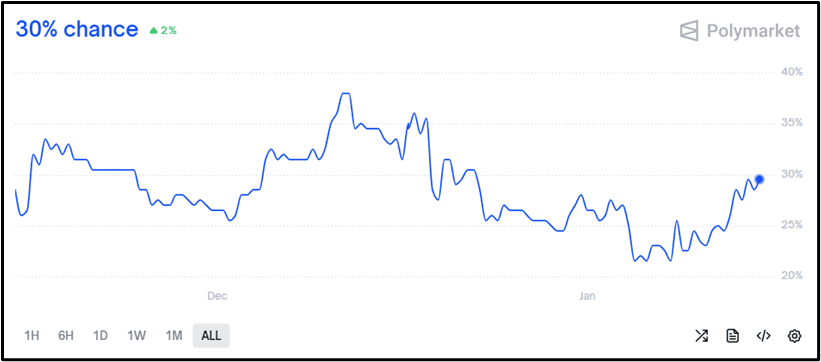

US: Risk Of Partial Govt Shutdown Ticks Up, But Impact On Markets Limited

The Senate is expected to pass a 3-bill appropriations minibus today, taking the total number of completed FY26 funding bills to 6 (out of 12). Senate appropriators are expected to release another package over the weekend, covering Defense, Transportation-HUD and Labor-HHS-Education.

- Politico notes Senate Majority Leader John Thune (R-SD) said that senators are “keeping their options open for how to process the six remaining funding bills once they return from next week’s recess. But senators... [may] ...need to merge all the leftover bills into one unless they can cut a deal to dramatically speed up the chamber’s work.”

- Despite uncharacteristically bipartisan progress on appropriations, a major confrontation is building over the Department of Homeland Security bill, which oversees Immigration and Customs Enforcement (ICE).

- While ICE is already funded with USD$170 billion via the GOP’s ‘One Big Beautiful Bill’, Democrats are resistant to authorising the DHS bill without guardrails to govern the conduct of ICE agents, for example, bodycams and removing facemasks.

- In light of the DHS standoff, the risk of a partial government shutdown on January 31 has ticked up to 30%. A solution to the standoff could be a short-term funding measure to keep the lights on at DHS without increasing funding. If a shutdown does take place, it would likely be limited to DHS and have little impact on markets as funding for the remaining agencies appears set to be competed ahead of the deadline.

Figure 1: Government Shutdown by January 31

Source: Polymarket

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

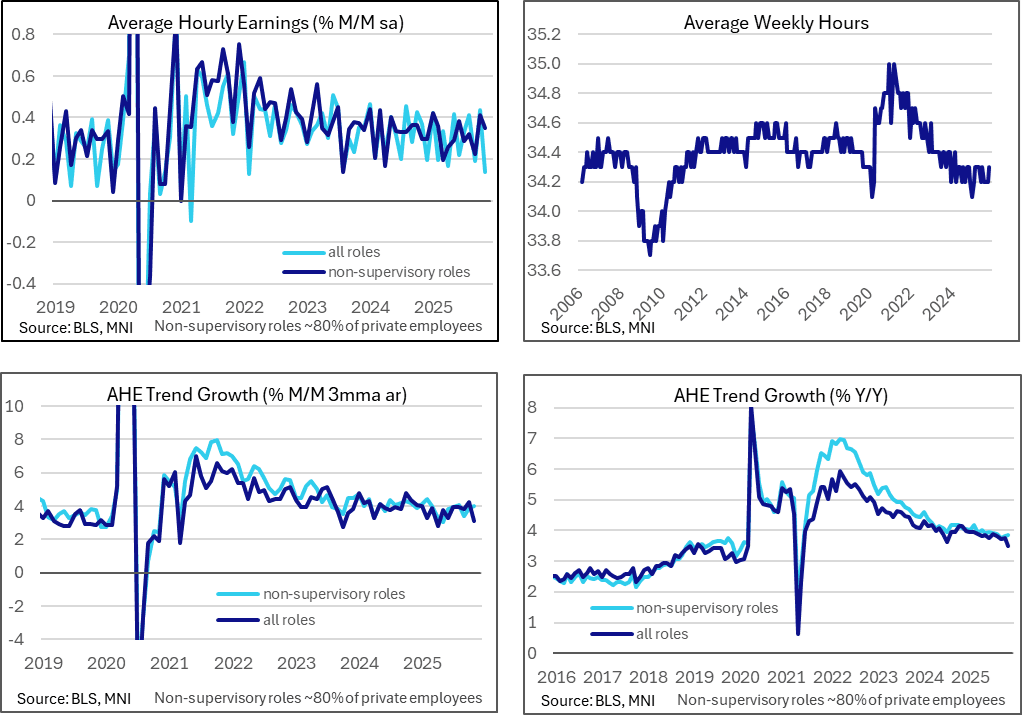

US DATA: AHE A Mixed Bag Rather Than A Clear Miss In Two-Month Update

The two months of average hourly earnings data were a mixed bag rather than the outright weakness that the headlines suggest, with non-supervisory employee wage growth running firmer and hours worked also increasing in November.

- Overall AHE growth of 0.14% M/M in November was clearly softer than the 0.3% M/M widely expected although it was countered by a stronger than expected 0.44% M/M in Oct (we had seen limited estimates with a median 0.3 but with risks skewed lower). Still, September was also revised lower to 0.19% M/M vs the previously estimated 0.25% M/M.

- The combination meant the Y/Y rate surprised lower, with 3.51% Y/Y (cons 3.6) after 3.75% in Oct for a fresh low since May 2021.

- Non-supervisory earnings painted a stronger picture however, at 0.35% M/M in Nov after 0.41% M/M in Oct and only a marginally downward revised 0.22% (initial 0.25%) in Sep.

- This typically less volatile category that captures about 80% of employees accelerated to a three-month high of 3.86% Y/Y from 3.81%.

- Another factor that makes the headline AHE figures look less weak is that average hours worked surprised higher in November at 34.3 (cons 34.2) after the 34.2 was unchanged from the previously reported 34.2 in September. This would mechanically have biased average hourly earnings of salaried employees lower in the month.

MNI: US REDBOOK: DEC STORE SALES +5.9% V YR AGO MO

- MNI: US REDBOOK: DEC STORE SALES +5.9% V YR AGO MO

- US REDBOOK: STORE SALES +6.2% WK ENDED DEC 13 V YR AGO WK

STIR: Dovish Reaction To NFPs Counters ADP Move, Despite Some Limiting Caveats

Initial dovish reaction to the uptick in the unemployment rate and soft AHE readings countered by the fact that the unrounded unemployment figure (4.564%) was a ‘low’ 4.6%.

- Elsewhere, the firmer-than-expected headline NFP reading and caution after the recent BLS notice flagging changes to statistical weights for the November household survey estimates, which will result in November labor force estimates having "slightly higher" variances than usual, further temper the initial market reaction.

- A firmer-than-expected control group reading on the retail sales release may also be factoring in.

- FOMC-dated OIS still prices ~6bp of easing for January, little changed vs. pre-NFP levels. 58bp of easing is priced through ’26 on the whole after a couple of spikes above 60bp during the initial reaction to NFPs.

- SOFR futures now flat to +2.0 through the blues. Implied terminal rate pricing moves to ~3.115% vs. 3.135% ahead of the NFP release, briefly hitting 3.035% in the wake of the data.

- The modest hawkish move that followed the weekly ADP employment print has been reversed.