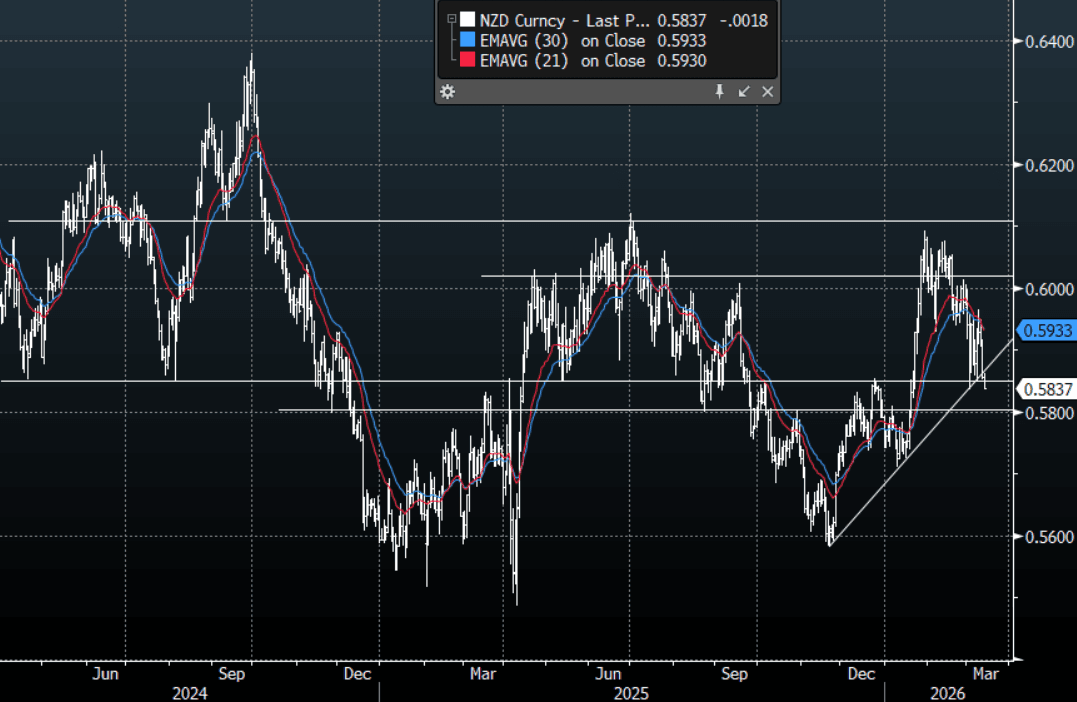

NZD: NZD/USD - Looking To Challenge Pivotal 0.5800-0.5850 Support

The NZD/USD had a range today of 0.5836-0.5862 in the Asia-Pac session, it is currently trading around 0.5836, -0.30%. Risk aversion seems to be building now and the NZD fell away very quickly in the New York session when US stocks turned lower. The USD is bouncing in this scenario and the NZD is now pressing the lows of its recent messy 0.5840-0.6020 range. The NZD has traded with a heavy bias consistently throughout this conflict and a sustained break below 0.5800-0.5850 could potentially see the move begin to accelerate. On the day, I suspect sellers could return back toward the 0.5890-0.5920 area and then toward 0.6000, looking for the pair to challenge lower at some point.

- MNI AU - Feb PMI Elevated But BNZ Notes Note Too Early Assess Iran Impact: The New Zealand Feb BNZ-Business NZ PMI (manufacturing) edged down a touch to 55.0 (from a revised 55.1 in Jan, originally reported as 55.2). The PMI is still pointing to better y/y GDP momentum in to early 2026. BNZ via BBG notes: "Subcomponents provide further evidence that the manufacturing sector started 2026 well. The new orders and production indexes are meaningfully above their long run-averages: BNZ" but adds: "Recent economic data have taken a backseat relative to the conflict in Middle East. "It is too early for the PMI to capture any of these impacts."

