US DATA: Rental Inflation Easing Below Pre-Pandemic Trend Drives Dovish Reaction

Dec-11 14:09

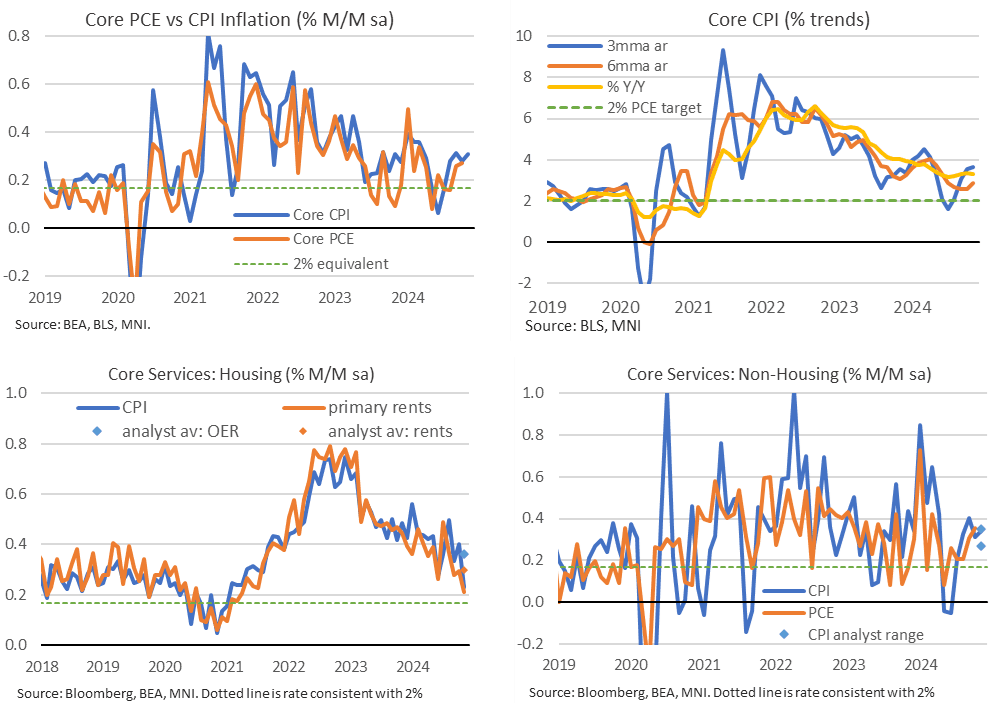

- Core CPI inflation was a little stronger than expected in November at 0.31% M/M (cons 0.28) as it extended its oscillation between 0.28-0.31% M/M to four months now.

- It pushed the three-month run rate to 3.66% annualized (highest since April) having bottomed at 1.6% in July, the six-month rate to 2.9% annualized (highest since June) from October’s recent low of 2.6% and the Y/Y stabilized at 3.32%.

- Broadly speaking, the surprise strength was concentrated in core goods (0.31% M/M vs 0.1% expected) - notable ahead of potential tariffs, as detailed above - whilst surprise weakness was seen in core services (0.28% vs 0.32% expected).

- Core services would have been much weaker were it not for surprise lodging strength (3.2% M/M vs cons -0.1%), which played a large role in pushing supercore (core services ex OER & primary rents, not ex broader shelter which includes lodging) to the top end of expectations at 0.34% M/M after 0.31% M/M.

- OER and primary rents inflation of 0.23% and 0.21% M/M saw 45- and 43-month lows respectively. Importantly, the weighted average of 0.23% M/M is the first month this cycle that monthly rental inflation has been below its pre-pandemic average of 0.27% (it last tied with this 0.27% increase back in June before surprisingly surging to 0.47% M/M in Aug).

- The moderation in these rent components is significant. Housing has previously appeared to us to be the main stumbling block in the return to the inflation target. With the labor market increasingly looking like it won’t be a source of inflationary pressure in the near-term (even more so after yesterday’s productivity revisions), supercore inflation should start to take less precedence.

- However, clouding this dovish take is that some surprisingly soft core services items were in CPI-specific categories such as airfares (0.4% M/M vs average estimate of 1.1%) and auto insurance (0.1% M/M vs 0.7%). PPI tomorrow will play an important role in latest core PCE implications, more on that to follow.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SLOVAKIA AUCTION PREVIEW: On offer next week

Nov-11 14:03

Slovakia has announced it will be looking to sell the following SlovGBs at its auction next Monday, November 18:

- the 3.00% Feb-28 SlovGB (ISIN: SK4000024683)

- the 3.625% Jun-33 SlovGB (ISIN: SK4000023230)

- the 3.75% Mar-34 SlovGB (ISIN: SK4000024865)

- the 0.375% Apr-36 SlovGB (ISIN: SK4000018958)

UK DATA: MNI UK Labour Market Preview: November 2024 Release

Nov-11 13:58

- After the CPI data and possibly the PMI data, this release is still up there as one of the most important UK domestic releases of the month.

- We still place most emphasis on private sector regular AWE. The November latest MPR forecast looks for this metric to come in at 4.75%Y/Y in the 3-months to September (but rounding up to 4.8% to 1dp), a little below the 4.83%Y/Y forecast it made 3-months prior) and August print of 4.81%, but a little above the 4.7% MNI median.

- It appears to us as though there are some risks that the 3-month number rounds up to 4.8%Y/Y here – or at least that seems more likely than a 4.6%Y/Y print in the 3-months to September.

- The unemployment rate is forecast at 4.17% by the BOE (4.1% MNI median and Bloomberg consensus) up from 3.99% in August. Given the volatility (and unreliability) of the LFS data, we don’t place too much weight on the unemployment rate.

For the full document see the PDF: UK_Data_Labour_2024_11_Release.pdf

EURUSD TECHS: Fresh Trend Low

Nov-11 13:53

- RES 4: 1.1040 High Oct 4

- RES 3: 1.0997 High Oct 8

- RES 2: 1.0937 High Nov 5 and key short-term resistance

- RES 1: 1.0761/0850 Low Oct 23 / 20-day EMA

- PRICE: 1.0646 @ 13:52 GMT Nov 11

- SUP 1: 1.0637 Low May 1

- SUP 2: 1.0611 38.2% retracement of the Sep ‘22 - Jul ‘23 bull cycle

- SUP 3: 1.0568 Low Nov 2 2023

- SUP 4: 1.0517 Low Nov 1 2023

A sharp sell-off on Nov 6 in EURUSD highlighted a resumption of the current downtrend. The move down resulted in a reversal of the recent Oct 23 - Nov 5 correction and a breach of 1.0761, the Oct 23 low. Today’s fresh cycle low reinforces the bearish theme and sights are on 1.0611, a Fibonacci retracement. Key short-term resistance has been defined at 1.0937, the Nov 5 and 6 high. A break would highlight a potential reversal.

Trending Top

Mar-27 20:13