GLOBAL POLITICAL RISK: More Headlines From Trump's Speech On Iran

*TRUMP: CORE STRATEGIC OBJECTIVES IN IRAN NEARING COMPLETION" "*TRUMP: MUST COMPLETE MISSION IN IRAN...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: Antipodean Update

The AUD and NZD are trading slightly higher in the Asian morning. The AUD in particular continues to outperform, though it will need to clear 0.7120-0.7130 area against the USD to reassert its upward momentum. The NZD continues to trade firmly within in its recent 0.5885-0.6015 range albeit with a heavy tone.

- {AUDUSD Curncy} - 0.7100, +0.10%

- {NZDUSD Curncy} - 0.5945, +0.07%

- {AUDNZD Curncy} - 1.1945, +0.05%

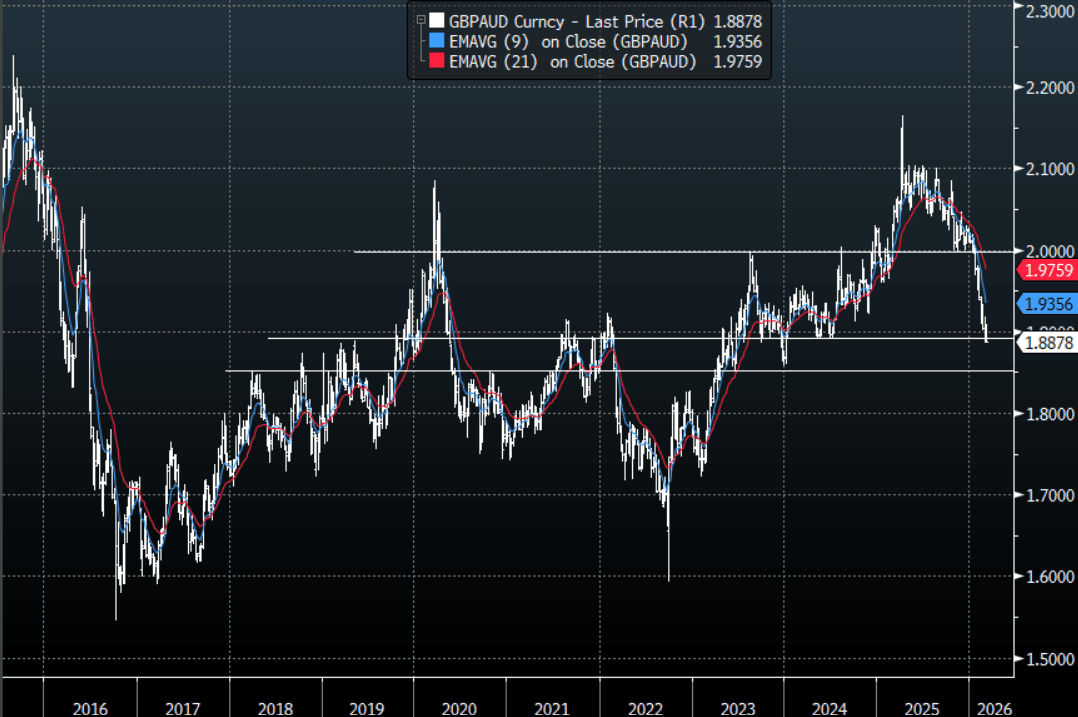

AUD: GBP/AUD - Still Trades Heavy After Reaching 1.8900 Target

The GBP/AUD range overnight was 1.8856-1.8986, Asia is trading around 1.8875. The pair quickly moved back to its lows as the AUD continues to outperform strongly in the crosses, the complete turnaround by US stocks certainly helped but for the moment the AUD is being very well supported. Having ultimately reached its initial target of 1.8900 my advice of some prudence down here has not proven to be warranted as of yet. The down trend remains technically strong and at the moment it feels it would take something significant to dent the conviction of the AUD bulls. On the day, the first resistance is back toward 1.9000-1.9050 and then the 1.9200-1.9250 area. A sustained break below 1.8850-1.8900 and the next target would be around 1.8500.

- The GBP/AUD Average True Range(ATR) for the last 10 Trading days: 133 Points

Fig 1: GBP/AUD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSTRALIA DATA: Net Export Drag To Q4 GDP Less Than Forecast, Govt Spend To Add

Australia's Q4 net exports contribution to GDP cut -0.1pps off growth, the same as the Q3 drag. The market expected a -0.3ppts drag, so a slightly better than expected outcome. The ABS also notes that total public demand will contribute 0.3ppt to Q4 growth. This comes ahead of tomorrow's Q4 GDP print. The market consensus is a 0.7%q/q rise (prior 0.4%) and y/y pace of 2.2% (prior 2.1%). The q/q forecast range is 0.5-1.0% at this stage. The focus will be on the domestic demand impulse, particularly as the economy bumps up against capacity constraints.

- RBA Governor Bullock noted earlier that every RBA meeting is live. If we see signs of stronger domestic growth in Q4 last year, it would likely add, at the margins, to rate hike expectations.

- Other data today showed a wider than expected current account deficit -$A21.1bn, versus -A$16.5bn forecast (Q3's outcome was

-A$18.3bn). The ABS noted: ‘The current account balance recorded its second consecutive fall, as the net primary income deficit widened by $2.5 billion.’ The wider primary income deficit was due to a $1.6 billion rise in primary income paid to overseas investors, driven by stronger dividends paid by Australian firms. Adding to this was a decrease of $0.9 billion in income received from Australian investment overseas. The $1.3 billion surplus on goods and services remained steady for the December quarter 2025, as export growth was fully offset by import growth." - Finally, Jan building approvals fell by 7.2%m/m, well below the +5.0% forecast rise (and after a -14.9% dip in Dec). The private sector houses component rose 1.1% after a 1.2% Dec gain. Weakness for the second straight month was in the apartment/townhouse segment.