US DATA: Mortgage Spreads Continue To Narrow, But MBA Activity Stays Weak

Dec-17 19:20

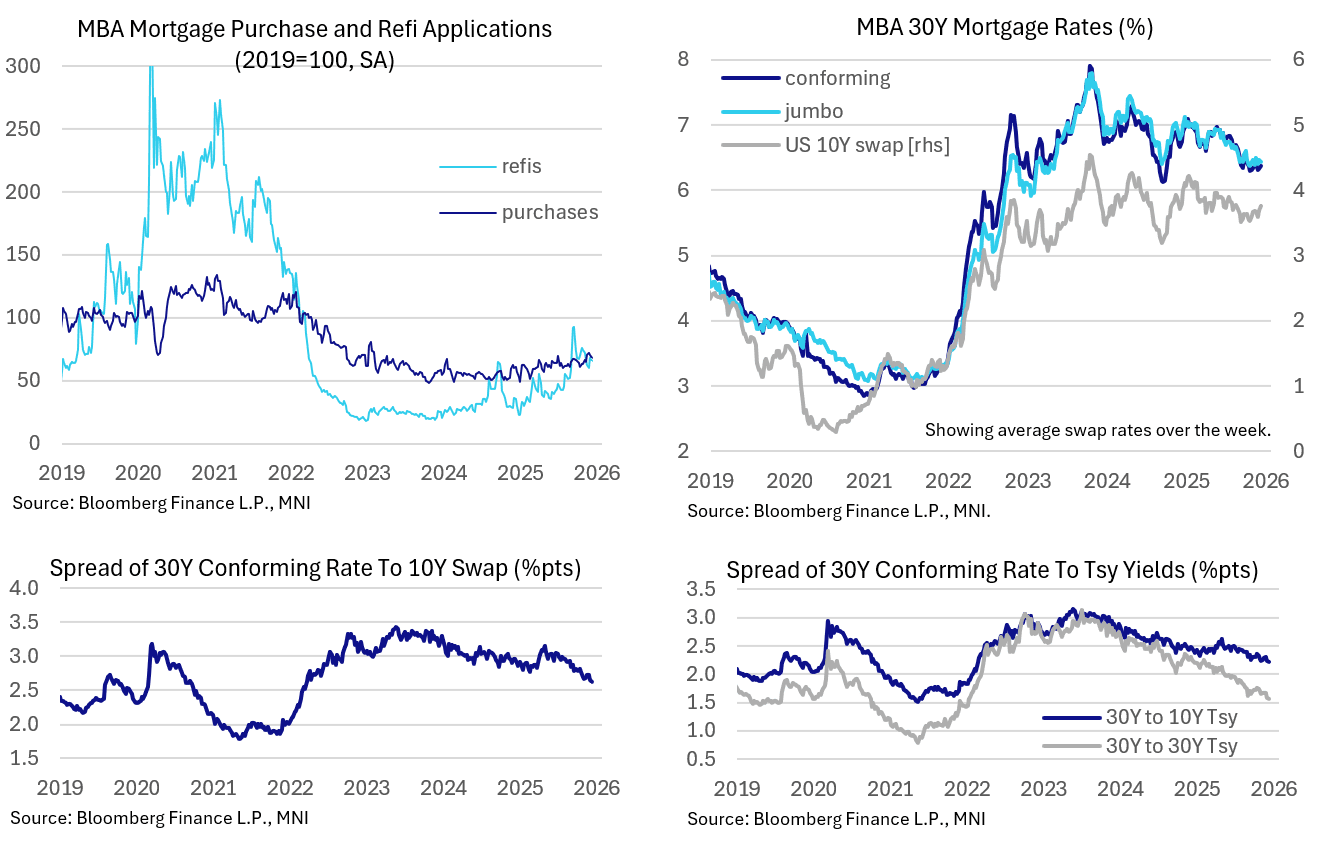

MBA mortgage application activity softened slightly in the latest week, but the more notable trend in recent weeks has been a continued narrowing of mortgage rate spreads.

- The MBA composite fell 3.8% W/W in the week of Dec 12, partially reversing the 4.8% rise the previous week but keeping activity at the overall subdued levels seen since late 2023 (at 1/3 below pre-pandemic levels). Purchase applications fell 2.8% for a 2nd consecutive fall, while refinancing apps pulled back 3.6% after soaring 14.3% the prior week.

- This pullback came as 30Y conforming mortgage rates ticked up, by 5bp to 6.38% for a 3-week high; Jumbo rates dipped 2bp after a 6bp rise the prior week.

- But this was due to a rise in underlying rates. 10Y Treasury yields averaged 7bp higher than the prior week (4.17% after 4.09%) with 30Y up 6bp (4.81% after 4.75%), with 10Y swaps up 8bp (3.76% after 3.68%).

- As such, mortgage spreads continued to fall. Conforming 30Y mortgage spreads to 10Y fell to 221bp and to 30Y to 157bp with spreads to 10Y swaps at 261bp, all the lowest since early 2022.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Former Senior Fed Board Economist On Monetary Policy

Nov-17 19:14

MNI interviews former senior Fed board economist on monetary policy -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

US STOCKS: Back to Extending Session Lows

Nov-17 19:13

- Couple of large program sales, one appr 1,470 names - largest since late October, sees the DJIA fall to 46,712.19 low.

- Chip makers continue to lead late session declines (Dell -8.79%, Hewlett PAckard Ent -8.59%, Super Micro -6.47%), followed by Energy and Financial names.

US LABOR MARKET: MNI US Payrolls Preview: Better Late Than Never

Nov-17 19:12

- We have published and e-mailed to subscribers the MNI US Payrolls Preview.

- Please find the full report including MNI analysis and analyst views here.

- The long-awaited nonfarm payrolls report for September will be released on Thursday at 0830ET.

- Having been collected prior to the government shutdown, this could be the last “conventional” payrolls release of the year with potential for a combined report covering October and November in December.

- Nearly all primary dealer analysts have stuck with their original estimates, for a median estimate of 60k nonfarm payrolls growth, consistent with the 58k in the broader Bloomberg survey.

- The unemployment rate should be watched particularly closely not least before there’s a good chance there won’t be an unemployment rate estimate for October. It’s seen holding at 4.3% with various trackers pointing to very marginal deterioration on the month.

- Patient Fedspeak has seen a large hawkish adjustment at the front-end in recent weeks, with only ~10bp of cuts priced for the Dec 9-10 FOMC meeting vs 22bp prior to Powell’s press conference late last month.

- There’s a chance we won’t have another payrolls report released prior to this December meeting.