- Bloomberg - “Traders are now predicting a Fed rate cut in mid-2027, with Goldman pushing back its reduction call to September from June.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5790(NZD310m). Upcoming Close Strikes : none - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 64 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

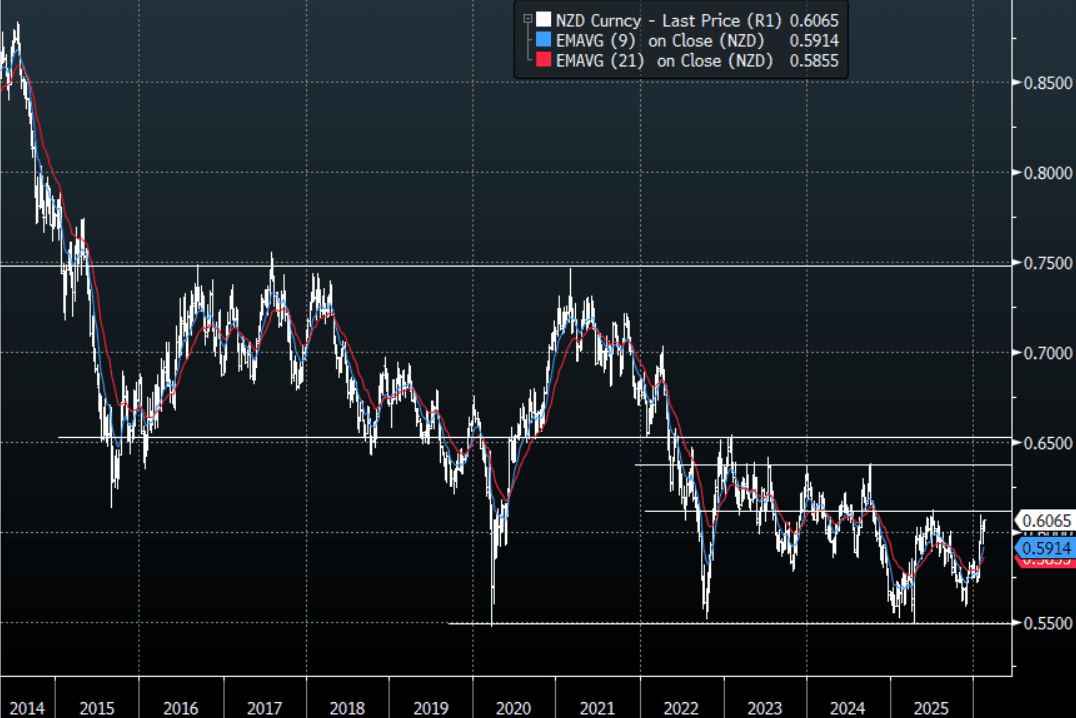

NZD: NZD/USD - Dragged Back Toward 0.6100 As The USD Gets Hit

The NZD/USD had a range today of 0.6037-0.6066 in the Asia-Pac session, it is currently trading around 0.6065, +0.33%. The NZD is pushing above its overnight highs that saw its momentum stall as the USD trades poorly into NFP. On the day, the NZD bulls will be hoping the pair can maintain its upward momentum to test the pivotal 0.6100 area. The first support is back toward 0.6025-0.6045 and then the 0.5900-0.5950 area. A sustained break back above 0.6100 could potentially open up a move back toward the 0.6400-0.6600 area and then beyond.

- MNI - Westpac Expects RBNZ To Raise Rates More Quickly In 2027: Westpac now expects the RBNZ to raise rates more quickly in 2027 (as spare capacity is exhausted). It maintains the start of the hiking cycle is expected in Dec of this year. The next RBNZ meeting is on Feb 18, next Wednesday. Market pricing, per OIS markets, is very flat for the first few meetings this year (around 2.25%, the current target rate). A full 25bps hike is priced by around the Oct meeting this year.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5900(NZD301m Feb16), 0.6200(NZD430m Feb 16) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 61 Points

