RUSSIA: Peskov-We Hope UAE Withdrawal Does Not Imply End To OPEC+

Apr-29 10:19

Following the UAE's shock withdrawal from OPEC and OPEC+, announced on 28 April, Kremlin spox Dmitri...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: 80bp Of ECB Hikes Priced After Hawkish Inflation Components In EC Survey

Mar-30 10:16

Hawkish move in EUR STIRs in the time since the European Commission’s economic survey.

- We flagged the potential for increased attention on the data ahead of the release, specifically on the inflation front.

- The press release accompanying the data noted that “press Managers’ selling price expectations were sharply up in all four business sectors, and strikingly so in industry. Selling price expectations moved further beyond their long-term average in all business sectors. Consumers’ perceptions of price developments over the past twelve months increased moderately, but their expectations about price developments for the next twelve months surged”. This triggered the hawkish move.

- ECB-dated OIS pricing 80bp of hikes through year-end vs. ~73bp at one point this morning.

- Euribor futures now 0.5-3.0 firmer on the day.

- Thursday’s high in ERZ6 held, with the contract now 7.0 off highs.

- Monday ECB-speak has been fairly neutral but cognisant of stagflationary risk linked to the Iran conflict.

- National level German inflation data is due later, with the regional level readings seen so far roughly in line with national consensus (+2.6% Y/Y for CPI vs. +1.9% last time out).

ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR (bp) |

Apr-26 | 2.073 | +14.3 |

Jun-26 | 2.293 | +36.3 |

Jul-26 | 2.454 | +52.4 |

Sep-26 | 2.602 | +67.2 |

Oct-26 | 2.686 | +75.6 |

Dec-26 | 2.732 | +80.2 |

OUTLOOK: Price Signal Summary - Bearish Theme In S&P E-Minis Intact

Mar-30 10:05

- In the equity space, a bear trend in S&P E-Minis remains intact and last week’s sell-off reinforces current conditions. Note that moving average studies remain in a bear-mode position, highlighting a dominant downtrend. This opens 6316.61 next, a 3.236 projection of the Feb 11 - 17 - 25 price swing. Initial firm resistance is at 6699.10, the 20-day EMA. A bounce would be considered corrective.

- The trend condition in EUROSTOXX 50 futures remains bearish and recent gains appear to have been corrective. Note that the S/T trend condition is oversold and a stronger recovery would allow this set-up to unwind. Key pivot resistance is seen at 5750.39, the 50-day EMA. Scope is seen for an extension towards 5277.64 next, a 1.382 projection of the Mar 5 - 9 - 10 price swing.

