OIL: Oil End of Day Summary: Crude Rises

Sep-26 18:18

Crude markets are on track for a strong weekly gain with Brent front month back above $70/bbl for the first time since early-August. A weaker dollar has supported crude’s gains today, alongside continued focus on Russian supply risks.

- WTI NOV 25 up 0.9% at 65.57$/bbl

- Baker Hughes US rig count: Oil: 424 (6) -The highest since July 11. This is down 60 rigs, or 12.4% on the year.

- EU leaders have been clear in their message to Russia that a NATO alliance would be ready to respond to repeated violations of European airspace by Russia, predominantly with drones. US Defense Secretary Pete Hegseth ordered an urgent meeting of top military commanders for an unusual meeting early next week.

- Indian official told Trump a significant reduction in oil imports from Russi would require purchases from sanctioned supplies Iran and Venezuela instead, Bloomberg said.

- Gulf Keystone Petroleum on Friday said it signed agreements with the KRG and Iraq's federal government to restart international crude exports from Kurdistan, with flows in the coming days.

- Norway’s DNO has no immediate plans to ship oil through the Iraq-Turkey pipeline that is said to restart Sep 27, and will continue to sell directly to Kurdistan, Reuters reported.

- Oil traders see OPEC+ agreeing to revises more production in November, Bloomberg Survey.

- OPEC+ has delivered about three quarters of the extra oil output it targeted since April, and the level may fall closer to half later this year as producers hit capacity limits: Reuters.

- Pemex reported exports of 500,203 b/d of crude oil in August, down 32% y/y, as its local refineries processed slightly more.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

COMMODITIES: Crude Finds Support, Gold Unchanged, Copper Declines

Aug-27 18:18

- Oil prices found support on Wednesday, supported by a slightly larger than expected US crude stock draw.

- A breakdown in E3 talks with Iran also added support earlier in the session, along with growing threats from the EU to further sanctions on Russia – though its options remain limited.

- WTI Oct 25 is up by 1.4% at $64.2/bbl.

- A bear cycle in WTI futures remains intact and the latest round of short-term gains appear corrective - for now.

- Initial support is at $61.99, the Jun 30 low, which has recently been breached, strengthening a bearish theme. Initial resistance to watch is at $66.56, the Aug 4 high.

- Elsewhere, spot gold is broadly unchanged on the session around $3,395/oz, after rallying off session lows following the IAEA-Iran headlines that flagged that monitors have not yet returned to damaged Iranian sites. Reports also suggested that Iran isn’t providing adequate access to inspectors.

- The medium-term trend condition for gold remains bullish, with initial resistance seen at $3,409.2, the Aug 8 high, followed by $3,439.0, the Aug 23 high.

- Meanwhile, copper has fallen by 0.9% to $449/lb today.

- Copper futures are in consolidation mode, with initial resistance at $488.17, the 50-day EMA. On the downside, a continuation lower would signal scope for a test of key support at $418.85, the Apr 7 low.

BONDS: EGBs-GILTS CASH CLOSE: OATs Extend Underperformance

Aug-27 18:10

OATs underperformed for a 3rd consecutive session as French political concerns lingered.

- Core EGBs and Gilts gained in morning trade, the latter after registering fresh cycle lows at the open, amid a bit of risk-off with equities sagging.

- Impactful data was limited, but regional politics were a key focus, with France's Sep 8 no-confidence vote continuing to weigh on OATs (the Dutch government survived a no-confidence motion of its own today, though this was expected).

- Outright OAT yields hit recent highs with 30Y seeing yields hit a 14-year high, as spreads to Bunds continued to widen.

- Trade turned more constructive going into the close, with OATs seemingly finding a footing, boosting Bunds and Gilts (as well as Treasuries).

- The belly outperformed on the German curve (despite a soft 7Y auction), with yields down throughout, while the UK curve saw yields drop more or less in parallel.