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

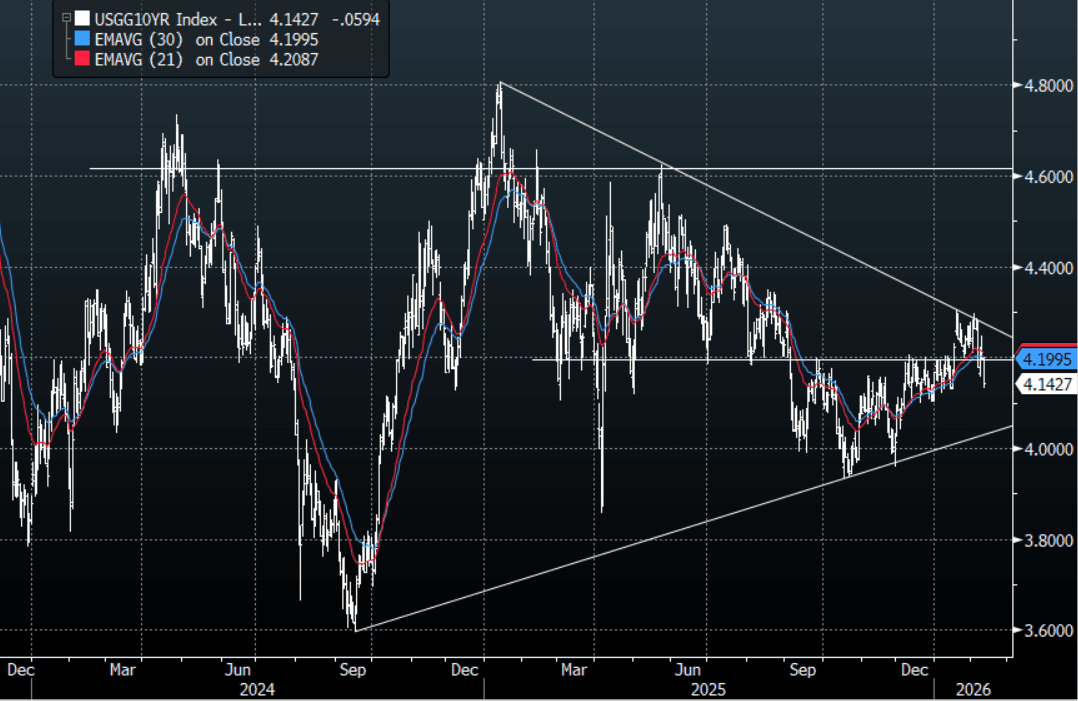

JPY: USD/JPY - Continues To Drift Lower As The USD Trades Poorly Into NFP

The USD/JPY range today has been 153.51 - 154.52 in the Asia-Pac session, it is currently trading around 153.55, -0.55%. USD/JPY could not bounce at all and was back under pressure from the open and has remained so all through our session. The price action on Monday in response to the election outcome showed it was mostly priced in, and we have seen some “buy the rumour, sell the fact” play out. I thought we would see better demand back toward the 155.00 area initially but this move in US yields is causing the Yen shorts some angst. This price action does look messy but I still believe dips back toward the 149-152 will probably provide solid support again should we see it, until then it looks like we chop around albeit with a heavy tone as we await tonight's US labour data which will directly impact that move in US yields. On the day, the first resistance is back towards 154.75-155.15 and then the 155.80-156.20 area as the market pares back its USD longs and looks for another base to from from which to move higher again.

- “Deutsche Bank strategists said they’re no longer bearish on the yen after PM Sanae Takaichi’s election victory.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 156.50($1.16b), 156.60($550mm). Upcoming Close Strikes : 158.50($1.57b Feb 13), 159.00($1.91b Feb 13),160.00($3.06b Feb 13) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 154 Points

Fig 1 : US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Richer Ahead Of US NFP, Stronger Demand Drove Hike - RBA Hauser

ACGBs (YM +3.0 & XM +6.5) are stronger.

- MNI: The Reserve Bank of Australia’s 25bp February hike to 3.85% reflected stronger global growth, looser financial conditions and firmer private demand relative to supply, Deputy Governor Andrew Hauser said.

- There has no cash US tsys dealings in today's Asia-Pac session, with Japan out on holiday.

- All focus turns to today's US employment data. Monthly payroll growth is currently expected at 70k in January for a slight acceleration from the 50k in December and 56k in November.

- Cash ACGBs are 2-5bps richer, with the 3/10 curve flatter.

- The latest ACGB April 2037 auction attracted solid demand, with the weighted average yield printing 0.68bps through prevailing mid-yields.

- Moreover, the cover ratio jumped sharply to 4.1429x from 3.4933x at the previous auction. The AOFM also plans to sell A$1000mn of the 2.50% 21 May 2030 bond on Friday.

- The bills strip has bull-flattened, with pricing flat to +3 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 15% for March to 93% by June and 146% by December 2026.

- Tomorrow, the local calendar will see Consumer Inflation Expectation data alongside the RBA’s Senate Testimony and RBA Hunter’s Speech.

Bloomberg Finance LP