RUSSIA: MNI CBR Preview: October 2024

Oct-24 10:16

- The CBR is expected to hike the key rate by 100bps to 20%, with the recent surge in household inflation expectations and tightness in the labour market leaving the Bank little to no room to pause.

- Meanwhile, early signs of slower price increases and more moderate economic activity data will likely limit the size of the hike to just 100bps.

- As per a Bloomberg survey, 9 out of 13 analysts expect a 100bp hike to be delivered (2 expect no change and 2 expect a larger hike).

See the full preview, with a summary of sell-side analyst views, here.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: Slovenia 3.00% Mar-34 SlovGB tap: Update

Sep-24 10:15

- Guidance revised to MS+60bp (was MS+62bps area)

- Size: EUR benchmark size tap increase

- Books in excess of E2.5bln (inc E150mln JLM interest)

- Settlement Date: 1 October 2024 (T+5)

- Joint Bookrunners: Barclays (B&D), Deutsche Bank, Erste Group, J.P. Morgan

- ISIN: SI0002104576

- Timing: Books open, today's business

From market source

EGB SYNDICATION: Spain 12-year ObliEi: Final terms

Sep-24 10:10

- Size set at E4bln (the middle of the E3-5bln range MNI had expected)

- Books closed in excess of E51bln pre-rec (inc E4.7bln JLM interest)

- Spread set earlier at 0.70% Nov-33 ObliEi RY + 22bps

- Guidance was 0.70% Nov-33 ObliEi RY + 25bps area then +23bps +/-1bp WPIR

- Maturity: 30-Nov-2036

- Settlement: 01-Oct-2024 (T+5)

- Coupon: Fixed, annual ACT/ACT, full first on 30-Nov-2024

- ISIN: ES0000012O18

- Bookrunners: CITI / CACIB / GSBE / MS (B&D/DM) / SANTAN / SGCIB

- Timing: Books closed - allocations and pricing later today

From market source

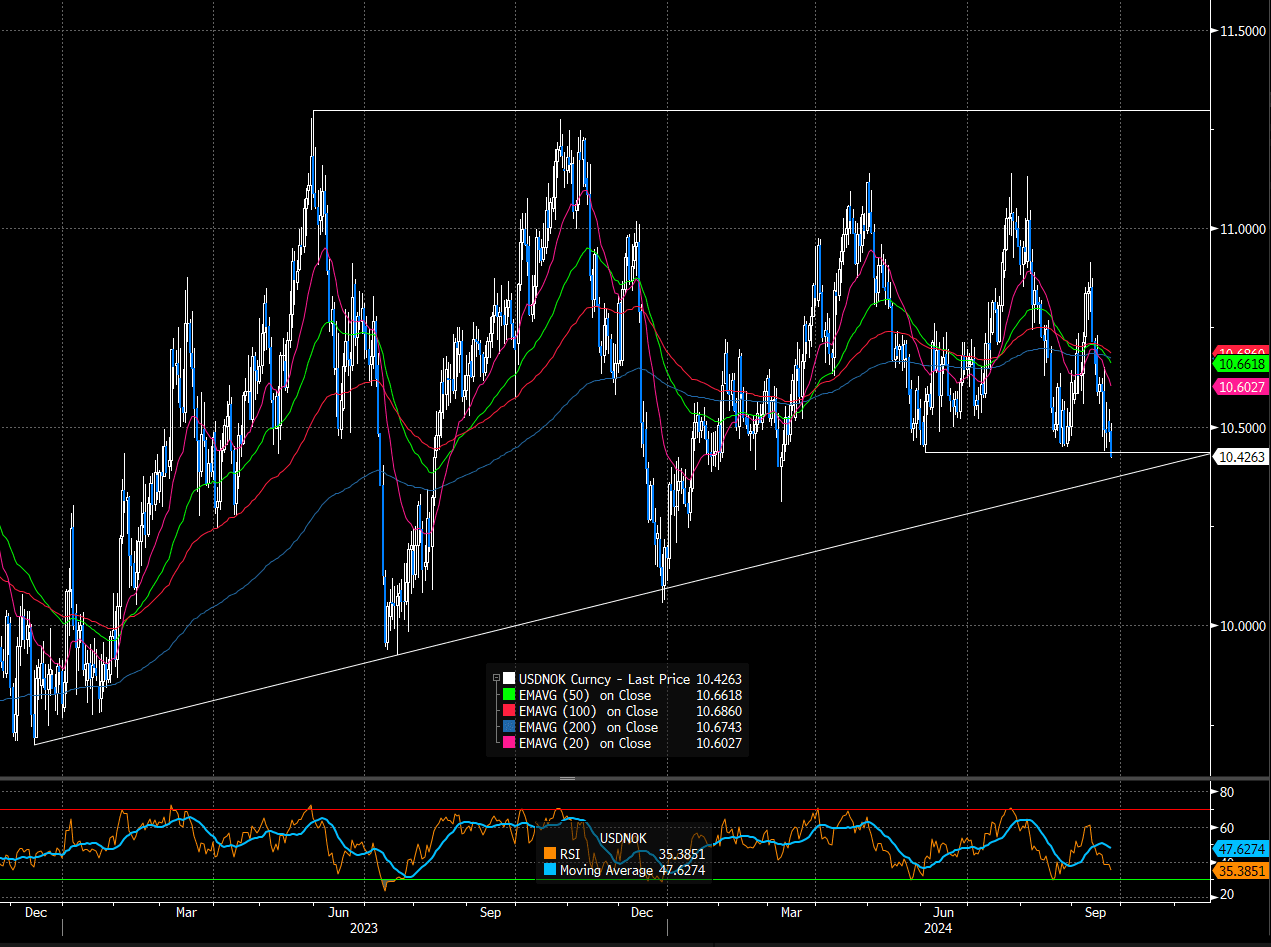

NOK: USDNOK Pierces Key June 4 Support

Sep-24 10:10

USDNOK has pierced key support at 10.4354 (Jun 4 low), as the krone finds support from China stimulus-driven bids in equities and crude oil. Today’s price action extends the latest leg of NOK strength following last week’s Norges Bank decision.

- USDNOK has fallen ~4.5% from the Sep 11 high, and a sustained breach of the Jun 4 support would strengthen a bearish theme.

- This would expose trendline support drawn from the December 2022 low.

- EURNOK has similarly tested the Aug 30 low at 11.6133, currently 0.35% lower today.

- Domestic developments take somewhat of a backseat this week following last Thursday’s Norges Bank decision, where the rate path/guidance re-affirmed that rates were likely to stay on hold until early 2025.

- Unemployment data is due on Thursday and Friday this week, but these are not usually market movers.

- This will leave NOK crosses sensitive to movements in global risk sentiment and US data, including Friday’s PCE report.