area between the two averages represents a key short-term support zone. A resumption of gains would refocus attention on key resistance at 0.6707, the Sep 17 high and bull trigger.

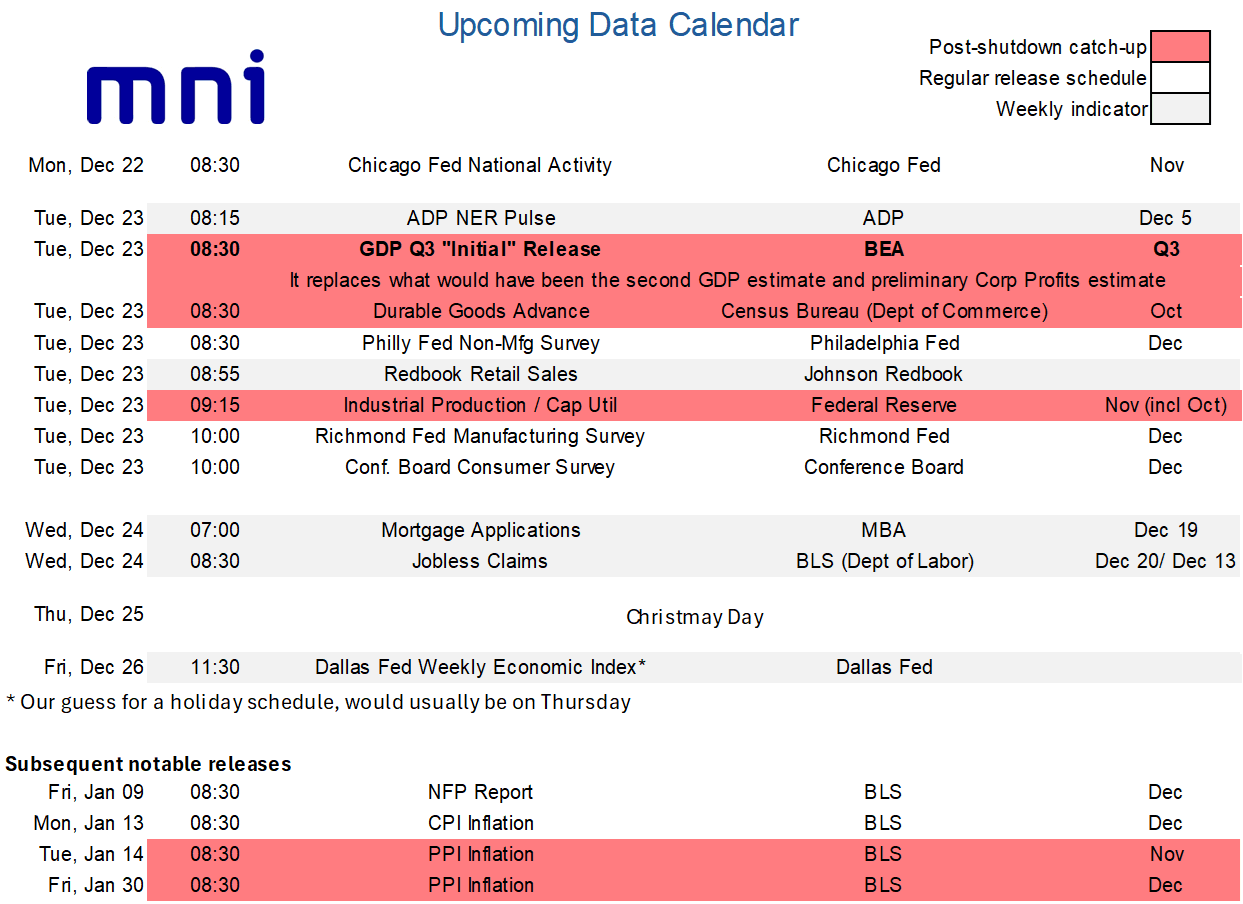

LOOK AHEAD: US Macro Week Ahead: Long-Awaited Q3 GDP Plus Labor Updates

- The week ahead sees a slimmed down data schedule after a particularly busy few weeks, including distorted NFP and CPI reports in the week just gone. There are still some important releases though, with the highlight being the long-awaited “initial” Q3 GDP release on Tuesday.

- This report will replace what would have been the second GDP and the preliminary corporate profits estimates, with the extended tracking window of the Atlanta Fed’s GDPNow pointing to strong real GDP growth of 3.5% annualized after an average 1.6% in 1H25 (-0.65% in Q1 before 3.84% in Q2).

- Expect continued close attention on private demand, best seen by Powell’s preferred PDFP category, which is currently tracking at ~2.4% annualized for similar to the 2.4% averaged in 1H25 (1.9% Q1 before 2.9% in Q2).

- Tuesday also sees updates for the weekly ADP tracker in the four weeks up to Dec 5, getting closer to the reference period for the monthly report, after last week’s further improvement. It’s followed by useful updates for Q4 GDP tracking with durable goods for October and industrial production for both October and November, before the Conference Board consumer survey for December with its closely watched labor differential having stalled at subdued levels but not deteriorated further since September.

- Note as well that Wednesday then sees weekly jobless claims a day early ahead of Christmas Day, with continuing claims capturing the December payrolls reference period. There is currently minimal Fedspeak scheduled and we suspect this will remain the case ahead of Christmas, likely confined to media appearances if any.