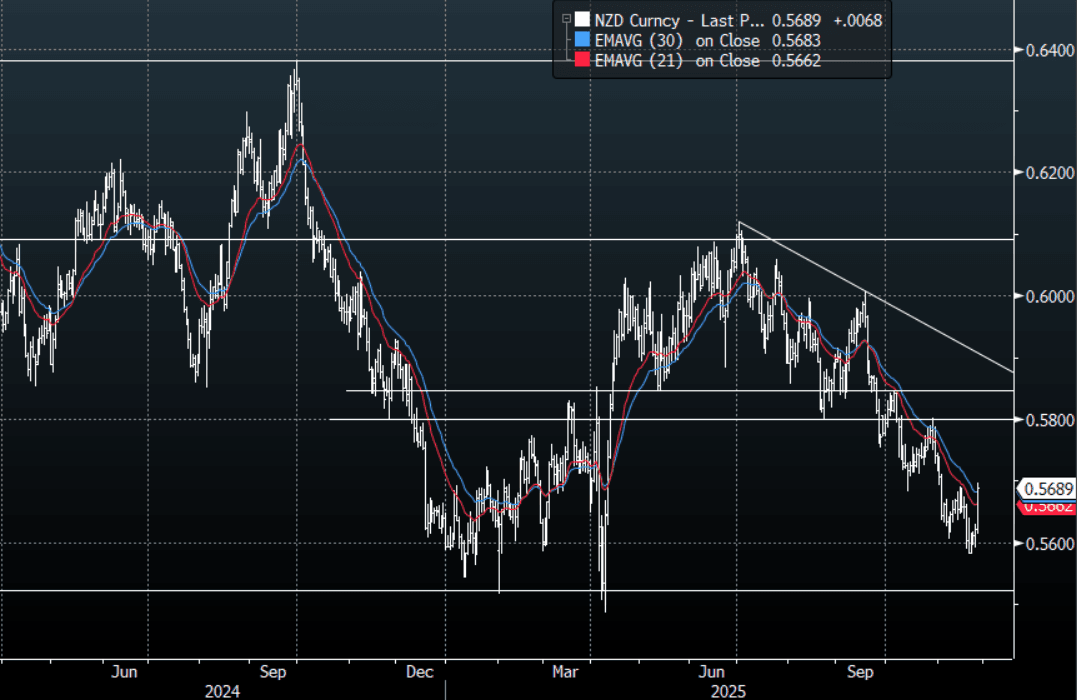

NZD: NZD/USD - A Hawkish Cut Squeezes A Short NZD Market

The NZD/USD had a range today of 0.5613 - 0.5697 in the Asia-Pac session, going into the London open trading around 0.5690, +1.20%. The NZD/USD has exploded higher in reaction to the RBNZ’s suggestion they could be on hold now If the economy develops close to expectations. I had been wary of positioning going into this and we could see a paring back of these underweights in the short term. On the day, look for dips back towards 0.5650-0.5670 to now find buyers looking for a sustained move above 0.5700 which could potentially signal a more significant pullback toward the 0.5800-0.5850 resistance area.

- MNI AU - RBNZ: RBNZ Maintains Easing Bias, In Good Position Going Into 2026. In his final press conference, RBNZ Governor Hawkesby noted that the 2.20% OCR projection in Q2 2026 signals that if rates are to change they are more likely to fall than rise. While in 2027, they are more likely to rise than fall. The OCR path is consistent though with rates on hold as the MPC sees risks around its central case as balanced. So if the economic recovery and inflation develop as the RBNZ expects over the coming months, then it may leave rates on hold at 2.25% at the next meeting on 18 February.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5670(NZD788m). Upcoming Close Strikes : 0.5550(NZD300m Nov 28), 0.5650(NZD300m Nov 28) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 48 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

