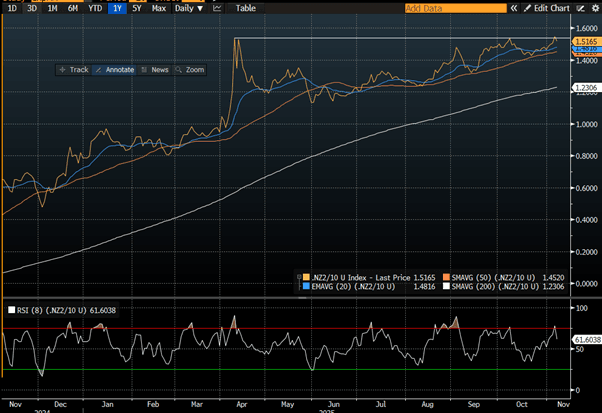

BONDS: NZGBS: Curve Steepener Takes A Breather

Nov-07 04:01

NZGBs closed showing a bull-flattener, with benchmark yields 2-5bps lower.

- Today's move sees the 2/10 curve pull back from cycle highs, just shy of the 2021 high. (see chart)

- The NZ-US 10-year yield differential was unchanged on the day at -1bp, while the NZ-AU differential was 3bps narrower at -26bps.

- Swap rates closed 3-4bps lower.

- RBNZ dated OIS pricing closed little changed across meetings. 28bps of easing is priced for November, with a cumulative 37bps by February 2026.

- Over the past three weeks, year-end rate expectations in NZ — along with Canada — have been the clear outperformers within the $-bloc, easing slightly by 2bps. In contrast, year-end expectations for policy rates have risen by 15bps in the US and 25bps in Australia over the same period.

- On Monday, the local calendar will be empty. The next release of note will be the RBNZ's Inflation Expectations data on Tuesday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Former BoJ Chief Economist On The Policy Rate Outlook

Oct-08 04:00

A former BOJ chief economist shares his policy rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

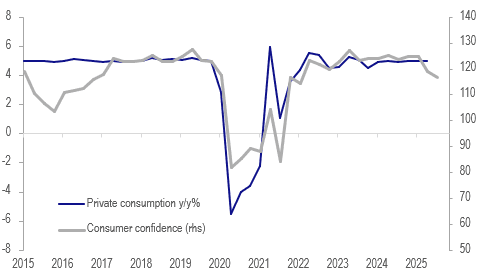

INDONESIA: Confidence Signals Slower Q3 Consumption Growth & More Easing

Oct-08 03:48

Indonesian consumer confidence fell for a second straight month to 115.0 in September from 117.2, the lowest since April 2022. There were major protests at the end of August regarding economic pressures and generous housing subsidies for politicians, which were overturned. The respected finance minister Indrawati was also replaced and dissent restricted. The issues appear to be still weighing on sentiment.

- Private consumption growth been steady around 5% for around two years but the 1.8% q/q drop in Q3 average consumer confidence is signalling that it slowed last quarter.

Indonesia private consumption

Source: MNI - Market News/LSEG

- Bank Indonesia surprisingly cut rates for the third consecutive month in September signalling that it has become more focussed on growth rather than the currency and so further easing on 22 October is possible given the softer consumption picture.

- BI's September statement added the phrase "joint efforts to stimulate economic growth", suggesting that it may be supporting government policy. It expects H2 2025 to improve due to the "strengthening policy synergy between Bank Indonesia and the Government".

- September consumer confidence was pressured by a 4 point drop in current incomes to 112.9 and 1 point in employment to 92.0. Thus it is unsurprising that durables purchases fell almost 2 points to 103.2. Expectations were 2 points lower to 127.2 driven by incomes and business but employment was slightly higher.

BONDS: Bull-Steepener After RBNZ Cuts By 50bp

Oct-08 03:33

NZGBs closed 4-7bps richer after the RBNZ cut 50bps to 2.50%.

- The MPC discussed cutting the OCR by 25bp or 50bp and all members agreed the latter was appropriate given material spare capacity in the economy. Given that this is likely to persist for some time and that while the economy has begun to recover it remains lacklustre, further cuts bringing policy into stimulatory territory are likely. In line with this it said that “the Committee remains open to further reductions in the OCR”.

- The MPC’s inflation concern appeared to shift this month. In August, it said it could ease policy further “if medium-term inflation pressures continued to ease as expected”, whereas this month it seemed more concerned with undershooting the target mid-point, stating it “remains open to further reductions … for inflation to settle sustainably” near the 2% mid-point over the medium-term.

- Swap rates closed 4-6bps lower on the day.

- RBNZ dated OIS pricing closed 9-15bps softer across meetings. 34bps of easing had been priced for this meeting. A cumulative 62bps of easing had been priced by November 2025 versus 75bps now (including today’s move).

- Tomorrow, the local calendar will see the NZ Government 12-Month Financial Statements.

- The NZ Treasury also plans to sell NZ$275mn of the 1.50% May-31 bond and NZ$175mn of the 4.25% May-34 bond.