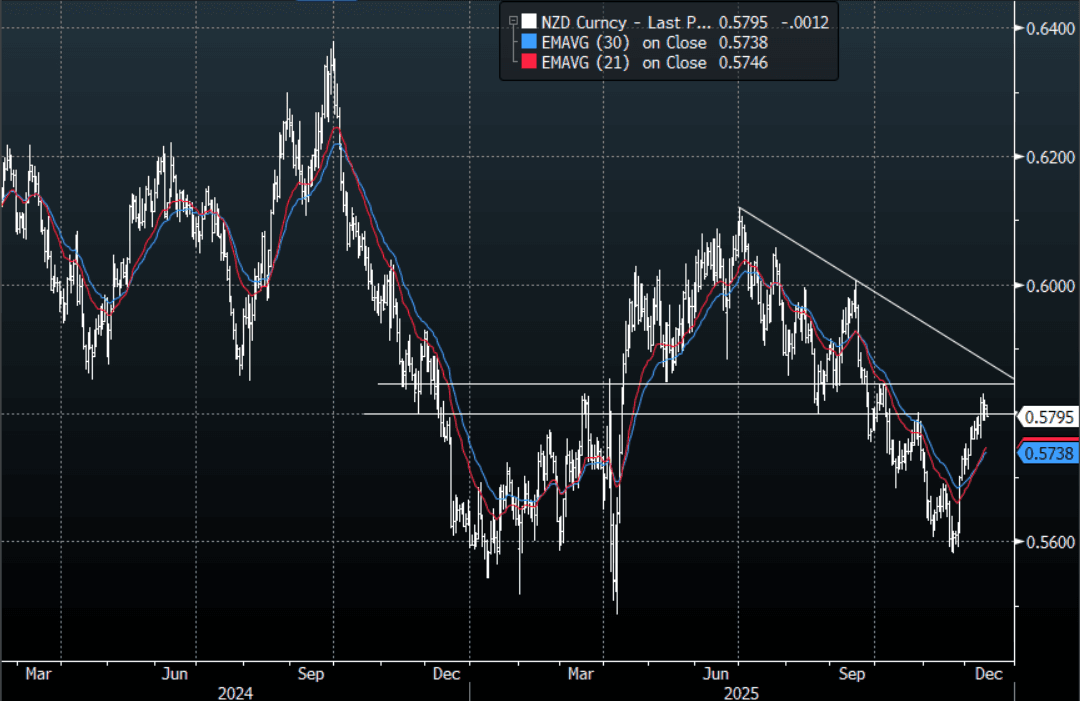

NZD: NZD/USD - Stalls Above 0.5800 For Now, Support Seen Below 0.5750

The NZD/USD had a range Friday night of 0.5788 - 0.5821, Asia is trading around 0.5795. The US stock market wobbled on Friday as AI concerns came back to the fore and US yields in the long end tick back up. This saw the USD’s decline stall but it has not bounced, yet. The NZD’s momentum higher looks to be stalling above 0.5800 for now. On the day, watch how risk starts the week with first support on the day around the 0.5780-90 area if this does not hold it could signal a retracement to the more important 0.5730/0.5760 area. I have this area between 0.5800-0.5900 as being decent longer-term resistance and it has provided some early headwinds for now.

- (Bloomberg Economics) - “New Zealand’s November price data are likely to show inflation still above the Reserve Bank’s 1%-3% target band but drifting closer.” {NSN T7507DKJH6V5 <GO>}

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5650(NZD410m Dec 18 ), 0.5690(NZD531m Dec 18 ), 0.5860(NZD471m Dec 18 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 36 Points

