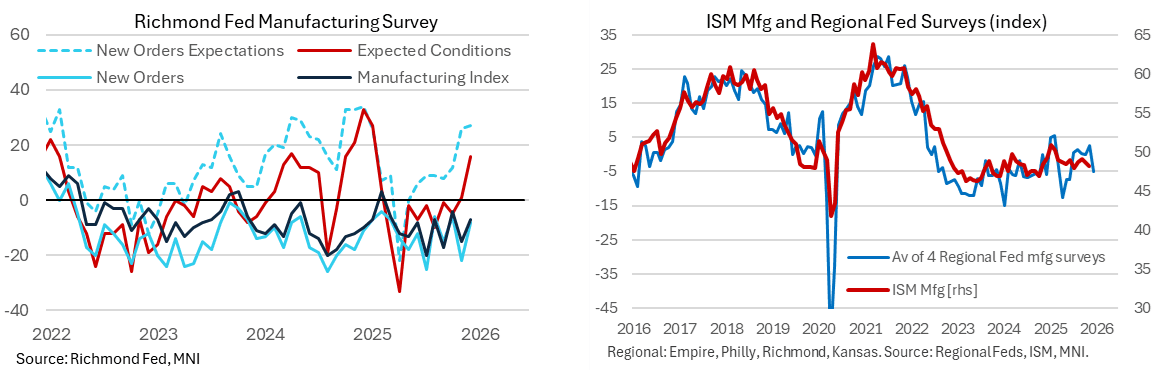

US DATA: Richmond Manufacturers Expect Solid Improvement In Local Conditions

The Richmond Fed manufacturing index saw a relative improvement in December as it bucked the trend from three other regional Fed surveys which had all deteriorated. A sideways and noisy recent pattern makes it hard to get a sense of trend in current activity although six-month ahead expectations of local business conditions saw a solid improvement after prior increases in new orders and shipments.

- The Richmond Fed manufacturing index fared a little better than expected in December, rising to -7 (Bloomberg cons -10) after -15.

- It broadly continued a recent run of oscillating between -4 and -20 in 2H25 in patterns that have largely been seen in new orders albeit with some greater volatility (latest -8 after -22).

- Six-month ahead expectations of local business conditions offered a stronger take though, rising to 16 after the 1 in November was its first positive since February.

- This improvement follows a previous increase for new orders (27 after 26 in Nov and 12 in Oct) and shipments (28 and 25 in Nov and 13 in Oct) which was largely cemented this month, although the number of employees index also saw a reasonable increase this month (8 after -1 in Nov and 2 in Oct).

- Back to current indicators, the sequential increase goes against deterioration seen in the other regional Fed surveys with Empire at -3.9 after 18.7, Philly at -10.2 after -1.7 and Kansas at 1 after 8.

- The average of these four regional Fed surveys fell to -5.0 in Dec from 2.5 for its lowest since June, pointing to downside momentum risk to ISM manufacturing (released Jan 5). We’ll revert on the latest for manufacturing indicators after Dallas (Dec 29) and the MNI Chicago PMI (Dec 30).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RATINGS: Moody's Upgrades Italy To Baa2 From Baa3, Still A Notch Below Others

The Moody's upgrade to Italy's credit rating announced late Friday was the first from the agency since 2002 but shouldn't be considered a major surprise. Among the 3 major ratings agencies, Moody's had the lowest rating on Italy - by two notches (Fitch and S&P both BBB+).

- So this upgrade to Baa2 from Baa3 represents something of a closing of that gap rather than a major breakthrough for Italy.

- From the release:

- "The rating upgrade reflects a consistent track-record of political and policy stability which enhances the effectiveness of economic and fiscal reforms and investment implemented under the National Recovery and Resilience Plan (NRRP). It also points to prospects of further policy actions supporting growth and fiscal consolidation beyond the plan's deadline in August 2026. As a result, we expect that Italy's high government debt burden will gradually decline from 2027 onwards."

