STIR: Over 20bp Of BoE Easing Priced For Dec After CPI

Nov-19 07:53

Dovish moves in the GBP front end as the latest CPI data doesn’t provide any impediment to the BoE cutting rates in December.

- BoE-dated OIS 1.5-3.0bp more dovish, showing ~20.5bp of easing for December, ~29bp through February, 38bp through March and 48.5bp through April.

- SONIA futures 0.25-4.0 higher, implied terminal rate pricing 3.35%, comfortably within the multi-week range.

- Looking at the data, outside of the 4 hundredths downside surprise in headline CPI (vs. BoE forecasts), services CPI was lower than BoE forecasts, while the food inflation metric was softer than BoE forecasts but firmer than the median of sell-side forecasts that we had seen.

- Note that the volatile airfares reading skewed services inflation lower as well.

- All in all, we think that the reading lowers the bar for a Dec cut but doesn’t have much of an impact for policy over the medium-term.

- A reminder that we will still get another round of CPI and labour market data before the Bank’s December meeting.

- Note the BoE will get the next round of CPI data under embargo on the Monday before the next meeting.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.764 | -20.5 |

Feb-26 | 3.676 | -29.3 |

Mar-26 | 3.590 | -37.9 |

Apr-26 | 3.484 | -48.5 |

Jun-26 | 3.437 | -53.2 |

Jul-26 | 3.458 | -51.1 |

Sep-26 | 3.444 | -52.5 |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUNDS: Block trade

Oct-20 07:53

Bund Block trade, suggest seller:

- RXZ5 2.4k at 129.90.

FRANCE: S&P Casts Doubt Over Budget Consolidation; Moody's Due Friday

Oct-20 07:47

- While the timing of S&P's decision came as a surprise, the outcome was in line with our expectations.

- S&P wrote that “reflecting the likelihood of modifications to the 2026 draft budget, we expect deficits to remain elevated over the next three years"

- "Even if snap parliamentary elections were to be called and produce a clear majority in the National Assembly, there is no guarantee that this would smooth the path for a credible medium-term fiscal consolidation plan or economic reform implementation. The closeness of the 2027 presidential elections casts doubt on whether any such strategy could be consistently implemented--or whether France could realistically achieve its 3% of GDP budget deficit target by 2029"

- S&P's 2026 deficit forecast of 5.3% is well above Lecornu’s target of 4.7% (which is expected to move closer to 5.0% through the budget negotiation phase).

- Moody's are scheduled to review France's sovereign rating on Friday (Current rating Aa3, Outlook Stable). An outlook downgrade to Negative is likely (and probably in the price for OATs), but a downgrade to A1 remains a risk.

- At the April periodic review, Moody's noted that "a reversal of the reforms implemented since 2017, such as labour market liberalization and pension reform, would be credit negative if we were to determine that this policy choice would have materially negative medium-term implications for France's growth potential and/or fiscal trajectory".

- A reminder that Lecornu has temporarily suspended the 2023 pension reform until the 2027 elections to appease the Socialists.

FRANCE: 10-year OAT/Bund Unwinds Some Early Widening As S&P Decision Digested

Oct-20 07:44

- The 10-year OAT/Bund spread opened ~2bps wider at 80bps, but has since narrowed back to ~79bps as markets digest S&P’s unscheduled rating downgrade (to A+ from AA-) on Friday. S&P had held France on a Negative Outlook, but were not scheduled to conduct a review until November 28.

- With the S&P downgrade now in the rear view, this could provide scope for OAT/Bund to drift lower in the coming weeks (based on a "no news is goods news" argument). However, we struggle to see the spread pushing below the 70bp handle in the near-term, and expect material upside sensitivity on headlines related to political/fiscal negotiations.

- Although PM Lecornu survived last week’s no confidence votes, risks remain present. Budget negotiations start from this week, and Lecornu will have to tread a fine line to maintain tacit support from the Socialist and Republican parties.

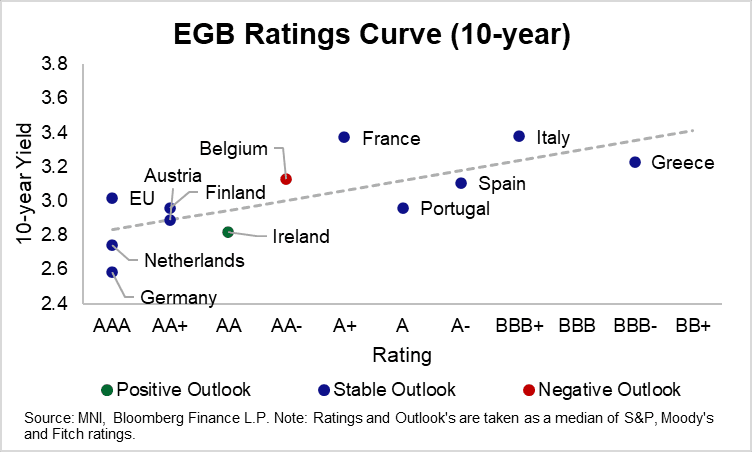

- The simple chart below suggests OATs continue to embed a political/fiscal risk premium, pushing 10-year yields above the ratings trendline.