IRAN: Parliament NSC Sec-Trump's Claims On Enriched Uranium 'Political Bluff'

Semi-official outlet ISNA reports comments from the secretary of the National Security Commission of the Parliament, Behnam Saeedi, claiming that US President Donald Trump's claim about the removal of enriched uranium from Iran is "completely baseless."

- He added that "[Iran's] right to enrichment, the complete lifting of sanctions, and the release of the country's assets are non-negotiable red lines." Adds that Trump's claims about enriched uranium having to leave Iran is "political bluff and a pure lie" and said: "No uranium has left the country."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

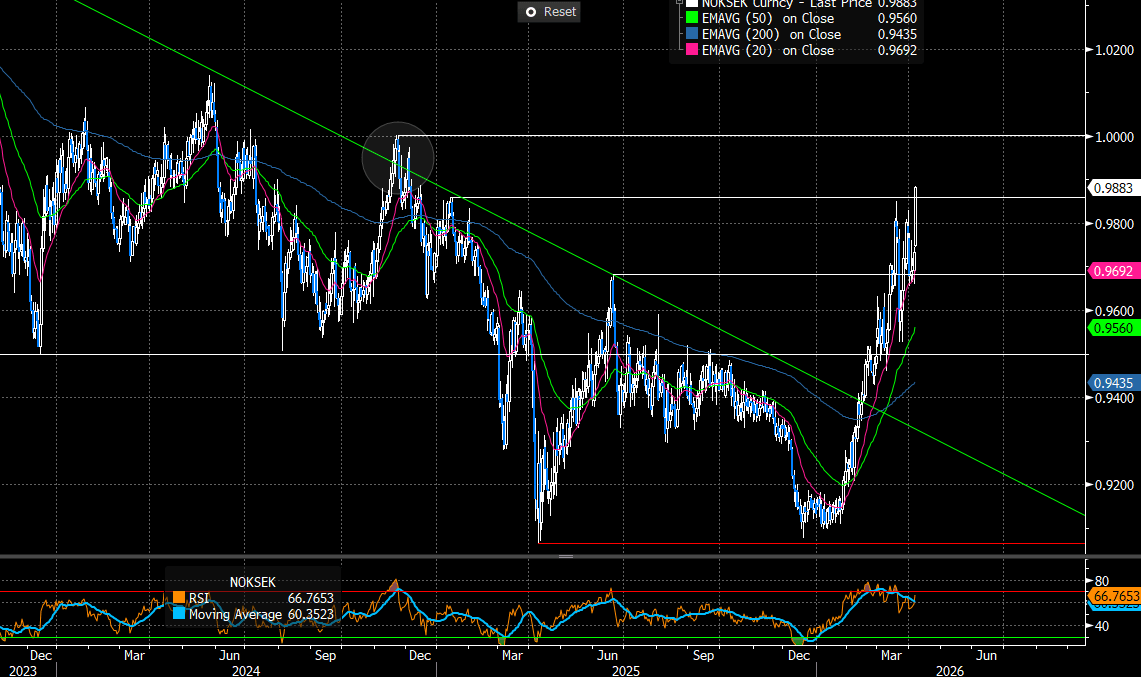

SCANDIS: NOKSEK Pierces Resistance, Driven By NOK Leg

Fresh push higher for NOKSEK in recent trade, this time driven by the NOK leg. The cross is now +1.5% on the session at 0.9880, piercing key resistance at 0.9859 (Jan 15 high). A clear breach of this level would expose parity as the next topside target.

- We haven’t seen an obvious trigger for the move, which also sees EURNOK lurch to session lows of 11.1540 (-0.5% today).

- NOK has benefitted from the terms of trade channel since the Iran war started, with a hawkish Norges Bank decision providing additional support in late-March. With the policy rate at 4.00% and likely to increase in the coming months, carry remains attractive, particularly with growth risks from the energy price shock less relevant in Norway compared to other DM peers.

- That said, the krone’s sensitivity to the broader global risk/growth backdrop presents an ongoing risk that could contain further strength going forward.

- Alongside Iran war developments, domestic focus remains on Friday’s inflation report.

