EU REAL ESTATE: Property: Week in Review

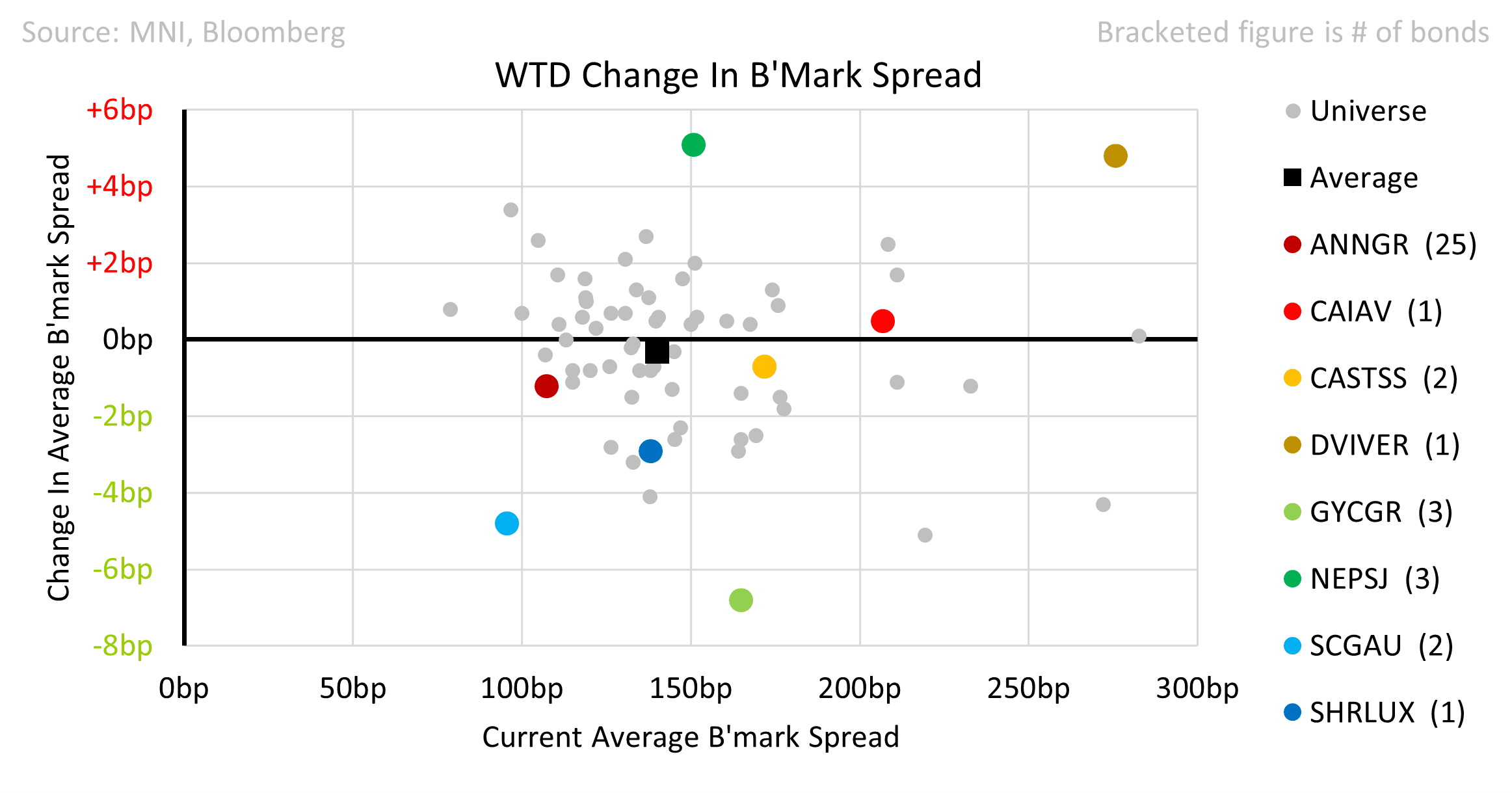

Up until the Trump tariff announcement, spreads were unchanged on average on the week. NEPSJ was the weakest name but after a strong rally from early April.

