BONDS: NZGBS: Market Reverses Sell-Off After RBNZ Gov Comments

NZGBs closed slightly mixed and well off the session's yield highs after today's comments from RBNZ ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Oil Supply Questions Key to Gold's Next Moves

- Gold has traded in a range of US$4,517 - $4,420 Monday and is currently down -0.15% at US$4,488.

- Gold is currently trapped in a counter-intuitive cycle. Whilst the Middle East conflict usually drives gold higher, oil price gains are fueling massive inflation fears. This may force the Fed to pivot to a higher-for-longer stance, pushing Treasury yields up and making the non-yielding gold less attractive to investors.

- Investors are watching for further liquidity related selling. Institutional investors have sold gold (particularly ETFs) to raise cash to cover losses in other sectors. This week will see if that forced selling has finished or if more stop-losses drive gold below $4,400.

- The April 6 deadline for the re-opening of the Strait of Hormuz looms large with its continued closure having the potential for oil eye $130bbl, putting further pressure on yields and downward pressure on gold. The insertion of Houthi rebels into the conflict raises the question of security in the Red Sea.

- US economic data will show if high oil prices are beginning to impact the US economy and provide an insight into the likely direction for US rates. Markets are looking for signs that high fuel costs are stalling the 2026 industrial recovery via the ISM. If job growth (NFP) slows significantly while gas prices flirt with $4.00/gallon, the stagflation narrative will take over as traders fear a looming recession.

FOREX: USD - BBDXY Looking To Extend After Breaking Above 1215-1217

The BBDXY has had a range today of 1217.80 - 1221.27 in the Asia-Pac session; it is currently trading around 1218, -0.10%. The BBDXY broke above the 1215-1217 to extend above its recent range as risk starts to potentially turn Bearish. US 10 year yields above 4.40% and the NASDAQ accelerating its break below the pivotal support around 24000 saw Trump try and jaw-bone markets again this morning, with very limited effect. Cracks are starting to show and the USD is breaking higher in response. Should we enter a Bear market and this move lower in risk begins to accelerate I suspect the USD will then break higher. USD/EM could be most vulnerable, specifically against those currencies that have been bought for the Carry-Trade, though DM carry trades will also be impacted. On the day, watch for this break higher to hold and potentially regain upward momentum. I continue to be skewed toward fading dips while uncertainty remains high and risk is under pressure. First support is back toward 1214-1216 where I suspect buyers should reemerge looking for a retest of the pivotal 1230-1240 area.

- EUR/USD - Asian range 1.1488-1.1521, Asia is currently trading 1.1520. The pair traded heavily into the weekend but as of yet has been unable to break back below the 1.1500 support. The pair remains above its pivotal support in the 1.14-1.15 area for now but I still prefer to be fading bounces as Europe looks to be at the epicenter of the global supply issues. On the day, I would be looking for sellers back toward 1.1540-1.1570 initially, expecting a challenge of the support around 1.1500. A sustained break below 1.1500 and the market will again be looking to test the important 1.1400 area. Some Corporate month-end demand for USD’s could be seen today which could potentially add to the EUR headwinds. Some decent optionality though between 1.1450 & 1.1500.