Figure 1: NOKSEK Since 2024 (Source: Bloomberg Finance L.P)

ITALY T-BILL AUCTION PREVIEW: On offer Thursday

MEF will look to sell the following BOTs at its auction on Thursday:

- E2.5bln of the 3-month Jul 14, 2026 BOT

- E7.5bln of the new 12-month Apr 14, 2027 BOT

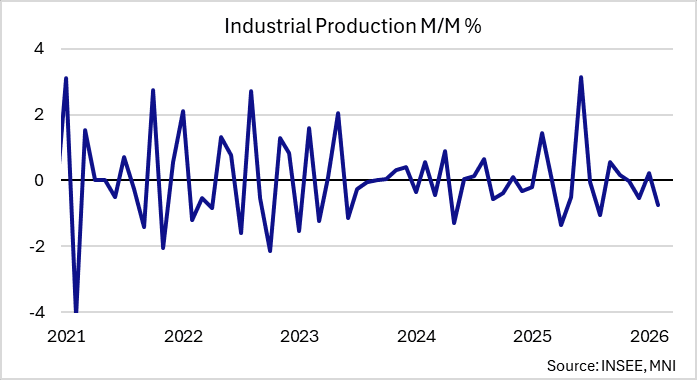

FRANCE DATA: Sharp IP Pullback In February on Mild Weather

Released on Good Friday, French IP pulled back sharply in February prior to any adverse impacts from higher energy prices following the Middle East conflict. It was driven by a steep decline in energy production due to unusually mild temperatures whilst manufacturing production was flat with offsetting detailed components.

- Industrial production fell -0.7% M/M (-0.1% cons) which was further dampened by a 0.3ppt downward revision to Jan's reading to 0.2%.

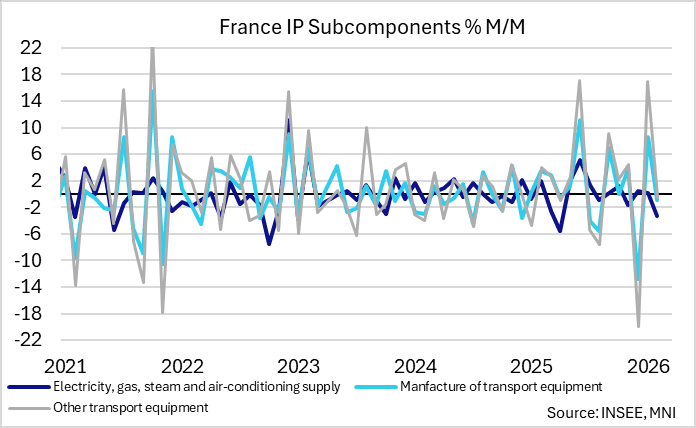

- The sharp decline in electricity, gas, steam and air conditioning supply (-3.2% M/M after +0.3%) was due to unusually mild temperatures in Feb. INSEE's household spending data released last week commented that Feb 2026 was the second-mildest Feb on record (since 1900, start of Metéo-France's series), which also caused a drop in energy consumption.

- Manufacturing output was stable on the month (after Jan's reading was revised down 0.4ppt to 0.2% M/M), driven by offsetting moves: food contracted again at -0.8% M/M after -0.9%, transport equipment dropped -0.8% M/M after a strong 8.5% increase (though revised down 1.3ppt).

- Rebounds were seen in "manufacture of "other industrial products (metallurgy, chemicals, pharmaceuticals, etc.)" (+0.4% after -1.0%) and in coking and refining (+1.8% after -3.1%). Finally, production stabilised in the manufacture of electrical, electronic, and computer equipment (after -1.4%)."

- The notable downward revisions to Jan are "due to the inclusion of late responses from some companies, particularly in the "other transport equipment" sector", which we note has been a big driver of the headline numbers as of late. While it hasn't hugely impacted the Feb data, its large upward influence on the Jan data has diminished (in the initial Jan release manufacturing output was only positive due to the strong increase in transport equipment).

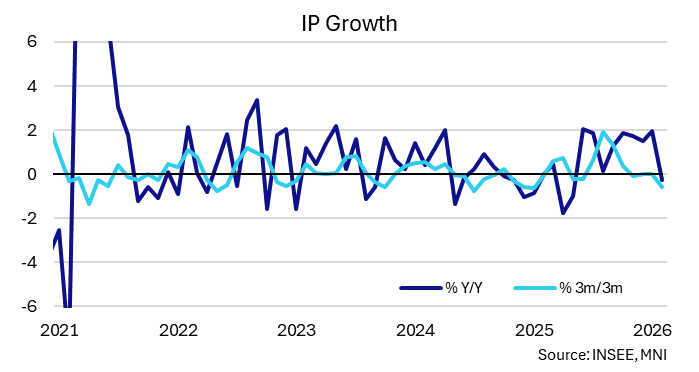

- Momentum in the series has slowed further, with 3M/3M growth dropping to -0.6% 3M/3M, from flat in the prior two months (helped lower by the latest revisions), for the lowest rolling quarterly rate since Jan 2025.

- Year-on-year, IP declined -0.3% Y/Y (1.6% cons, 1.9% Jan [revised down 0.5ppt]), the first negative reading since May 2025. Manufacturing output grew 0.8% Y/Y (2.1% Jan, revised down 0.6ppt).