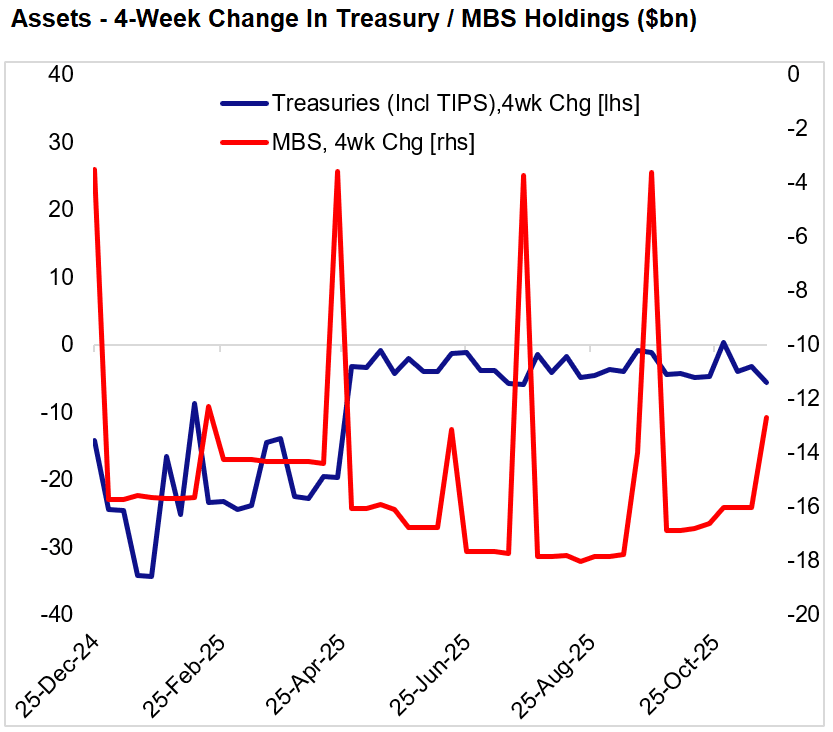

FED: Heading Into Its Final Weeks, QT Pace Remains At $20B/Month (2/2)

On the asset side of the Fed balance sheet, we saw a $25B drop in assets, of which just $2B could be attributed to QT in one of its final weeks (ends Dec 1).

- Instead it was a $6B drop in dealer repo operations vs a week earlier, and $17B in "other" areas that aren't related directly to monetary policy and typically don't have any significant impact on the size of the balance sheet (such changes are largely due to items such as bank premises, accrued interest, and other accounts receivable.)

- Discount window takeup edged up $0.3B to $6.1B but remains relatively low.

- QT has totaled just under $21B over the last month, around the expected pace, though as noted this will flatline in December with a pickup in net bills as MBS proceeds are rolled over into T-bills.

LOOK AHEAD: US Week Ahead: Retail Sales, PPI & Claims Headline Thanksgiving Week

A Thanksgiving-condensed week sees data highlights from delayed retail sales and PPI reports for September on Tuesday (Nov 25) before a Wednesday release for weekly jobless claims (Nov 26). Aside, the Fed’s Beige Book should also offer another important update on Wednesday for latest liaison reporting, with no Fedspeak currently scheduled around the holiday and the FOMC media blackout due to start on Saturday, Nov 29.

- As we regularly comment in this weekly publication, Redbook and Chicago Fed CARTS indicators point to solid nominal growth in retail sales, something broadly reflected in analyst consensus for the release.

- PPI inflation will offer a useful albeit not overly timely update on input cost pressures.

- Jobless claims will be watched particularly closely, both for latest initial claims for signs of layoffs and a notable update for continuing claims. The latter covers the payrolls reference period for November and will be an important reference point for FOMC members trying to get a sense of latest unemployment rate clues with the next payrolls reports coming after the Dec 9-10 FOMC decision (going into it with this week’s 0.12bp rise to 4.44% back in September).