LNG: Osaka Gas sees LNG Procurement as Manageable in Russia Supply Contingency

Osaka Gas, which sources about 2% of its LNG from Russia’s Sakhalin-2 project, says it can cover any disruption by boosting volumes under existing contracts or by turning to the spot market, Platts said.

- President Masataka Fujiwara noted that although the share is small, Sakhalin’s two-day shipping time offers valuable supply security.

- The company imports around 0.2m mtpa from the project, which supplies more than half its output to Japanese buyers.

- Russia was Japan’s fourth-largest LNG supplier in 2024, accounting for 8.6% of national imports.

- Fujiwara warned that a sudden nationwide loss of Russian LNG — roughly 9% of total procurement by power and gas firms — would be difficult but said Osaka Gas has plans to manage its own exposure.

- The comments come amid rising pressure from G7 partners for Japan to cut Russian energy imports, with the EU set to ban Russian LNG from 2027 and the US urging Tokyo to phase out such purchases.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Oct23 $1.1515-25(E1.1bln), $1.1555-65(E1.3bln), $1.1575(E1.2bln), $1.1650(E1.1bln), $1.1670-80(E1.0bln), $1.1750-70(E2.8bln); Oct24 $1.1500-20(E1.2bln), $1.1635-50(E1.1bln); Oct27 $1.1520-35(E1.2bln), $1.1670-80(E1.1bln), $1.1700-10(E1.1bln)

- USD/JPY: Oct24 Y150.00($2.0bln), Y151.00-20($1.4bln)

- AUD/USD: Oct23 $0.6585-00(A$1.1bln); Oct24 $0.6450(A$1.6bln); Oct27 $0.6490(A$1.8bln)

RIKSBANK: Jansson Notes MonPol Will Look Through Temporary Tax Changes

Jansson speech summary here

- "There are strong reasons to believe that the currently elevated inflation is transitory. In September it was therefore possible to provide some additional interest rate support to economic activity without taking too much risk in terms of inflation."

- On the upcoming temporary reduction in food VAT, Jansson notes that "It is reasonable that in monetary policy we ‘look through’ this type of temporary tax change, in the same way as I believe the social partners will do in wage formation. But for us at the Riksbank it will be important to monitor how households' and companies' expectations and behaviour are affected, so that fluctuations in inflation that are temporary to begin with do not become more permanent."

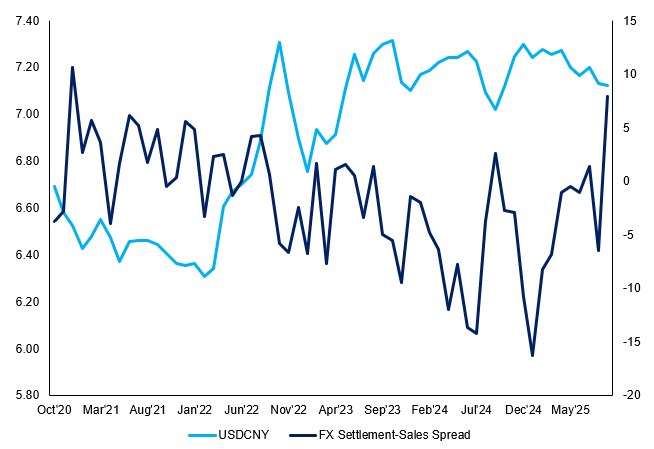

CHINA: SAFE Data Shows FX Settlement-Sales Spread at New High

Data on FX settlements from China's SAFE show the FX settlement ratio (a proxy for client willingness to settle FX) posting a sharp rise in September, to 71.2% from 61.2% in August. This is the highest level since August 2023 and is consistent with a sharp rise in exporters settling FX transactions in the month that covered USDCNY printing a new YTD low (Aug-Sept peak to trough was over 1.5%).

In contrast, the FX sales ratio (a proxy for client willingness to buy FX) was relatively stable at 63.3% (vs. August 67.7%), leading to a wider gap between settlement and sales in September. As a result, the FX settlement-sales spread has risen to a new 2025 high, and would be consistent with the weaker USD helping trigger the fastest pace of corporates closing out of FX positions relative to new FX exposure over the period.

Figure 1: FX Settlement/Sales Spread Highest of the Year

Source: MNI / SAFE / Bloomberg Finance L.P.

In addition, the SAFE data also shows an FX surplus totalling $51.1bln as a result of the rise of total FX purchases (up to $265bln from $212bln) outpacing the rise in FX sales (up to $214bln from $197bln).