BONDS: NZGB Yields Follow US Yields Lower, NZ Consumer Confidence Rises Further

NZGB yields are tracking lower in the first part of Friday dealings, off 1-2bps, with the back end leading. This follows a weaker US Tsy yield backdrop on Thursday (off around 2.5-3.5bps) post weaker CPI data (although the data is noisy and difficult to interpret). The NZGB 2yr yield is off around 1bps to under 2.70%, which is back close to Dec lows. Further downside could bring the 2.60% region back into focus, where we tracked in late Nov. Still, data outcomes are mostly on the improve, pointing to an on hold outlook for the RBNZ in the first part of 2026. The 10yr NZGB is off 2bps, to be around 4.40%.

- The NZ-US 10yr spread is around +30bps, so off earlier Dec highs (near +39bps) but little changed over the past week and still holding the bulk of its recent gains . The NZ 2/10s curve is slightly flatter at +170bps.

- The NZ 2yr swap rate (NDSO) is down further at 2.73%, but comfortably above earlier Dec lows sub 2.60%.

- Earlier data showed the ANZ consumer sentiment reading rising above 100.0, reaching fresh highs since late 2021. This points to an improving spending outlook/backdrop as we progress into 2026.

- Nov trade data showed a narrowing in the trade deficit to -NZD163mn (from a revised -NZD1598mln in Oct).

- Later on we get ANZ business confidence/activity for Dec.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Oil Rallies On Tough EU Comments, US Stock Build May Pressure Prices

Trading in recent months has been characterised by concerns over excess supply pushing prices lower and an expansion of sanctions on Russia driving them higher. Prices rose on Tuesday following comments from EU foreign minister Kallas that increased expectations of stricter restrictions on Russia. The announcement of new US/EU sanctions in October pressured Russia’s Urals benchmark and it is down further this week. Reports of another US oil inventory build may pressure prices on Wednesday.

- Kallas said that Russia’s actions against the EU constitute “state-sponsored terrorism” prompting expectations of further sanctions. There have been numerous incursions of airspace over recent weeks.

- WTI rose 1.3% to $60.69/bbl after a high of $60.93. It had traded below $60 through Tuesday’s APAC and early European sessions before breaking above. Initial resistance is at $62.59 with the bear trigger at $55.96.

- Brent is up 0.9% to $64.78/bbl off the intraday peak of $65.10, holding below resistance at $65.95. The bear trigger is at $59.97.

- Ukrainian attacks on Russian refineries and sanctions on Russian majors Rosneft and Lukoil, which are due to be imposed on Friday, have increased concerns over diesel supplies driving prices higher. ICE gasoil prices rose 6.4% yesterday. The restrictions already appear to be having an effect with some Asian purchases out on hold and ICE reporting that physical diesel deliveries will have to be from non-Russian crude.

- Bloomberg reported that there was a US crude inventory build of 4.4mn barrels last week after an increase the week before, according to those familiar with the API data. Product stocks were higher too with gasoline +1.5mn and distillate +600k. The official EIA data is out on Wednesday.

OIL: Industry Data Show US Crude & Product Stock Builds

Bloomberg reported that there was a US crude inventory build of 4.4mn barrels last week after an increase the week before, but a drop of 800k at Cushing, according to those familiar with the API data. Product stocks were higher too with gasoline +1.5mn and distillate +600k. The official EIA data is out on Wednesday and showed a 6.4mn barrel build the previous week.

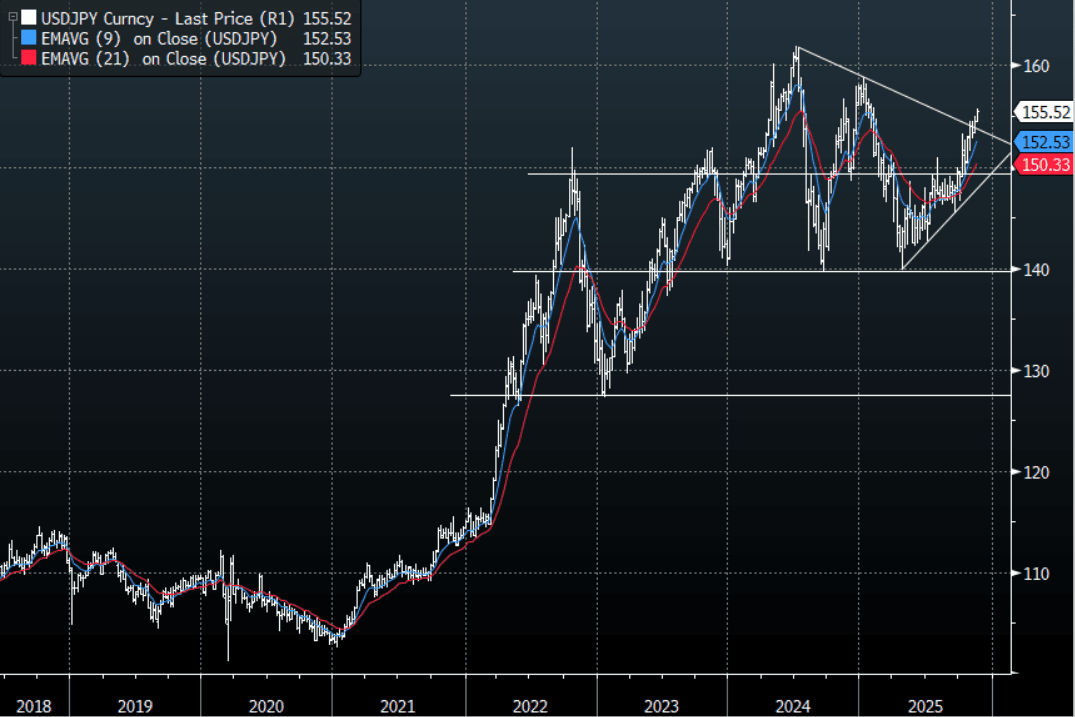

JPY: USD/JPY - Consolidates Break Above 155.00

The overnight range was 154.87 - 155.73, Asia is currently trading around 155.50. The pair was again quietly bid all day yesterday consolidating its recent break above 155. The move lower in risk did not bring the usual bout of Yen buying as its safe haven status begins to be questioned. Usd/Jpy I suspect will remain well supported on dips as the market remains wary of the new leadership policies together with a reticence to hike rates. I will be watching again for dips in the Asian session back toward 154.80-155.00 to be supported on dips initially. This break should now turn the markets focus back toward 160, much to the displeasure of the MOF/BOJ.

- Bloomberg is reporting, “Governor Kazuo Ueda told Prime Minister Sanae Takaichi that the Bank of Japan is in the process of slowly dialing back its easing support for the economy, signaling his unshaken intention to carefully raise rates.”

- “Yen Slide Signals Japan Losing Control of Its Policy Mix. The yen’s slide is accelerating, with USD/JPY breaking above 155 for the first time since January as fiscal concerns in Tokyo battle with stubbornly easy monetary policy.” {NSN T5XVRCGPL3WG <GO>} - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.00($1.26b). Upcoming Close Strikes : 155.00($1.49b Nov 20), 150.00{$1.3b Nov 20) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 97 Points

- Data/Event : Core Machine Orders

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P