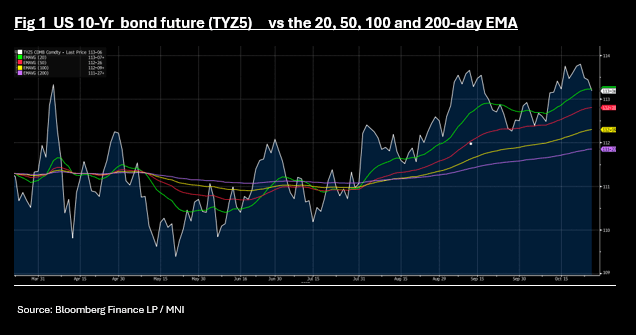

US TSYS: 10-Yr Bond Future Breaks Below Key Technical

The morning's sell off moderated into the afternoon, but the damage was done with bond futures all lower. TYZ5 is down -08 at 113-05+, breaking below the 20-day EMA of 113-07+

Cash bonds remain weak with yields across the curve 2-3bps higher.

- The US 2-Yr is at 3.51% (+2.5bps today)

- The US 5-Yr is at 3.63% (+3bps today)

- The 10-Yr is at 4.03% (+3bps today)

- The 30-Yr is at 4.62% (+3bps) today.

Tonight sees multiple bill issuance, 2-Yr notes, 5-Yr notes as the key auctions for markets.

Key focus for data tonight is Durable Goods, Dallas Fed Mfg, and Capital Goods orders.

JGBS: Risk On Pauses Long End Yield Slide, 30yr JGB Yield Around 100-day EMA

JGB futures are holding negative, but downside sub 136.00 has been limited so far. We were last 135.96, -.18 versus settlement levels. We are still above key support levels (135.61 from Oct 8). Near term focus will be on global bond futures weakness, as markets digest positive weekend news around de-escalating US-China trade tensions. US 10yr futures are down 8 ticks to 113-06, sub its 20-day EMA support point.

- JGB yields are a touch higher, led by the belly of the curve. 5-10yr tenors up a 1bps or more. The 10yr outright yield was last near 1.67%. 20-40yr tenors are close to flat, but the recent downtrend has stalled today. The 30yr yield holding at 3.07%, which is around the 100-day EMA support point. The 2/30s JGB curve is steady at +213bps.

- We had the PPI services earlier, which ticked up to 3.0% y/y, from 2.7% prior, implying some headline CPI upside risks. Still, while some hawkish BoJ board members feel the price target has been achieved, this doesn't appear to be a core board viewpoint yet. The meeting outcome is due Thursday, with no change expected and focus on hike risks for Dec or Q1 next year.

- The local data calendar is empty tomorrow, with debt supply not returning until Friday when a 2y sale is due.

AUSSIE BONDS: Weaker Futures, Risk On Weighs, RBA's Bullock May Signal Caution

Aussie bond futures are holding weaker, but slightly up from session lows. 10yr futures (XM) were last 95.81, off 3.5bps (session lows rest at 95.79), while 3yr futures were 96.58 off 4bps (session lows at 96.57). After the initial gap lower at the open, as risk on was dominated by positive US-China trade sentiment from the weekend, we have largely been range bound. ACGB yields are off earlier highs, around +3.5-4.5bps firmer, outperforming US Tsys so far today (benchmarks

- Domestic news flow has been light, as markets await an RBA Bullock Fireside chat latter, at the ABE dinner (7:15pm AEDT). This is the final RBA speak before next Tuesday's monetary policy outcome. It may be the case Bullock stays quite non-committal around easing risks at that meeting (in Bullock's style of not ruling anything in or out). Market pricing is delicately poised, with a 25bps cut around 60% priced per OIS dated RBA contracts for the Nov meet.

- Monetary policy centered questions this evening may focus on this recent disappointing jobs data but Bullock has said previously that given volatility it is best to focus on the 3-month average of the unemployment rate which was consistent with a gradual easing in conditions.

- The 3y ACGB yield is trying to recapture the 3.40% handle, with after the earlier break in Oct out of the 3.40-3.60% range to the downside. The 10yr is short is potential resistance around 4.20%.

- The AU-US 10yr spread is +15bps, so within recent ranges. The bias would be for higher levels in this spread if we see further risk on related to US-China trade outcomes.

- On the data front, things are quiet until Wednesday's Q3 CPI print.