AUSSIE BONDS: Modestly Stronger, Jobs Data Tomorrow

ACGBs (YM +1.0 & XM +2.0) are modestly stronger after US tsy futures closed firmer.

- Looking ahead, Wednesday’s US data is limited to MBA Mortgage Applications and $42bn 10Y Note. Focus on multiple Fed speakers through the session: Williams, Paulson, Waller, Bostic, Miran and Collins.

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at +25bps.

- The bills strip is little changed across contracts.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 9% probability, with a cumulative 16bps of easing priced by mid-2026.

- Interestingly, AU-NZ 1-year forward 3-month swap (1Y3M) spread at 103bps is now at its highest level since 2012.

- Today, the local calendar will see Home Loan data alongside RBA Jones' Fireside Chat.

- However, the highlight of this week's AUS calendar will be Thursday's October jobs data. The unemployment rate rose 0.2pp to 4.5% in September.

- Last month's weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035bond today and A$800mn of the 1.75% 21 November 2032 bond on Friday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (Z5) Reversal Lower Extends

- RES 3: 95.960 - High Apr 7 (cont.)

- RES 2: 95.875 - High Jul 2 (cont.)

- RES 1: 95.780 - High Sep 12, 18 and 19

- PRICE: 95.635 @ 15:42 BST Oct 10

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

Aussie 10-yr futures are trading closer to their recent lows. It is still possible that the recent move down is a correction. Near-term resistance to watch is 95.780, the Sep 12 high. A clear break of this level would signal scope for a continuation higher and open 95.875, the Jul 2 high on the continuation chart. On the downside, key short-term support to watch has been defined at 95.510, the Sep 3 low. Clearance of this level would instead be bearish.

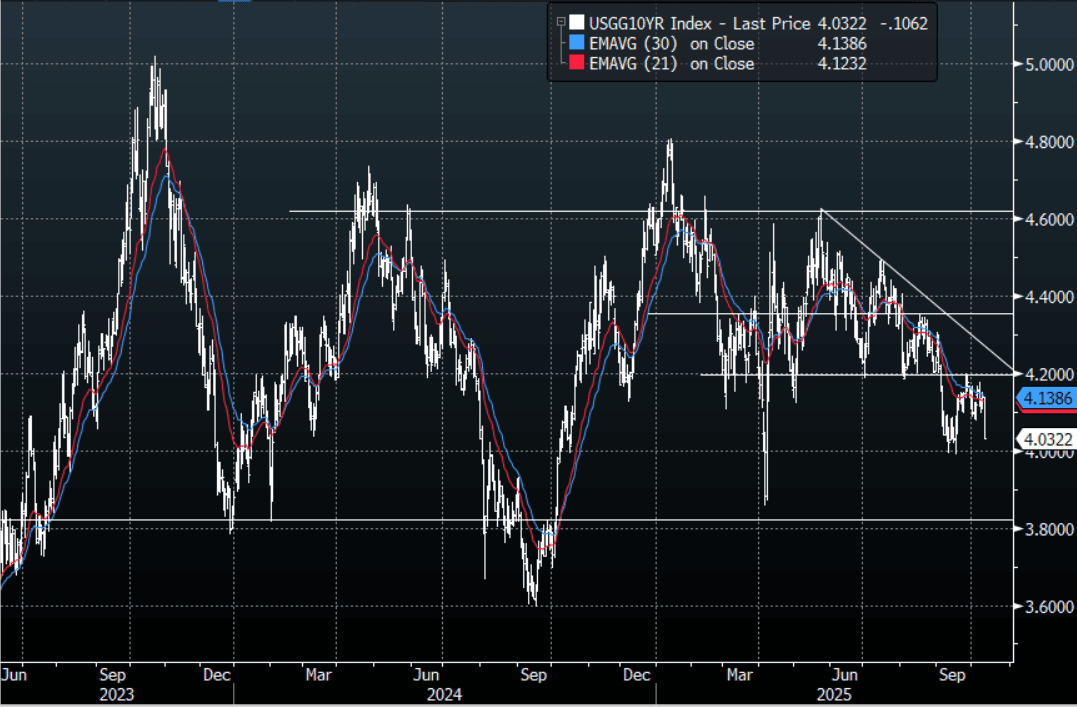

US TSYS: Yields Collapse On Friday, How Far Can They Bounce As Tone Changes

10-Year yields accelerated lower on Friday on the back of China/US Escalation. Some clarification from China over the weekend on their new rare earth export controls has seen the US walk back its aggressive stance and a more conciliatory tone is being set. I suspect a lot of Friday's moves will see some decent pullbacks on this, but how long it lasts is anybody's guess. A break of 4.00% could potentially see the start of another leg lower.

- TYZ5 reopens at 112-31, down 0-05+ from closing levels in today’s Asia-Pac session

- Friday night the US 10-year yield had a range of 4.0322% - 4.1286%, closing around 4.032%.

- Treasury yields all had some significant moves lower on Friday night;(2s10s -1.51 at 52.857, 5s30s +0.70 at 99.046.

