STIR: No Impact From Data, Bulk Of Dovish Fed Move That Followed Williams Holds

The U.S. front end is essentially unmoved by the recent run of data (flash PMIs and final UoM sentiment reading).

- Fed Funds futures show 17bp of easing for December vs. ~9bp ahead of this morning’s comments from NY Fed President Williams (in which he provided uncharacteristically indicative guidance, pointing to a cut at the December FOMC).

- 26.5bp of easing showing through January, 36.5bp through March, 45.5bp through April and 61bp through June.

- Meanwhile SOFR futures are flat to +5.5 with implied terminal rates at 3.00% last. in the middle of the recent 2.80-3.20% multi-week range.

- A recovery in risk appetite (albeit at least partially triggered by Williams’ comments) has countered some of the dovish move.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

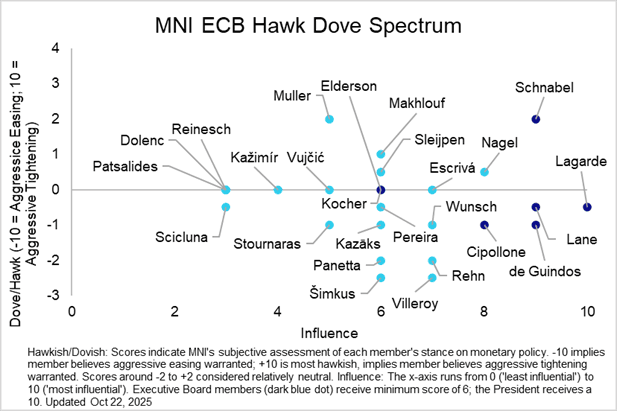

ECB: ECB Speak Wrap (Oct 6 - Oct 22)

The IMF/World Bank meetings in Washington DC brought a significant amount of commentary from ECB Governing Council members. Save for some nuances in views on both the dovish and hawkish end of the spectrum, the overwhelming message was that policy remains in a “good place”. The bar to another rate cut appears to be high, though policymakers haven’t fully closed the door to such a move, in line with the data-dependent and meeting-by-meeting approach.

An unchanged rate decision at next week’s October decision seems assured, with major guidance changes also unlikely. EUR STIR markets will probably pay more attention to next week’s swathe of regional data, including Q3 flash GDP and October flash inflation.

As usual, the full summary of ECBspeak by date, policymaker and topic are in this publication. In this iteration, we also launch our MNI’s ECB Hawk/Dove matrix.

US 10YR FUTURE TECHS: (Z5) Bull Cycle Intact

- RES 4: 115-00+ High Oct 1 ‘24 (cont)

- RES 3: 114-21+ 1.00 proi of the Aug 18 - Sep 11 - 25 price swing

- RES 2: 114-10 High Apr 7 (cont) and a key resistance

- RES 1: 114-02 High Oct 17

- PRICE: 113-21 @ 16:01 BST Oct 22

- SUP 1: 113-03+ 20-day EMA

- SUP 2: 112-30 Low Oct 13

- SUP 3: 112-22 50-day EMA

- SUP 4: 112-06 Low Sep 25 and a reversal trigger

Bullish conditions in Treasuries remain intact. The recent breach of key resistance at 113-29, the Sep 11 high, confirms a resumption of the medium-term uptrend. Moving average studies are in a bull-mode position and this set-up highlights a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance. Firm support lies at 11303+, the 20-day EMA.

PIPELINE: Corporate Bond Update: GM Financial, Dominican Republic on Tap

- Date $MM Issuer (Priced *, Launch #)

- 10/22 $1.5B #Alberta 10Y SOFR+81

- 10/22 $1B Rep of Korea WNG 5Y +19a

- 10/22 $Benchmark GM Financial 3Y +110a

- 10/22 $Benchmark Dominican Republic 10Y 6.25%a

- 10/22 $Benchmark Pershing Square 7Y investor calls