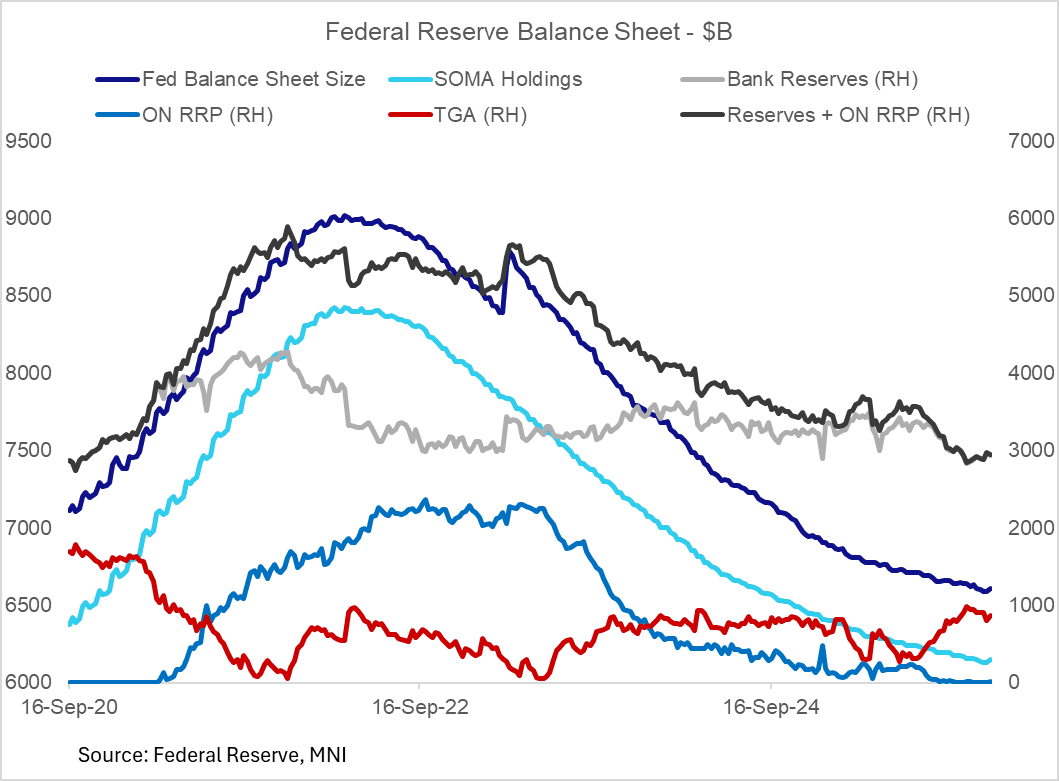

FED: Reserves + ON RRP Remain Sub-$3T In Latest Week As TGA Picks Up (1/2)

Dec-19 19:53

Reserves slipped back slightly in the week to Wednesday December 17, per the Fed's latest H.4.1 release.

- The $40B weekly drop combined with continued limited takeup in overnight reverse repo kept the reserves level below $3T for a 10th consecutive week.

- Downside pressure on reserves was applied by a $56B increase in the Treasury General Account, coinciding with a tax payment deadline on Dec 15. The TGA level of around $860B is close to Treasury's medium-term targeted level.

- Reserves are up $16B in the last month (during which time the Fed has acknowledged it is at a level more consistent with "ample" rather than the previous "abundant" conditions), with the TGA down $39B.

- Overall Fed liabilities are due to start picking up in coming months as reserve management purchases pick up.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

COMMODITIES: Crude Falls, Gold Pares Gains Amid USD Rally

Nov-19 19:53

- WTI has lost ground today as the market digests signs of renewed efforts by the US to strike a Ukraine peace deal, coupled with an unexpected rise in US crude stocks last week.

- WTI Dec 25 is down by 2.1% at $59.4/bbl.

- Axios reported that the US has put together a new 28-point Ukraine peace plan after closed US-Russia discussions.

- Meanwhile, Reuters said that the US-drafted framework to end the war with Russia proposes Kyiv giving up territory and some weapons.

- From a technical perspective, WTI futures are trading in a range. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend.

- Resistance to watch is $61.84, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction.