- Robin Brooks wrote a substack expanding on how he thought markets might play out if the situation escalates again: “If the China-US trade war escalates and China devalues, there'll be lots of collateral damage: (i) US Treasury market will go "yippy" like in April; (ii) high-debt countries like Japan and France will suffer; (iii) $-pegs in Argentina and Turkey will blow.” https://t.co/Sh4nlrKDWC

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS 5-7bps Lower Following Fri US Moves, 2yr Eyeing 2.50% Downside Test

NZGB yields sit around 5-7bps lower across the benchmarks in the first part of Monday trade, with the back end leading slightly. This follows a sharp risk off move late on Friday, where equities falter and US Tsys saw a flight to safety post Trump's 100% tariff threat against China. Comments from the weekend and today from US officials suggest issues can be resolved though. We won't have cash US Tsy trading in Asia Pac today with Japan markets out, but if broader risk sentiment stabilizes NZGB yield losses may stabilize reverse somewhat.

- The 2yr was last near 2.57%, down 5bps, the 10yr around 4.05%, off 7bps. The short end of the NZGB curve remains oversold in terms of yield losses, while the 10yr yield is also close to this point (based off RSI (14)).

- For the 2yr NZGB yield we are at fresh lows back to 2022, for the 10yr we near 2024 lows. Downside risks prevail at the short end of the curve, even with oversold conditions, as markets await a catalyst to break us out of the steep trend decline. The 2.50% level beckons for the 2yr NZGB yield.

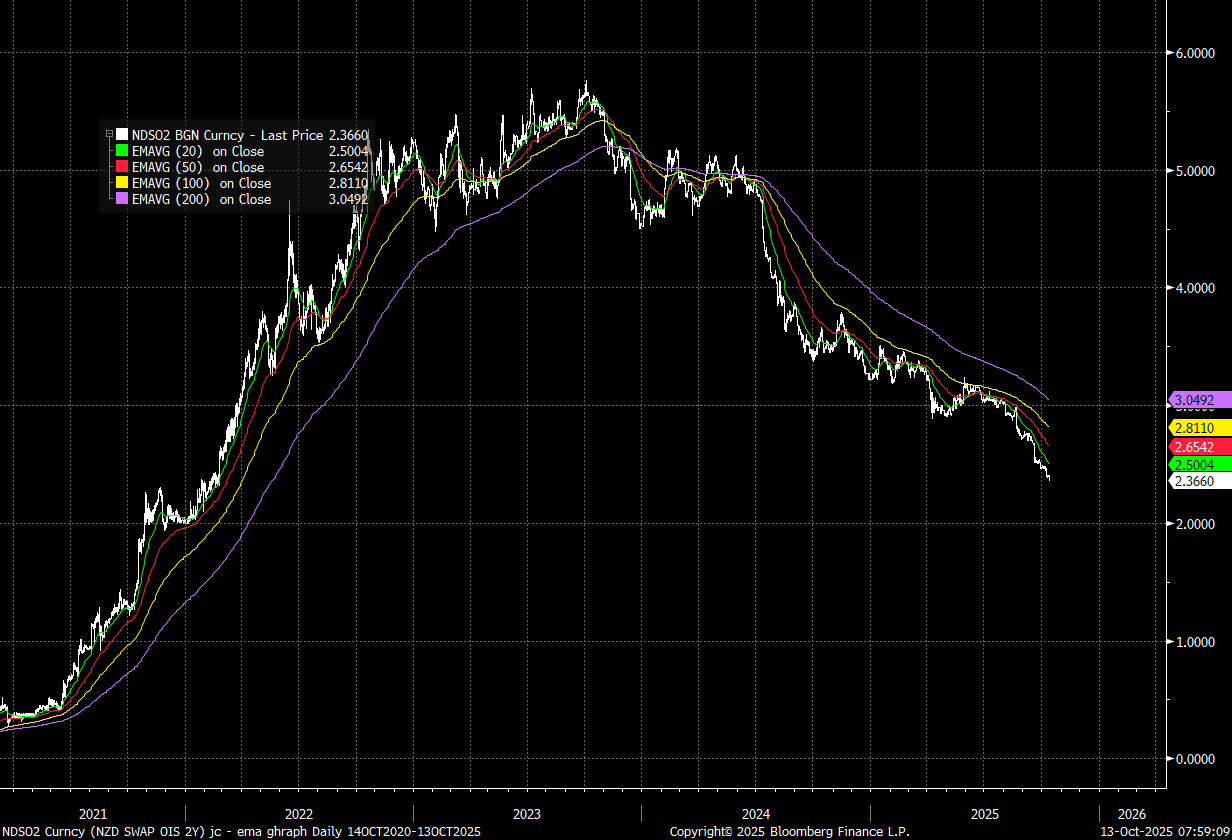

- The 2yr swap rate is already comfortably under this point, last 2.37%, off a further 3bps today. Longer term trends look set for a move into the 2.00-2.25% region, see the chart below (notwithstanding oversold conditions).

- NZ-US10yr spread was last +4bps, up from recent lows sub flat. We are still in the bottom half of recent ranges. The US 10yr yield lost close to 11bps on Friday as risk off gripped markets.

- On the data front, the PSI rose in Sep to 48.3 from 47.6, so an improvement but still in contraction territory. Net migration eased for Aug, while annual migration slowed to just under 10.7k.

Fig 1: NZ Swap 2yr Versus Key EMAs - Steep Downtrend Persists

Source: Bloomberg Finance L.P./MNI