• Shurgard Є500m 10yr came just inside our FV with a nearly 5x book. The company has a very strong business model. The existing 34s tightened 3bps on the week.

• CA Immo released a strong update along with the very positive news that they had received an unsolicited approach for its Austrian business (5% assets) and one CEE country’s portfolio. The 30s were +2 wider but only after the Tariff headlines.

• Castellum upgraded to Baa2.

• Vonovia tendered for up to €500m of the ANNGR 4.75 27 and ANNGR 5% 30. We were able to flag this to clients during the outage on Wednesday. The 30s tender price is 1.25pts above the undisturbed price; the bonds tightened 10bps and 15bps on the week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Early Volatility Buyer

- +7,500 TYM5 111 straddles, 156

- 2,000 TYN5 109/114 strangles ref 111-10

- 1,058 FVM5 108.5/109.5/110.5 call flys ref 108-12

- +1,000 FVK5 108.25/108.5 strangles, 18.5 ref 108-11.75

BONDS: Gilt Bulls Unable To Force Break Below 200bp Vs. Bunds

The combination of beta to Tsys, this morning’s gilt remit revision and softer-than-expected UK PMI data has driven gilt outperformance vs. Bunds, with the UK/German 10-Year yield spread ~8bp tighter on the day at 202bp.

- The spread currently trades around the middle of its year-to-date range (177-227bp, based on closing levels).

- Gilt bulls were unable to force a break below 200bp, with the spread basing at 200.4bp around 12:00 BST.

- Gilt bulls have not managed to push the spread back below the 200bp mark since the break above on April 9.

- Potential meaningful reallocation flows out of Tsys have made the spread particularly difficult to trade in recent weeks, as have a couple of instances of reduced liquidity further out the UK curve.

- Outside of the intraday noise, longer term focus continues to fall on relative fiscal outlooks, with the UK already experiencing limited fiscal headroom, while Germany has pledged meaningful fiscal expansion, which is set to drive an uptick in issuance over the medium-term.

EGB SYNDICATION: Austria Triple Tranche Tap: Priced

2.50% Oct-29 RAGB (ISIN: AT0000A3EPP2)

- Reoffer: 100.86 to yield 2.293%

- Spread set earlier at MS + 19bp (guidance was MS+20 Area)

- Benchmark: HR 99% vs 2.50% Oct-29 Bobl +32.5bp. Spot ref 102.24.

- Size: E3bln (inc E500mln retention)

- Books closed in excess of E16.7bln (inc E1.525bln JLM interest)

- TOE: 13:46BST / 14:46 CET. FTT immediately.

3.20% Jul-39 RAGB (ISIN: AT0000A3D3Q8)

- Reoffer: 99.562 to yield 3.238%

- Spread set earlier at MS + 66bp (guidance was MS+67 Area)

- Benchmark: HR 87% vs 4.25% Jul-39 Bund +52.7bp. Spot ref 117.92

- Size: E2.25bln (inc E250mln retention)

- Books closed in excess of E22.9bln (inc E1.25bln JLM interest)

- TOE: 13:43BST / 14:43 CET. FTT immediately.

3.15% Oct-53 RAGB (ISIN: AT0000A33SK7)

- Reoffer: 95.00 to yield 3.427%

- Spread set earlier at MS + 97bp (guidance was MS+98 Area)

- Benchmark: HR 104% vs 1.80% Aug-53 Bund +56.1bp. Spot ref 79.51

- Size: E1.75bln (inc E250mln retention)

- Books in excess of E23.2bln (inc E1.65bln JLM interest)

- TOE: 13:40BST / 14:40 CET. FTT immediately.

For all:

- Settlement: April 30, 2025 (T+5)

- Bookrunners: Barclays (B&D), Citi, DB, GS, JPM, Raiffeisen Bank

From market source