- Thursday's data schedule includes consumer and business confidence for Italy and the Eurozone, along with an appearance by the ECB's Rehn and the account of the July ECB meeting.

- The week's regional focus - the Eurozone August flash inflation round - technically starts Thursday (Belgium is due) but most attention will be on Friday's releases for Spain, France, Italy, and Germany. MNI's preview is here.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.3bps at 1.915%, 5-Yr is down 3.1bps at 2.237%, 10-Yr is down 2.3bps at 2.7%, and 30-Yr is down 1.3bps at 3.307%.

- UK: The 2-Yr yield is down 0.4bps at 3.964%, 5-Yr is down 0.6bps at 4.133%, 10-Yr is down 0.4bps at 4.736%, and 30-Yr is down 0.8bps at 5.6%.

- Italian BTP spread up 4bps at 87.3bps / French OAT up 5.1bps at 82.4bps

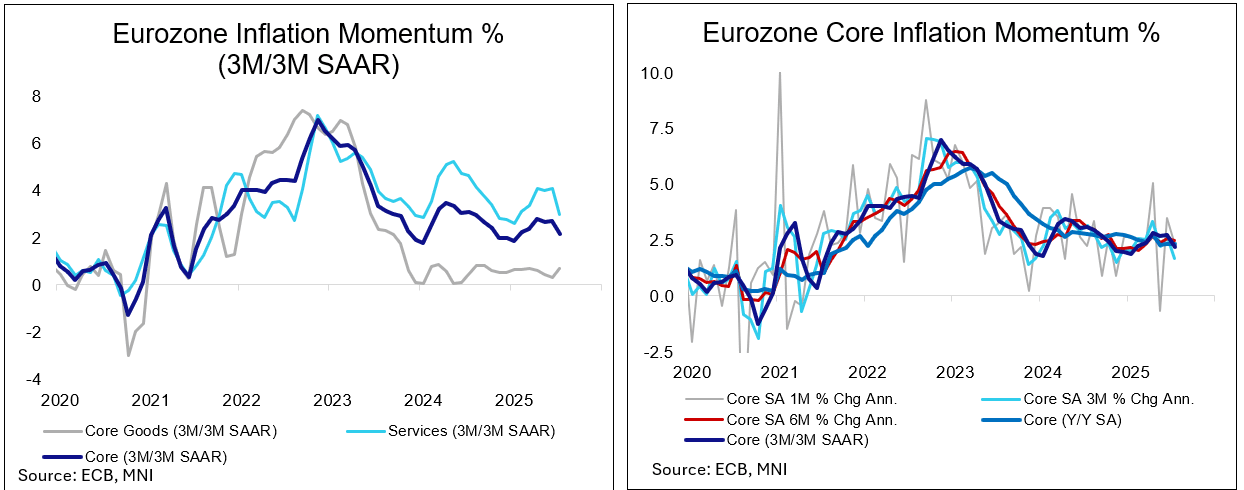

EUROPEAN INFLATION: MNI Eurozone Inflation Preview – August 2025

Aug-27 18:05

Full report here: LINK

Clear Downside Surprise Needed For Dovish Tilt

- The August Eurozone inflation round is split across two weeks, with the main prints of Spain, France, Italy, and Germany all scheduled for this Friday before the Netherlands and the Eurozone-wide figures follow next Tuesday.

- Analysts are looking for headline to pick up marginally to 2.1% Y/Y, while core inflation is expected to slow to 2.2%.

- Across categories, the main driver this time will be energy inflation base effects, putting upside pressure on headline. Analysts see the category around -1.6% Y/Y in August after -2.4% in July.

- Services inflation is expected to continue its downtrend seen this year, with consensus standing around 3.0-3.1% after 3.2% in July.

- Core goods meanwhile are seen to give away some of their July firmness, at 0.7% Y/Y, while views on food/alcohol/tobacco inflation are more mixed this time where consensus might be for a roughly unchanged print at 3.2%.