OUTLOOK: Price Signal Summary - Fresh Cycle Low In Bunds

Nov-20 12:28

- In the FI space, a bear cycle in Bund futures remains intact and today’s fresh cycle low reinforces a bear theme. The contract has pierced support at 128.52, the 76.4% retracement of the Sep 25 - Oct 17 bull leg. A clear break of this price point would signal scope for an extension towards 128.25, the Oct 7 low. Key short-term resistance is seen at 129.40, the Nov 13 high. Clearance of this hurdle would signal a reversal. First resistance is 129.07, the 50-day EMA.

- A sharp sell-off in Gilt futures yesterday strengthens a bearish threat and cancels a recent bullish condition. The contract has traded through support at 91.82, the Sep 11 high, and the move down signals scope for a deeper retracement that opens 91.12, 61.8% of the Sep 3 - Nov 4 bull leg. On the upside, initial key resistance is seen at 92.82, the 20-day EMA. A clear break of the average is required to signal a reversal.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK DATA: MNI UK CPI Preview

Oct-21 12:24

For the full document including sellside summaries click here.

- September CPI data on Wednesday should be significant as it is expected to mark the peak in CPI as it is boosted largely by base effects. The median of the previews that we have read look for a 4.0%Y/Y headline print which is almost exactly in line with the BOE’s 3.99%Y/Y projection. Note that this follows the BOE’s August projection coming within a hundredth at 3.79%Y/Y.

- Despite some MPC members appearing to have more entrenched views, we think that this data release will have huge importance for the prospects for a Q4 cut. We think that markets continue to underprice the possibility of a November cut (only 2.6bp priced at writing) with 9.1bp priced by December.

- We look through the details of what is expected in the upcoming CPI print and detailed expectations from the sellside.

- Petrol price and air fare base effects expected to boost headline Y/Y CPI by 7-9 hundredths while there is focus on the index date and tube strike, accommodation, catering and tuition fees.

- Core goods prices expected broadly unchanged.

- Food risks skewed to the downside, alcohol and tobacco to the upside.

COMMODITIES: Gold Accelerates Losses, But Move Looks Isolated For Now

Oct-21 12:23

- Gold prices fade to hit a new intraday session low, however the price action looks localized to gold as silver, platinum and palladium remain just above their respective daily lows printed earlier this morning.

- We note no signals of CTA flow, although these could remain a primary driver of the latest slippage.

- The price action on the latest leg lower looks consistent with flow, as short-term longs may be closed out on the way through $4250 support. Initial support in gold moves up to $4186.42 (Friday's low).

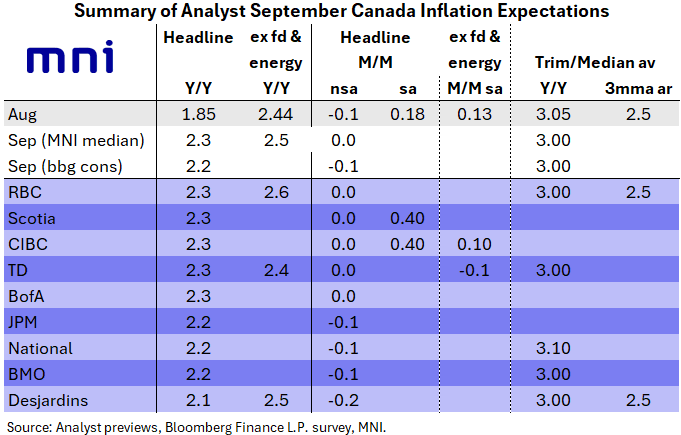

CANADA: Continued Progress On Trim/Median CPI Seen In Sept

Oct-21 12:20

Analysts look for a general continuation in softening in core price pressures in September's CPI report (0830ET), with the closely-watched trim/median average measure eyed by the BOC seen coming in at 3.0% after 3.05% in August.

- Headline Y/Y inflation is seen rising to 2.3% (MNI Median), a jump from 1.85% prior but this is largely on account of year-before base effects. The M/M reading is expected to come in flat with some bias toward a slightly negative print. When seasonally-adjusted, that would likely result in a fairly solid positive print.

- Categories to watch: goods prices following the removal of Canadian retaliatory tariffs on the US at the start of September (seen as key to an improvement in overall core pressures as well as for food), and a continued normalization of shelter costs which appears to be a relatively consensus expectation among analysts' notes we've seen.

- Recall in August, Ex-food and energy inflation (2.44% Y/Y unrounded) was the lowest since March (2.50% prior), while the measure of CPI ex-8 most volatile/indirect taxes was relatively steady at 2.63% (2.57% prior).

- The August report cemented a September BOC cut; current pricing for end-October is 19bp with 26bp through year-end.