- Data/Event: Performance Services Index

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

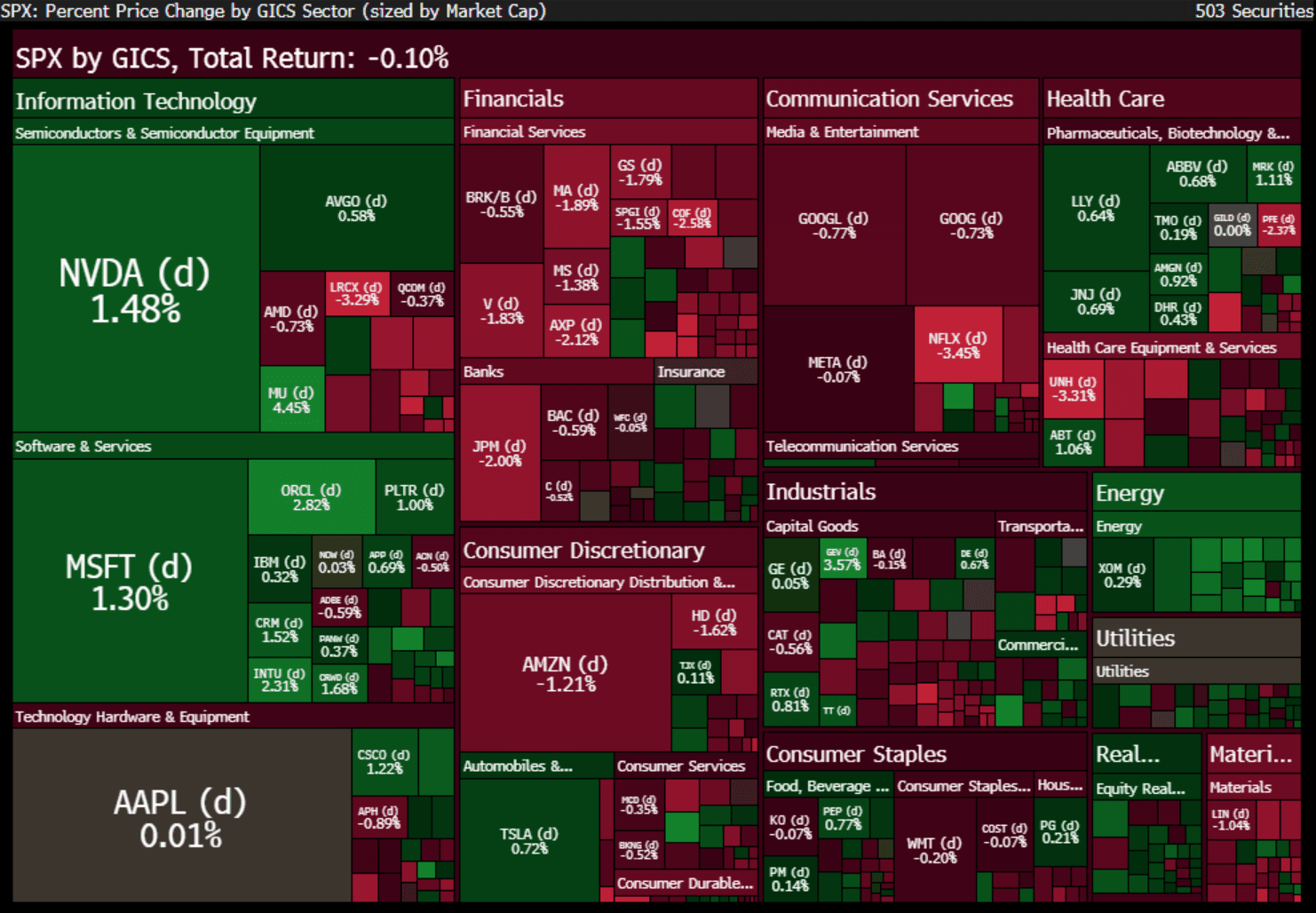

US STOCKS CLOSE: Equities Recover From Intraday Pullback

Equities recovered from a sharp intraday sell-off to close roughly flat Friday, with the Nasdaq and S&P 500 almost unchanged but the the Dow Jones retracing 0.7% after Thursday's outperformance.

- Reeling from concerns over AI-related valuations and waning prospects for a December Fed cut, the S&P fell as much as 1.3% (6,646.87) which would have marked the lowest close in a month, but bounced to trade roughly flat on the session.

- Energy (+1.4%) and tech (0.7%) outperformed on the S&P 500, with losses led by financials (-1.0%) and materials (-1.2%).

- Megacaps NVidia (+1.6%) and Microsoft (+1.3%) were the biggest upside contributors, offsetting downside for Google (-0.7%), Netflix (-3.4%) and Amazon (-1.1%) in the tech/communications space, while JPM (-1.8%), Visa (-1.7%) and Mastercard (-1.8%) pulled down financials.

- Latest futures levels: Dow Jones mini down 325 pts or -0.68% at 47253, S&P 500 mini down 6.25 pts or -0.09% at 6762.5, NASDAQ mini down 13.75 pts or -0.05% at 25125.25.

USDCAD TECHS: Bear Theme Inside A Bull Channel

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4167 50.0% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.4140/62 High Nov 5 / Channel top drawn from Jul 23 low

- RES 1: 1.4057 High Nov 10

- PRICE: 1.4020 @ 16:26 GMT Nov 14

- SUP 1: 1.3985 Low Nov 13

- SUP 2: 1.3962 50-day EMA

- SUP 3: 1.3888 Low Oct 29 and a key support

- SUP 4: 1.3886 Bull channel base drawn from the Jul 23 low

A bear theme in USDCAD remains intact for now following recent weakness. Price action is trading inside a bull channel drawn from the Jul 23 low. The top of the channel - currently at 1.4162 - provided a firm resistance on Nov 11, highlighting scope for a bear extension towards the base of the channel at 1.3886. Initial key support to watch lies at 1.3962, the 50-day EMA. For bulls, a break of the channel top is required to confirm a resumption of the uptrend.

US TSYS: Softer To End The Week As Intraday Rally Reverses

Treasuries softened to end the week, with early gains dissipating and the cash curve ending bear steeper.

- An overnight selloff in Gilts related to UK fiscal concerns spilled over lightly into the US in early trade, but maintained a cautious tone for Treasuries following on from Fed commentary earlier in the week dampening enthusiasm for a December rate cut as well as weak long-end Treasury auctions.

- However a pullback in equities was enough to provide a safe-haven bid in equities which saw TY futures briefly touch the best levels of November so far. That would reverse however, with equities finding their footing and turning higher for the day and returning Treasuries to early morning levels.

- With the federal government shutdown now over, some postponed data is starting to come into view, with the BLS scheduling September's delayed nonfarm payrolls report for next Thursday, and the Census Bureau set to publish some delayed August data next week.

- Still, there's no official word on the fate of the October CPI release, which looks very likely to be cancelled altogether, or the date of the October employment report's publication (which is likely to see an establishment survey but not a household one).

- Against this backdrop, Friday's Fed commentary (with the usual exception of Gov Miran calling for further easing in December) was roundly hawkish, with Dallas's Logan and KC's Schmid reiterating their opposition to a December rate cut, largely out of concern over entrenched inflation. A December cut remained around 50/50 priced.

- Latest levels: The 2-Yr yield is up 2.1bps at 3.6121%, 5-Yr is up 2.6bps at 3.7327%, 10-Yr is up 2.7bps at 4.1463%, and 30-Yr is up 3.4bps at 4.7458%. Dec 10-Yr futures (TY) down 7.5/32 at 112-17 (L: 112-16 / H: 113-04.5)

- Along with the newly-rescheduled data mentioned above, next week's calendar includes the October FOMC minutes (we're watching for color on the debate over whether to ease any further) and flash November PMI data.