- Meanwhile, spot gold has given up earlier gains amid a rally in the dollar as the FOMC minutes suggested limited appetite for a follow-up rate cut in December.

- Gold is currently up by just 0.2% at $4,075/oz, having traded as high as $4,132.86 earlier in the session.

- Recent gains in gold suggest that the correction between Oct 20 and 28 is over. With the metal retracing off last week’s high, the key support to watch lies at the 50-day EMA, at $3,942.7. The short-term bull trigger has been defined at $4,245.23, the Nov 13 high.

FED: FOMC Minutes: Restrictiveness Debate Simmering

Nov-19 19:51

A few other notes of interest from the October FOMC meeting minutes:

- Restrictiveness Debate Continues: The passage on current policy restrictiveness in the October minutes repeats the September's edition in noting that "participants expressed a range of views about the degree to which the current stance of monetary policy was restrictive." But at the latest meeting it seems that caution was rising over the degree of restrictiveness, with "some" seeing policy as still restrictive even after the October cut, but also "some" seeing signs that the policy wasn't "clearly restrictive" even before the eventual rate cut.

- The October minutes say: "Some participants assessed that the Committee's policy stance would be restrictive even after a potential 1/4 percentage point reduction in the policy rate at this meeting. By contrast, some participants pointed to the resilience of economic activity, supportive financial conditions, or estimates of short-term real interest rates as indicating that the stance of monetary policy was not clearly restrictive.")

- That shows a subtle but important evolution since the September minutes which showed a majority that saw policy as still restrictive after the September cut: "Most judged that it likely would be appropriate to ease policy further over the remainder of this year. Some participants noted that, by several measures, financial conditions suggested that monetary policy may not be particularly restrictive, which they judged as warranting a cautious approach in the consideration of future policy changes."

- Staff Forecasts Remain Constructive: The Fed staff didn't show much concern over the impact of the federal government shutdown ("The government shutdown was expected to reduce GDP growth for as long as it continued, with a corresponding boost to growth once the government reopened and government production and purchases returned to normal levels"), while the economic outlook remained constructive: "GDP growth after 2025 was expected to remain above potential until 2028 ... the unemployment rate was expected to decline gradually after this year before flattening out at a level slightly below the staff's estimate of the natural rate of unemployment. The staff's inflation forecast was broadly similar to the one prepared for the September meeting, with tariff increases expected to put upward pressure on inflation in 2025 and 2026. Thereafter, inflation was projected to return to its previous disinflationary trend." That said, GDP and labor force risks were seen to the upside with inflation risks to the upside.

- Growing concerns over inflation by some, but greater relief for others. October: "Several participants observed that, setting aside their estimates of tariff effects, inflation was close to the Committee's target. Many participants, however, remarked that overall inflation had been above target for some time and had shown little sign of returning sustainably to the 2 percent objective in a timely manner. September: "A couple of participants expressed the view that, excluding the effects of this year's tariff increases, inflation would be close to target. A few other participants, however, emphasized that progress of inflation toward the Committee's 2 percent objective had stalled, even excluding the effects of this year's tariff increases."

- GDP vs Payrolls: In October, "Many" participants saw upside risks to their inflation outlooks; "many" also "observed that the divergence between solid economic growth and weak job creation created a particularly challenging environment for policy decisions".

- PCE Estimates In: the Fed estimates September PCE at 2.8% Y/Y based on CPI data for the month (PPI and import price data that goes into that calculation was postponed but will be published in the coming weeks).

PIPELINE: Corporate Bond Update: $6.35B to Price Wednesday

Nov-19 19:47

- Date $MM Issuer (Priced *, Launch #)

- 11/19 $2B #Baxter $300M 3Y +90, $700M 5Y +125, $1B 10Y +155

- 11/19 $1.1B #Bangkok Bank $500M 5Y +82, $600M 10Y +97

- 11/19 $1B #EOG Resources $750M +5Y +73, $250M 30Y tap +105

- 11/19 $500M #VSP Optical WNG 10Y +135

- 11/19 $500M #Element Fleet 5Y +95

- 11/19 $750M #SMBC Aviation 10Y +115

- 11/19 $500M #FIBRA Prologis WNG 10Y +145

- 11/19 $Benchmark First Abu Dhabi Bank (FAB) investor calls

Trending Top

Mar-27 20:13