EM LATAM CREDIT: Raizen: Potential Buyer of Arg. Assets – Positive

(RAIZBZ; Baa3*-/BBBneg/BBB-*-)

• Swiss commodity trading company Mercuria is reportedly the lead candidate to buy Raizen’s Argentina refinery and fuel distribution network for USD1.4bn, according to local news outlet Ambito, which is consistent with previous estimated values in past months.

• RAIZBZ 35s have been stuck in a holding pattern the past three weeks within a point of current quoted levels as we await news of a capital injection and asset sales, last quoted $82.17, down .44 today. Bonds are down almost 12 points since June 30th amid persistent operational losses and rising debt leverage.

• Mercuria has exploration and development assets in Vaca Muerta as well as a few other stakes in energy related investments in Argentina so this acquisition would fit in with their vertical integration strategy.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Fresh Record High

- RES 4: 180.86 Top of a bull channel drawn from the Feb 28 low

- RES 3: 180.00 Psychological round number

- RES 2: 178.94 1.236 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 1: 178.23 Intraday / Record High

- PRICE: 178.09 @ 16:24 GMT Oct 27

- SUP 1: 175.80 20-day EMA

- SUP 2: 174.82/27 Low Oct 17 / 50-day EMA

- SUP 3: 173.92 Low Oct 6 and a gap high on the daily chart

- SUP 4: 173.24 High Oct 3 and a gap low on the daily chart

The trend structure in EURJPY is unchanged, it remains bullish and the latest recovery reinforces bullish conditions. The cross has cleared key resistance and the bull trigger at 177.94, the Oct 10 high, hitting new record highs in the process. 178.94, a Fibonacci projection, is the next key upside level. First key support to watch lies at 175.80, the 20-day EMA. Support at the 50-day EMA is at 174.27.

US TSYS: Bonds Reverse Early Weakness, Curves Twist Flatter Ahead Wed's FOMC

- Treasuries are mixed after the bell, curves flatter (5s30s -3.996 at 94.579) with bonds outperforming - leading a bounce off midmorning lows; 27th day of the US Govt shutdown.

- Currently, Dec'25 TY contract trades -1 at 113-13 vs. 113-14.5 high, 10Y yield -.0097 at 3.9910%. A bullish structure in Treasuries remains intact and recent weakness appears to be a correction. The breach of a key resistance at 113-29, the Sep 11 high, confirmed a resumption of the medium-term uptrend.

- Spot Gold is now down 10% from last week’s all-time highs of $4,381.5, with an easing of US/China trade tensions being cited as the driver of today’s pullback. While the USD index came under some pressure, the sharp unwind for spot gold has offset the greenback pessimism somewhat

- Focus on Wednesday's FOMC - overwhelmingly expected to cut the funds rate by 25bp for a 2nd consecutive meeting on October 29, bringing the target range to 3.75-4.00%.

- Projected rate cut pricing vs. late Friday levels (*): Oct'25 at -24.5bp (-24.2bp), Dec'25 at -48.1bp (-50.2bp), Jan'26 at -61bp (-63.7bp), Mar'26 at -72.7bp (-75.8bp).

- Stocks continue to drift at/near record highs late Monday, sentiment buoyed amid trade optimism between the US & China. Officials from the two countries have reached basic consensus on arrangements to address their respective trade concerns following two days of talks in Kuala Lumpur, the People’s Daily reported.

- Earnings expected after the close include Whirlpool Corp, Alexandria Real Estate, Olin Corp, Waste Management, Nucor Corp, Brown & Brown, Welltower, Avis, Cadence, F5 and Amkor Technology.

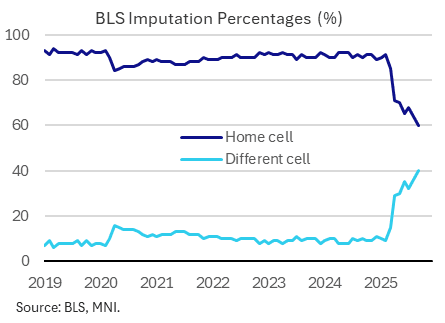

FED: Macro Since Last FOMC - Prices: Data Quality Concerns Increase

- When thinking about how the Fed will view this report, it’s important to note that translating it to core PCE with no publication of a PPI report would have been hard enough this month (CPI provides ~65% of inputs), but uncertainty is greater still with a deterioration in the quality of the CPI report itself.

- September saw 40% of sources using “different cell” imputation, a new high after 36% in August as budget and staff cuts have an increasingly large impact. It has historically averaged closer to 10% and peaked at 15% in the pandemic when in-person surveys weren’t possible, but it jumped to ~30% April and has continued to increase since.

- This September release shouldn’t have been impacted by the government shutdown in the sense that the data would have already been collected.

- The shutdown was however seriously calling the quality of the subsequent October report into question, although the White House's Rapid Response account on X.com suggests that the BLS may not release it because it was unable to conduct the in-person surveys as normal during the month.

- As for alternative timely indicators, the Fed’s Beige Book published Oct 15 was arguably the most inflationary Beige Book of 2025, certainly joint with June which saw 8 (of 12) districts characterize inflation pressures as "moderate", despite weaker growth conditions.