US: President Trump To Speak At White House Event Shortly

US President Donald Trump is shortly due to deliver remarks at a White House round table billed as "...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

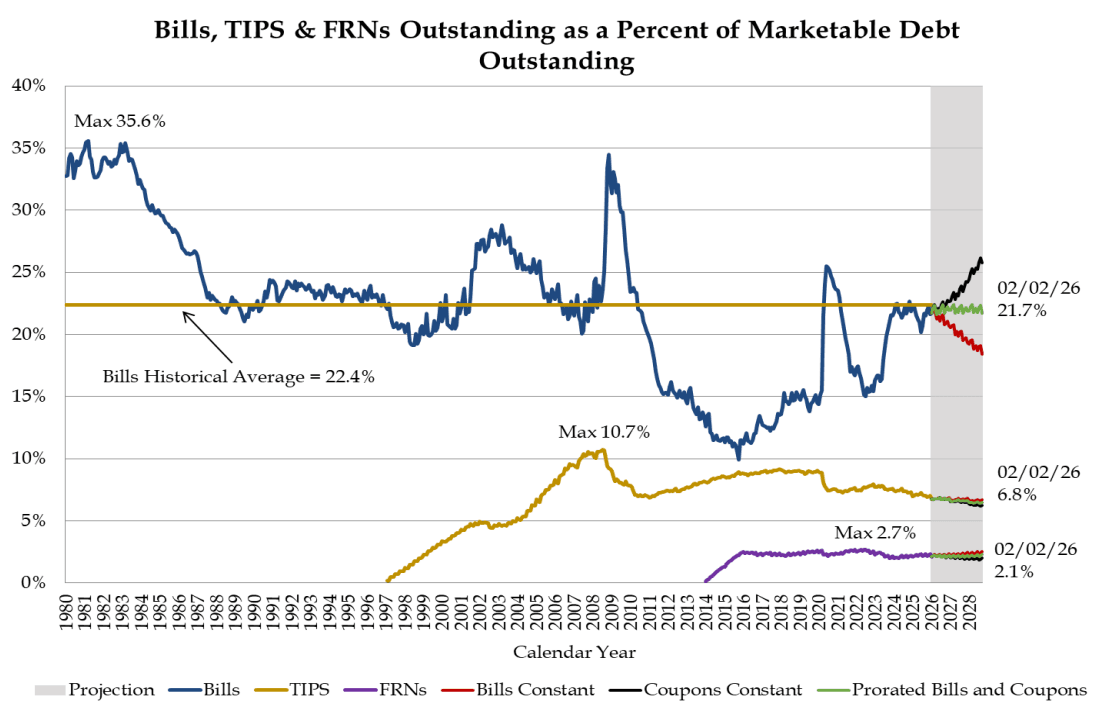

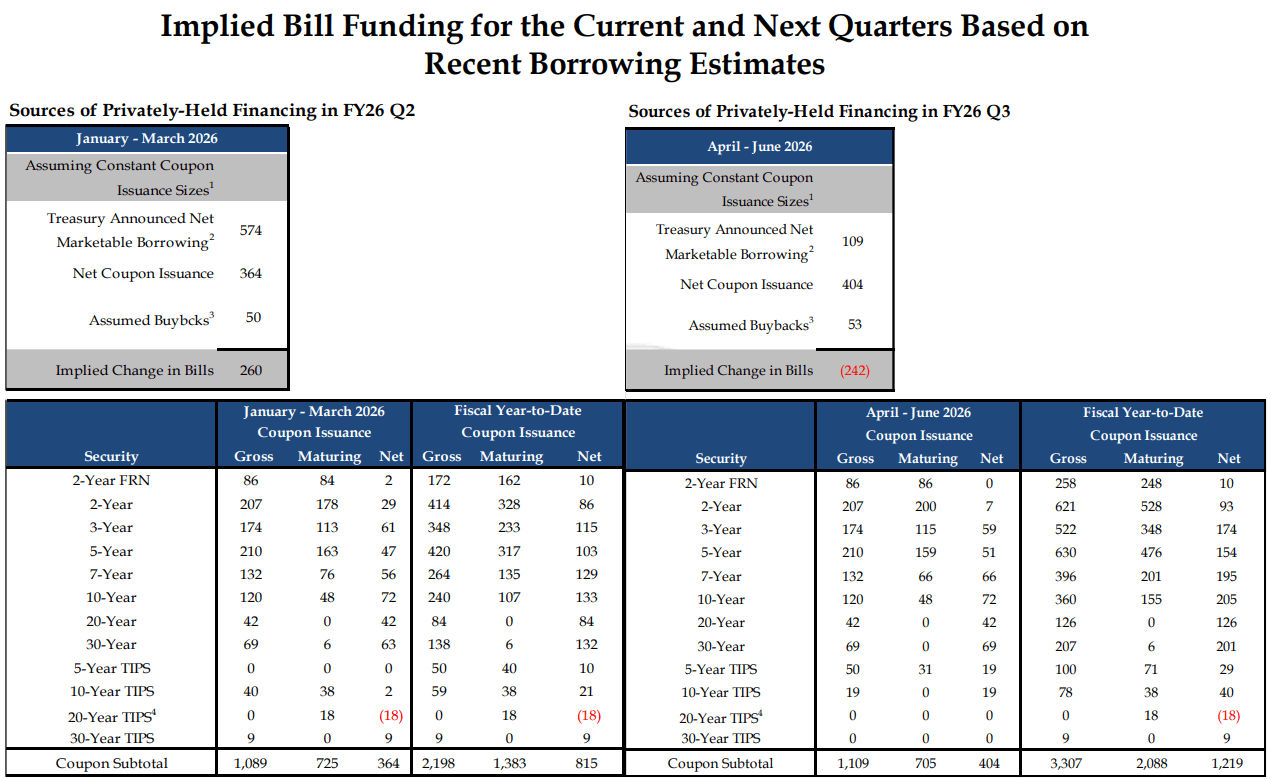

US TSYS/SUPPLY: Near-Term Bill Outlook Steady Before Usual Tax Season Drop (2/2)

