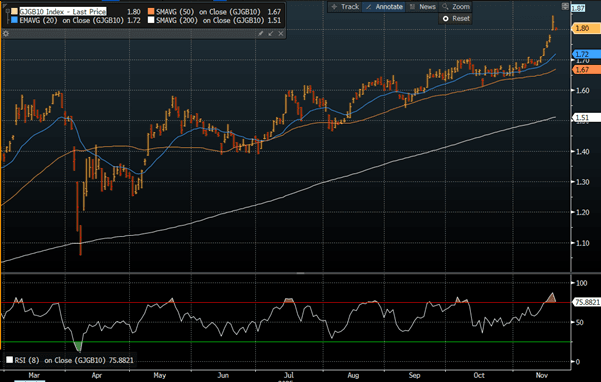

JGBS: Richer After National CPI Data, Core CPI Back To 3%

In Tokyo morning trade, JGB futures are stronger, +21 compared to settlement levels.

- Japan’s annual core consumer inflation rose to 3.0% y/y (first time in three months) in October from 2.9% in September, in line with expectations, driven by higher prices for household durable goods, although food prices excluding perishables eased.

- Underlying inflation, measured by the core-core CPI (excluding fresh food and energy), rose 3.1% y/y in October, edging up from 3.0% in September.

- S&P Global PMIs (P) for November have printed: Manufacturing index rises to 48.8 from 48.2 in Oct.; Services index unchanged at 53.1 from Oct.; and Composite index rises to 52 from 51.5 in Oct.

- Japan's FinMin Katayama has stepped up rhetoric around yen weakness, noting that intervention is an option. USD/JPY is modestly lower post the comments. Session lows rest at 157.20, but we now sit slightly higher, 157.35. Earlier highs were at 157.53.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday’s risk-off induced rally.

- Cash JGBs are flat to 2bps richer across benchmarks, with the 7-10-year zone leading. The benchmark 10-year yield is 2.1bps lower at 1.803% versus the cycle high of 1.84%, set yesterday.

- Swap rates are little changed.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JAPAN DATA: Exports Up, Aided By Tech Shipments, Unlikely To Shift BoJ Outlook

Japan headline exports were close to market forecasts, rising 4.2%y/y (+4.4% was forecast and -0.1% was the Aug outcome). Imports were stronger than expected, +3.3%y/y (+0.6% was forecast and -5.2% was prior), which left the trade deficit positions weaker than the consensus estimates. For export growth it was the first y/y rise since April of this year, which will be welcomed by the authorities. The BoJ is watching fallout from higher US tariff levels (albeit that were lowered in Sep) on export growth. Today's outcome is unlikely to shift near term thinking around rate hike timing.

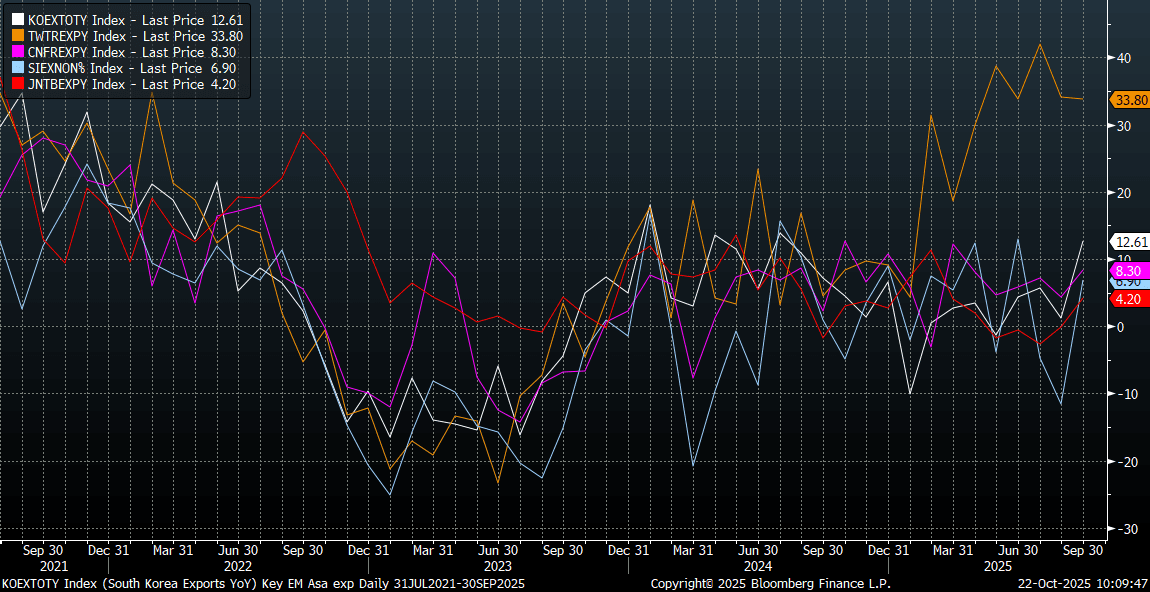

- The chart below plots export growth for key externally focused Asian economies (Japan is the red line on the chart). Japan's rebound in Sep brings is consistent with the trends for most other parts of the region, although Taiwan, the orange line, remains the standout.

- Tech/semiconductor exports were a source of strength, up 12.6%. Car exports fell 0.6%, with exports to the US fell by 13.3% (car exports to the US were off 24.2%y/y, after a 28.4% decline in Aug). Exports to China and the EU were both above 5%y/y, with tech related demand in Asia prominent.

- The trade deficit position persisted, but were around recent levels.

Fig 1: Export Growth For Key Asian Economies

Source: Bloomberg Finance L.P./MNI

GOLD: Gold & Silver Correction Continuing In APAC Session, Breached 20-d EMA

Profit taking in gold and silver begun on Tuesday has continued in Wednesday’s APAC trading with prices down 1.8% to $4052.3 and 1.0% to $48.21 respectively. The USD BBDXY is little changed but the slight decline appears to have provided a floor to the metals. Traders have been long, with the extent unclear due to the lack of CFTC positioning data due to the US government shutdown, and appear to be normalising those positions as both metals are in overbought territory.

- Gold prices fell to a low of $4004.26 as Asian markets opened, below support at $4021.6, 20-day EMA. It is currently trading above this level but another breach would open $3819.6, 2 October low. The correction is unwinding the overbought position.

- Silver reached a trough earlier at $47.550 below support at the 20-day EMA of $49.089. It continues to trade below this level opening up the 50-day EMA at $44.996. The market is smaller than gold which can exacerbate moves.

US TSYS: UST Yields Lower Again After Overnight Lead

TYZ5 has opened the Asia trading day at 113-24+ with limited price action at the open whilst bonds continued to grind lower in yield across longer maturities. If short end yields are most reactive to monetary policy and longer to growth, the bond markets appears to be suggesting that the government shutdown will trim growth expectations the longer it goes on.

- The US 2-Yr is barely to get off where it started at 3.45%.

- The US 5-Yr has moved lower by -1bp to reach 3.55%

- The 10-Yr has consolidated below 4.00%, rallying again overnight and is down a further 1bp to reach 3.95% in line with October 24 yield levels.

- The 30-Yr continues to outperform rallying -2.5bps overnight to reach 4.544%. The likely next inflection point could be the April lows of 4.40%.

With both the KOSPI and NIKKEI opening lower, markets will watch for signs of a pullback in risk sentiment given two very strong days this week already.