NZD: Reaction To RBNZ

NZD/USD went into the RBNZ meeting around 0.5795(+1.15%) and the NZX50 around 13300(+1.75%). "NZ LEA...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

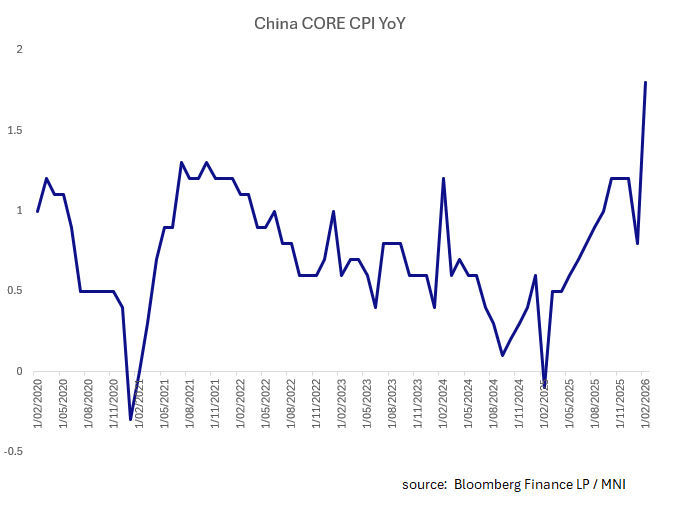

CHINA: LNY Distortions Give CPI a Bump, Look for RRR Cut Soon

- China's February 2026 inflation data shows a significant rebound in consumer prices alongside moderating factory-gate deflation, though underlying demand remains muted.

- China's CPI rose +1.3% year-on-year, significantly exceeding the +0.9% market forecast. This follows a muted 0.2% increase in January, which was weighed down by unfavorable base effects and a later Lunar New Year. The sharp rebound is largely attributed to the LNY holiday surge in spending on travel, food, and services, though January / February releases are best considered as a combined read.

- The PPI fell -0.9% YoY, marginally better than expectations and down from January's -1.4%. This marks the 41st consecutive month of PPI contraction. The moderation was driven by firmer global commodity prices (especially non-ferrous metals and gold) and government efforts to curb "involution" or excessive price competition in key industries.

- Core CPI was up also at +1.8%, its highest since March 2019.

- The narrowing PPI decline suggests that Beijing's push to reduce industrial overcapacity and end aggressive price wars is beginning to take some effect at the factory gate.

- Whilst the official 2026 CPI target is set at around 2%, markets treat this as a ceiling rather than a forecast, with most economists projecting actual full-year inflation between 0.8% and 1.0%.

- Consensus is building for a RRR cut post the NPC, which would inject c. CNY1tn of liquidity to support government funding objectives.

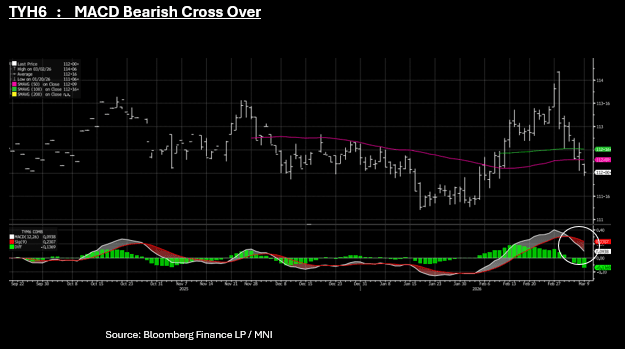

US TSYS: 10-Yr Eyes 4.20%: Feb High 4.27% Next

The US 10-Yr future opened down Monday, following on from Friday's weakness in the US. TYH6 ended Friday at 112-14 and touched 111-30 in the early part of the trading morning, currently at 112-00+. Whilst short term momentum indicators like the 14-day relative strength index have not reached oversold yet, the bearish crossover of the MACD (white) line over the Signal (red) line shows that the bearish momentum is significant.

Cash is weaker again with the 10-Yr nearing 4.20%. A close above could see the February high of 4.27% reached rapidly, given the pace of the sell off. Beyond that lies 4.30% the January high for the 10-Yr.

- The 2-Yr is up +4.6bps at 3.61%

- The 5-Yr is up +5.3bps at 3.781%

- The 10-Yr is up +5bps at 4.193%

- The 30-Yr is up +4.5bps at 4.805%

Given the oil led/ inflationary environment - data is likely to take a back seat here. Nonetheless NY FED 1-Yr inflation expectationsf ro FEB are released which are unlikely to capture the oil moves since the US attacked Iran, NFIB Business Optimism and the ADP Weekly Employment Change.

There are two auctions - a US$89bn 13-week and a US$77bn 26-week.

CNH: USD/CNY Fixing Rebounds, Error Term Back To Positive

The USD/CNY fix was set at 6.9158, notably above Friday's 6.9025 outcome. The fixing error flipped back to a positive of +42pips, versus -64pips on Friday. This has helped push USD/CNH higher, getting to 6.9341, but we sit slightly lower now, last near 6.9300. Onshore spot is opening up higher, the pair pushing above 6.9250. We had a little while ago the Feb inflation figures which were stronger than forecast at 1.3%y/y for headline CPI (0.9% projected and 0.2% prior) and -0.9%y/y for PPI (-1.1% projected).