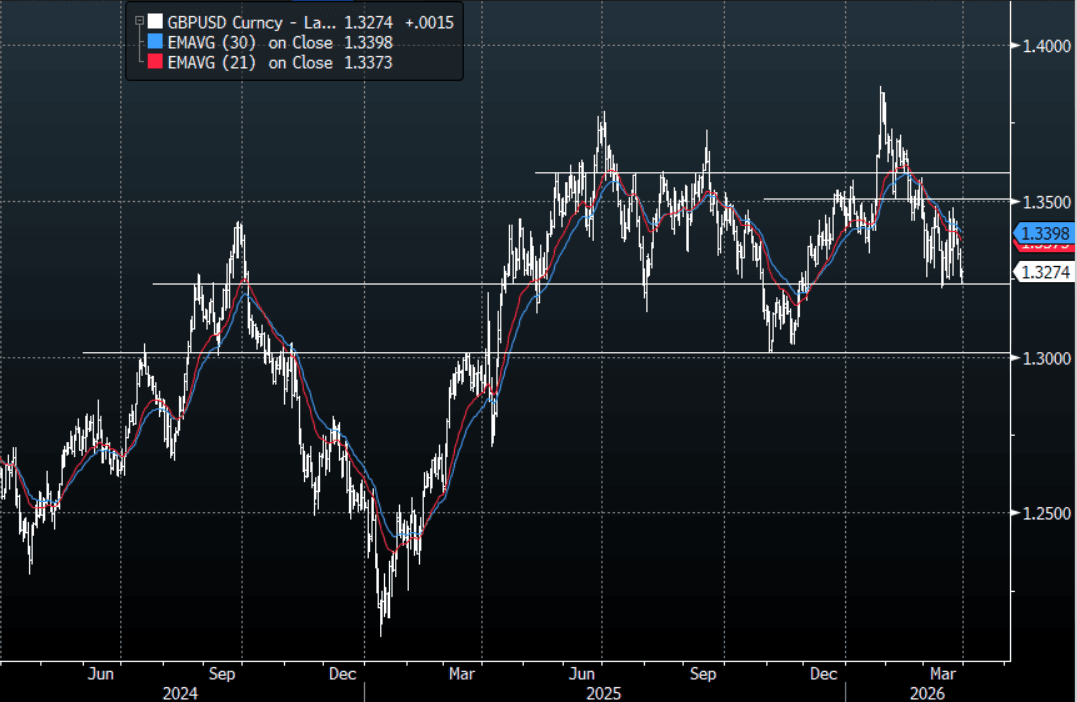

- GBP/USD - Asian range 1.3233-1.3277, Asia is currently dealing around 1.3275. GBP seems to be trading heavily towards its lows, albeit still within its recent range. The GBP is trying to put a top potentially in place, I prefer to be skewed to fade rallies while risk continues to trade on the backfoot. On the day, the pair looks to be in a choppy 1.3200-1.3500 range with the bears looking for a sustained move back below 1.3200-1.3250 to see the move lower regather momentum.

- Data/Events: ECB’s Stournaras speaks, UK Feb. Mortgage Approvals, Eurozone March Confidence, Germany March CPI, Fed’s Powell speaks, Fed’s Williams speaks, G7 finance and energy ministers and central bankers hold an online call.

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Front End Yields Down Sharply, Govt Cuts Fuel Taxes

The bias has for firmer Aussie bond futures, consistent with themes in the US and Japan, as Monday trade unfolded. Initially focused in the front end, 10yr futures are now up for the session. YM was last 94.90, +3bps, up from earlier lows of 94.78. Dips under 94.80 remain supported for this 10yr benchmark. 3yr is up 9.5bps to 95.25 (earlier lows were at 95.085). In the cash ACGB space, we are around 1-8bps weaker, with the front end leading. Growth concerns, risk aversion, from the longer the Iran conflict persists, is being cited as support for front end bonds globally.

- For the ACGB 3yr yield, recent highs are above 4.80%, while current levels around 4.72% are still above all key EMAs (the 20-day resting near 4.59%). For the 10yr moves above 5.15% haven't been sustained, while current levels around 5.07% remain comfortably above the 20-day EMA (4.95%).

- The government announced it will halve the fuel tax to cut local fuel prices. This will cost around A$2.55bn and lower the CPI by 0.5ppts per the Australian Treasury.

- Westpac has revised its RBA forecast. The local bank notes: "We have revised our view of the outlook for RBA policy, adding two further hikes to the near-term profile and pushing out the eventual reversal. We now expect 25bp rate hikes at the 16 June and 11 August decisions, in addition to the 25bp hike we already expected at the May meeting. The peak for the cash rate is now expected to be 4.85%." This reflects a longer return assumed for oil supplies, and stronger pass through of higher fuel prices to other goods and services.

- The AU 3/10s curve is steeper to +35bps today, while the AU-US 10yr spread is slightly wider at +68bps, but remains within recent ranges.

- Tomorrow, we get the RBA minutes from the March policy meeting.