US DATA: Payrolls Wrap: Weak And Volatile But Trend U/E Rate Broadly Stable

Mar-06 18:18

* Key figures in both the establishment and household surveys disappointed in the February payroll...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

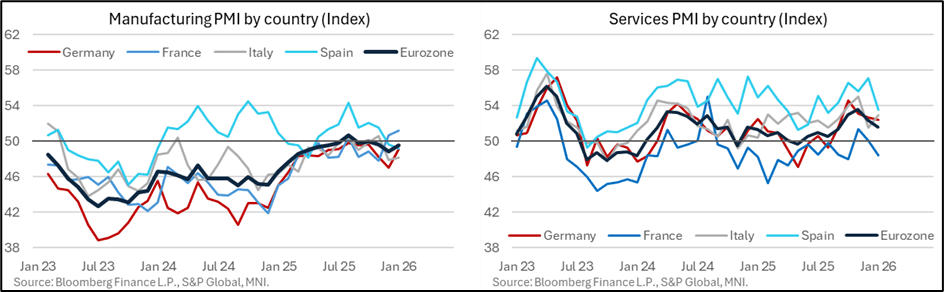

ECB: Macro Since Last ECB - Growth: ... But Further Stalling Of PMI Improvement

Feb-04 18:17

- PMIs meanwhile have been at best more mixed since the last meeting, with manufacturing on net a little stronger but services weaker.

- Specifically, the manufacturing PMI has most recently been seen at 49.5 in Monday’s final January release vs 49.2 in the December advance seen prior to the ECB decision, via 48.8 in the final December release.

- It mostly recovered to the 49.6 in Nov but despite seeing a trend improvement in 2025 has still seen only two months at or above the 50 breakeven level (Aug and October). The January details noted that "The volume of new work received by eurozone goods producers fell for a third successive month at the beginning of the year, although the contraction slowed and was only marginal. New export orders likewise decreased, in line with the trend since last July".

- The services PMI on the other hand was revised down from 52.6 to 52.4 in December before falling further to 51.9 in the flash January release and then lower again to 51.6 in Wednesday's final release for its lowest since September. Unusually, Spain saw a sharp 3.6pt drop to 53.5.

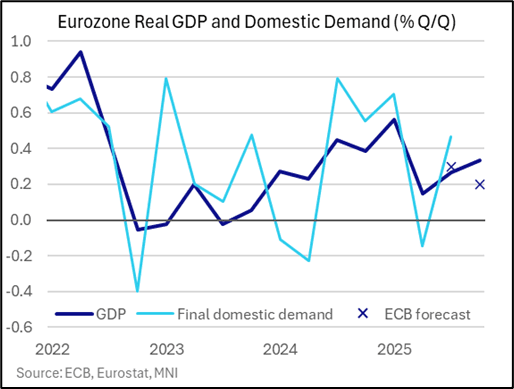

ECB: Macro Since Last ECB - Growth: Solid GDP...

Feb-04 18:15

- Eurozone real GDP growth was stronger than expected in the Q4 flash at 0.33% Q/Q vs consensus and ECB expectations of 0.2% and following 0.27% in Q3 (which had also surpassed ECB expectations of 0.0% from the September projections).

- Spain led individual contributions on the quarter (+0.08pp) owing to a strong 0.8% Q/Q increase, followed by Germany (+0.07pp, 0.3%), Italy (+0.04pp, 0.3%) and France (+0.03pp, 0.2%). There weren’t any material Irish distortions to consider, a small drag of -0.02pp after -0.01pp in Q3 and nothing like the +0.17pp averaged through 3Q24-1Q25.

- Aggregate details are lacking although country-level details point to a positive contribution from domestic demand whilst net trade looks mixed to potentially negative. Annual GDP growth stood at 1.32% Y/Y in Q4, technically a fourth consecutive deceleration as we move beyond that Irish boost but still above the 2023/24 average of 0.7%.

- Overall, the headline GDP data appeared consistent with ECB expectations for a cyclical recovery in 2026, with real GDP growth forecast at 0.3% Q/Q in Q1 before three quarters of 0.4% Q/Q.

EURUSD TECHS: Corrective Cycle Remains In Play

Feb-04 18:00

- RES 4: 1.2081 High Jan 27 and key resistance

- RES 3: 1.2045 High Jan 28

- RES 2: 1.1975 High Jan 30

- RES 1: 1.1896 Low Jan 28

- PRICE: 1.1797 @ 16:08 GMT Feb 4

- SUP 1: 1.1776 Low Feb 2

- SUP 2: 1.1735 50-day EMA

- SUP 3: 1.1693 76.4% retracement of the Jan 19 -0 27 bull leg

- SUP 4: 1.1670 Low Jan 22

A corrective cycle in EURUSD remains in play following the sharp reversal from the Jan 27 high. Note that moving average studies remain in a bull-mode position and this suggests that the retracement has been a correction - for now. Support to watch is at the 50-day EMA, at 1.1735. A clear breach of this 50-day average would suggest scope for a deeper retracement. Initial firm resistance is at 1.1896, the Jan 28 low.