While it continues to eye nominal coupon auction size increase at some point in upcoming quarters, and made its clearest signal yet that it would be looking increasingly toward bills to meeting financing requirements, Treasury's near-term outlook for bill sales looks to be largely as anticipated.

- As expected Treasury has no plans to upsize current bill auction sizes and as usual will start to pull them back going into the April tax receipt season.

- Per the Refunding policy document, "Treasury expects to maintain the offering sizes of benchmark bills at or near current levels into mid-March. By late March, Treasury anticipates incrementally reducing short-dated bill auction sizes in light of the April 15 tax date. These reductions will likely lead to a cumulative $250-300 billion net decline in total bill supply by early May."

- TBAC estimates that the net implied change in bills is basically flat through the first half of the calendar year, with $260B increase in supply through March followed by a drop of $242B in the Apr-Jun quarter (assuming a total of $103B in buybacks, based on previous quarters' results). This is calculated as: net marketable borrowing minus net coupon issuance plus buybacks as seen in the table. Note that buybacks

- Below is the TBAC presentation to the Treasury's estimates for bill financing as well as cumulative net issuance by Treasury coupon segment.

USDCAD TECHS: Unwinding A Recent Oversold Condition

- RES 4: 1.3929 High Jan 16 and a reversal trigger

- RES 3: 1.3879 High Jan 20

- RES 2: 1.3788 50-day EMA

- RES 1: 1.3715 20-day EMA

- PRICE: 1.3631 @ 17:01 GMT Feb 4

- SUP 1: 1.3482 Low Jan 30 and the bear trigger

- SUP 2: 1.3473 Low Oct 2 ‘24

- SUP 3: 1.3400 50.0% retracement of the 2021 - 2025 uptrend

- SUP 4: 1.3359 Low Jan 31 2024

The strong recovery from last Friday’s low in USDCAD continues to highlight a corrective cycle. Note that the trend has been in oversold territory and the bounce is allowing this condition to unwind. The next important resistance to watch is 1.3715, the 20-day EMA. Resistance at the 50-day EMA, is at 1.3788. Key support and the bear trigger has been defined at 1.3482, the Jan 30 low. A break of this level would confirm a resumption of the downtrend.

US TSYS/SUPPLY: Treasury Eyeing Later Coupon Upsizing, More Bill Reliance (1/2)

The combination of the two small changes in Treasury's guidance should help dispel suggestions that there is serious thought being given by Secretary Bessent and his team to reducing coupon sizes any time soon.

- Treasury's new guidance reads "Based on current projected borrowing needs, Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters. Treasury is monitoring SOMA purchases of Treasury bills and growing demand for Treasury bills from the private sector. Looking ahead, Treasury continues to evaluate potential future increases to nominal coupon and FRN auction sizes, with a focus on trends in structural demand and potential costs and risks of various issuance profiles", with that second sentence on Bills being added to the prior edition, and "continues to evaluate potential future increases" replacing "has begun to preliminarily consider future increases".

- As has seemingly been the case for a few refundings, there appeared to have been some lingering anticipation/hope that Treasury could signal the possibility of coupon reductions or, at the very least, suggest that an increase remained a distant prospect. As such swap spreads tightened and the curve lightly bear steepened following the release of the Policy Statement.

- Treasury's advisory committee (TBAC) reported it "continues to believe that current projections could warrant increases in coupon issuance in FY2027. The Committee had a robust discussion on the relative tradeoffs of increasing auction sizes more gradually, perhaps earlier than needed, compared to a more accelerated path of auction size increases when the financing gap is larger."

- MNI's penciled-in date for coupon upsizing of November 2026 looks increasingly on the early side; we note also that TD after the Refunding announcement wrote "we now only expect Treasury to increase auction sizes in February 2027 and look for the increases to be limited to the 2-10y sector" (previously they'd seen "late 2026).

- Treasury's subtle message in inserting the sentence on Bills without suggesting any particular action is that the current environment gives it flexibility to lean increasingly on bills. That was probably already assumed, but it's notable that Treasury put this explicitly into its policy statement.

- TBAC also noted in a scenario analysis that Fed bill purchases will help offset any increase in proportional issuance in terms of bills held by private market participants: "increased Treasury bill purchases in the Fed SOMA mean that even though the bill share of total issuance rises from 21.6% to 23.2% YoY, the share of privately-held debt outstanding represented by bills remains unchanged". Overall, "in the current environment, it would be reasonable for Treasury to meet some portion of the Federal Reserve’s System Open Market Account (SOMA) demand for Treasury bills through increased issuance in this sector of the curve."