EM LATAM CREDIT: Panama: Support for Copper Mine Reopening Increased – Positive

(PANAMA; Baa3neg/BBB-/BB+)

• Bonds have tightened 79bp since June 30th and 140bp YTD as the country has made progress on cutting the fiscal budget deficit. Reopening the copper mine, which at one point contributed 5% of GDP would be very supportive of the fiscal situation but is still facing a lot of opposition.

• A recent survey showed support climbed to 39.5%, up from 33.1%, according to Prodigious Consulting and La Estrella de Panama if there were better terms for the State which is what President Jose Mulino has promised. Unfortunately, 56.6% still don’t approve of the reopening.

• 62.9% said that nothing would change their opinion about reopening the mine and 47.1% said that environmental concerns were the main reason for the rejection. Only 10% would change their mind if independent environmental oversight were guaranteed, according to the survey.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

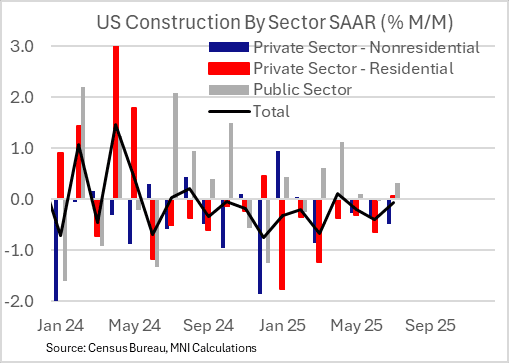

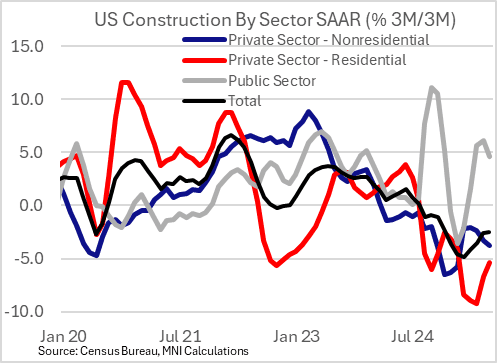

US DATA: Broad Private Sector Pullback In Construction Continues

Construction spending contracted in August for a 10th month in the last 11, despite residential activity seeing a rare uptick. Overall construction spending came in at -0.1% M/M (in line with consensus, -0.4% prior) in nominal, seasonally-adjusted annual rate terms.

- Private sector activity contracted for the 14th consecutive month (-0.2% after -0.5%). While residential construction - a little more than half of overall private sector construction - ticked 0.1% M/M higher for the first sequential increase of the year (-0.6% prior), nonresidential construction has seen continued deterioration. It contracted 0.5% (after -0.4%) for the worst performance since March, and comes as manufacturing construction fell 0.7% (same as prior).

- Public sector construction, about 1/4 of overall construction, grew for a 5th consecutive month, at 0.3%.

- The overall picture is of a 2.5% 3M/3M annualized rate of contraction for overall construction, a less-weak pace of growth than seen earlier in the year (closer to -5% in March) but with residential leading the "recovery" (-5.4% 3M/3M ann, best since February), and non-residential looking increasingly weak (-3.7%, weakest since February, led by Manufacturing construction at -7.7%).

- After tripling between mid-2021 and mid-2024 (rising proportionally from under 5% of construction to over 10%), the level of manufacturing construction has tailed off and is now at a 21-month low, with overall private sector construction at a 25-month low (and down 5+% from peak).

- Overall, since peaking in December 2023, private nonresidential construction has fallen by 6.9%. About 2/3 of the decline is attributable to a fall in commercial construction, in turn almost all warehousing/general commercial spending; within manufacturing the biggest pullback has been in computer/electronic/electrical which is down 10%.

- In another sign that AI-related spending is helping prop up the economy as a whole: data center spending hit a fresh all-time peak in July, and is up 69% since end-2023 (when overall construction started to decline). The rate of growth has started to slow in recent months but this is still clearly the brightest spot in an otherwise weak construction picture.

FED: US TSY 13W BILL AUCTION: HIGH 4.045%(ALLOT 77.02%)

- US TSY 13W BILL AUCTION: HIGH 4.045%(ALLOT 77.02%)

- US TSY 13W BILL AUCTION: DEALERS TAKE 28.05% OF COMPETITIVES

- US TSY 13W BILL AUCTION: DIRECTS TAKE 7.24% OF COMPETITIVES

- US TSY 13W BILL AUCTION: INDIRECTS TAKE 64.71% OF COMPETITIVES

- US TSY 13W BILL AUCTION: BID/CVR 2.96

FED: US TSY 26W BILL AUCTION: HIGH 3.880%(ALLOT 88.53%)

- US TSY 26W BILL AUCTION: HIGH 3.880%(ALLOT 88.53%)

- US TSY 26W BILL AUCTION: DEALERS TAKE 34.29% OF COMPETITIVES

- US TSY 26W BILL AUCTION: DIRECTS TAKE 10.97% OF COMPETITIVES

- US TSY 26W BILL AUCTION: INDIRECTS TAKE 54.74% OF COMPETITIVES

- US TSY 26W BILL AUCTION: BID/CVR 2.70