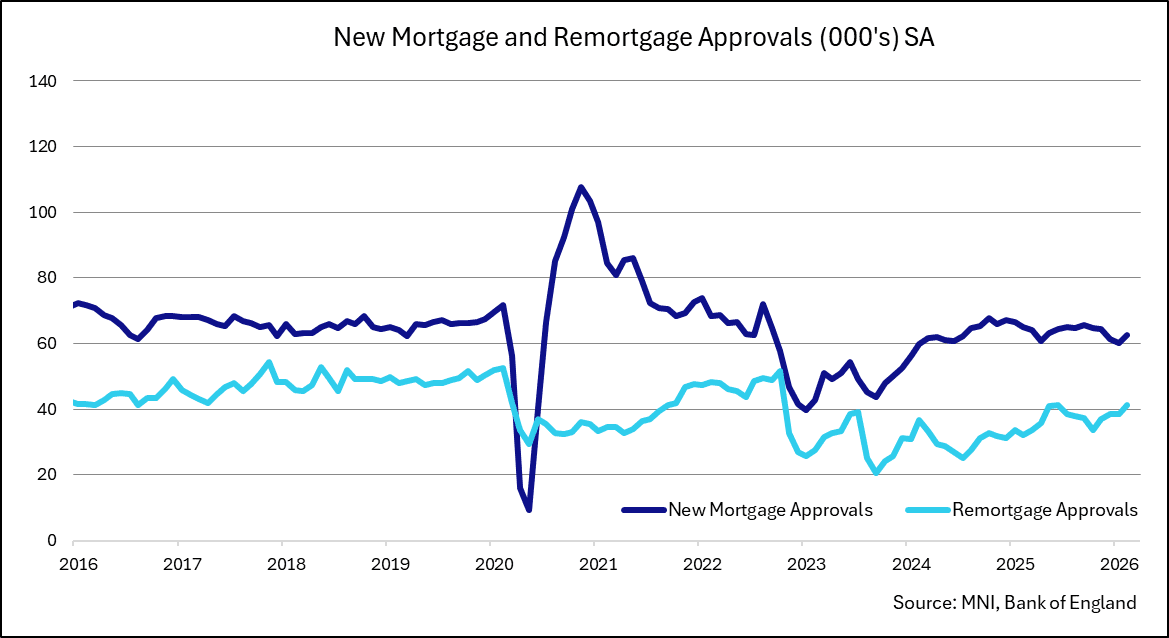

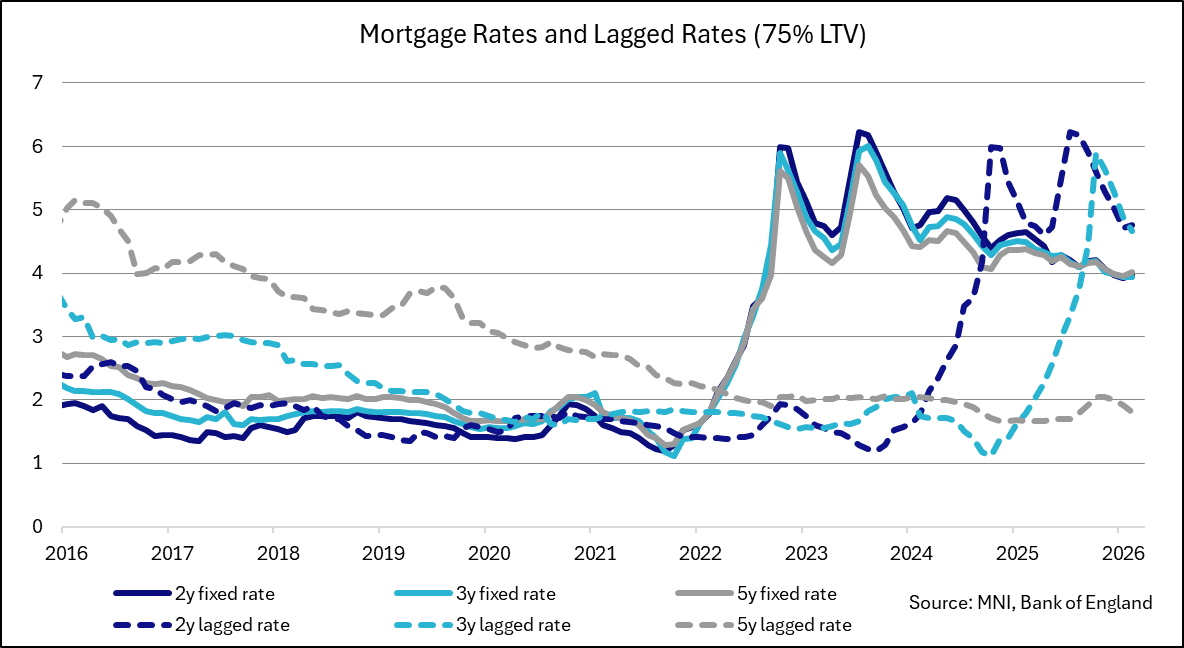

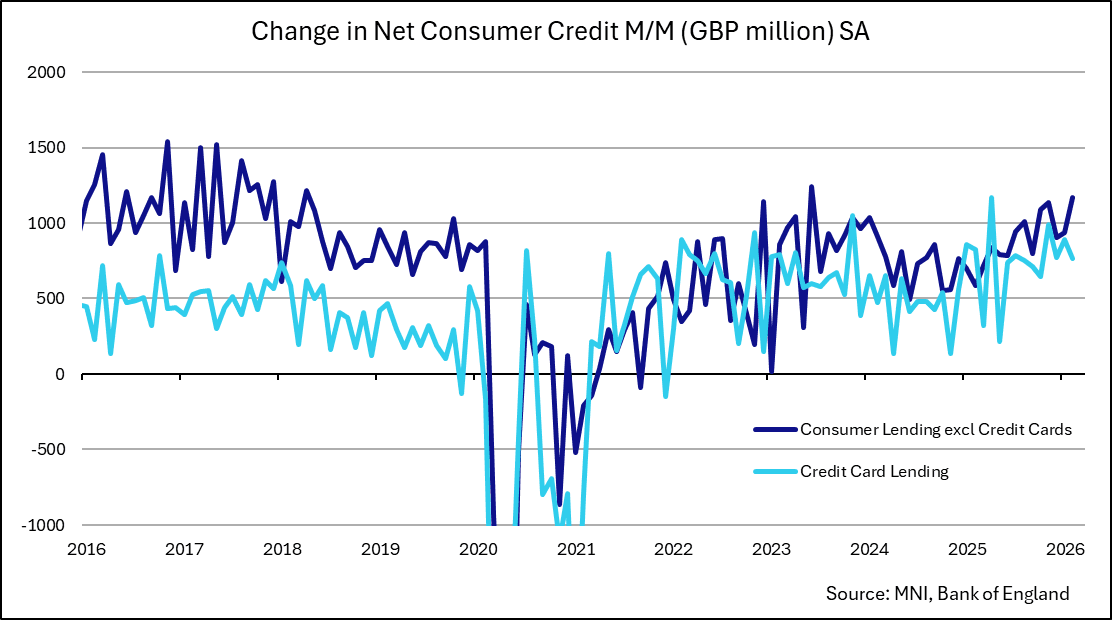

UK DATA: Private Lending Growth Surprisingly Solid Before Iran Conflict

Mar-30 10:01

UK mortgage lending came in notably stronger than expected in Feb (along with an upward revision to Jan), with mortgage approvals also just on the stronger side. Changes in mortgage rates were mixed across the maturity profile, but of course this data comes pre-Iran conflict. Net consumer credit was also on the stronger side.

- We wouldn't read too much into this print given it's already pretty outdated, but the potential tentative slowing of demand shown by Jan's data now seems short-lived. March data will likely be more important in assessing the impact of the latest shock on housing demand.

- Net lending on dwellings picked up to GBP4.84bln in February (cons GBP3.9bln) after an upward revised GBP4.21bln (vs GBP4.08bln) in January. Net mortgage approvals grew around 2.3k to 62.6k in Feb (60.8k cons, 60.2k prior, revised up from 60.0k). Changes in mortgage approvals have been quite muted in recent months, especially compared to the net lending on dwellings figure.

- Net consumer credit was also on the stronger side in Feb, at GBP1.94bln (cons GBP1.6bln) after GBP1.83bln in Jan (revised up from GBP1.81bln). The press release notes "net borrowing through credit cards was GBP0.8bln in February, down from GBP0.9bln in January. Net borrowing through other forms of consumer credit (such as car dealership finance and personal loans) increased to GBP1.2bln in February, up from GBP0.9bln in January."

- Mortgage rates were mixed across the maturity profile (-0.03 to +0.06ppt). Those remortgaging from a 2y or 3y fixed rate mortgage onto another of the same mortgage would still see around 0.7-0.8ppt drops in their mortgage rates, while those remortgaging from a 5y fixed rate onto the same would see a jump of around 2.2ppt.

- "The ‘effective’ interest rate – the actual interest paid – on newly drawn mortgages slightly increased, to 4.10% in February, from 4.09% in January. The rate on the outstanding stock of mortgages was 3.95% in February, up from 3.90% in January." - from the press release.

- Also in the release, M4 money supply growth picked up to 0.6% M/M, 3.6% Y/Y (from -0.1% M/M, 3.0% Y/Y in Jan).