MNI US OPEN - Yields March Higher, Triggering USD Buys

EXECUTIVE SUMMARY

- SENIOR LDP FIGURES RESIGN, UNCLEAR IF ENOUGH TO SAVE ISHIBA’S POSITION

- BOJ'S HIMINO SEES GRADUAL HIKES; UPSIDE, DOWNSIDE RISKS

- EUROZONE AUGUST HICP MARGINAL DOWNSIDE VS CONSENSUS FROM ENERGY

- EARLY DOSE OF RISK-OFF TRIGGERS LOSSES FOR GBP, JPY

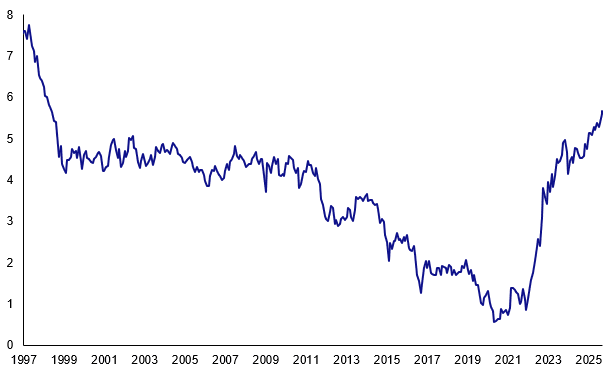

Figure 1: Yield on 30-year gilt rises to highest since 1998

Source: MNI/Bloomberg Finance L.P.

NEWS

JAPAN (MNI): Senior LDP Figures Resign, Unclear if Enough to Save Ishiba’s Position

A flurry of resignsations from senior leadership positions within the governing Liberal Democratic Party (LDP) have followed what is reported to have been a raucous internal party meeting this afternoon. Secretary-General of the governing Liberal Democratic Party (LDP), Hiroshi Moriyama, has said that he will stand down from his position in the wake of the party's poor performance in July elections to the upper house of the National Diet. Mainichi reports: "There is a strong view within the party that if Moriyama resigns, the administration's operations will come to a standstill", given that the gov't does not hold a majority in either chamber of parliament and the Sec-Gen was seen as a key interlocutor with the opposition.

US/INDIA (BBG): US, India Keep Door Open to Trade Talks Despite Tariff Tensions

President Donald Trump said India offered to cut tariffs, while New Delhi signaled it’s continuing to negotiate a trade agreement with the US, indicating both sides are keeping the door open to resolving tensions. Trump said in a social media post on Monday that India offered to reduce its tariffs on US goods to zero, without saying when the concession was made. He added that “it’s getting late” and India should have made the offer “years ago.” India’s government hasn’t officially responded to Trump’s remarks, but Commerce Minister Piyush Goyal said at an event on Tuesday that both sides continue to engage to reach a trade agreement. “We are in dialog with the US for a bilateral trade agreement,” Goyal said in New Delhi.

ECB (MNI): Schnabel Interview Contains Unsurprising Hawkish Themes

ECB Executive Board member Schnabel's extensive interview with Reuters this morning doesn't contain many surprising themes. It leans hawkish (that is, in favour of steady rates going forward). The key excerpt is: "At the current juncture, I see no reason to adjust the policy stance in either direction. Interest rates are in a good place. Medium-term inflation is projected to be around 2% and inflation expectations are anchored. We are at full employment and the economy is growing around trend."

ECB (BBG): ECB’s Simkus Hints at December Rate Cut

Governing Council member Gediminas Simkus suggested the European Central Bank may need to cut interest rates in December, according to Econostream Media. The Lithuanian governor said that he “would not be surprised if Santa Claus comes with scissors,” the news service said in an X posting, citing an interview. He added that it’s “more true than not” that another reduction is coming and that officials could conceivably discuss a move in October if presented with evidence of a worsening economy.

UK (BBG): UK Markets Slide as Debt Angst Drives 30-Year Yield to 1998 High

The yield on long-dated UK bonds rose to the highest since 1998 and the pound fell, pressuring Prime Minister Keir Starmer’s government to regain the confidence of investors who remain concerned over the fiscal outlook. The rate on 30-year gilts rose five basis points to 5.69% on Tuesday amid a global decline in government bonds. Sterling tumbled, falling as much as 1.3% to $1.3376 and lagging all other major currencies. The FTSE 100 Index retreated 0.5%.

BOJ (MNI): BOJ's Himino Sees Gradual Hikes; Upside, Downside Risks

Bank of Japan Deputy Governor Ryozo Himino said Tuesday the Bank would raise its policy rate to adjust the degree of monetary accommodation if its baseline scenario for economic activity and prices materialises, though he gave no guidance on timing or pace. “There are risks to economic activity and prices in both directions. Without any preconceptions, we will continue to monitor the economy closely to see if the baseline scenario unfolds as expected,” Himino told business leaders in Kushiro City.

CHINA/RUSSIA (BBG): Xi, Putin Meet in Beijing, Highlighting Their Close Ties

Chinese leader Xi Jinping and Russian President Vladimir Putin met briefly in Beijing — a reminder of the tight relationship the two have developed since Moscow’s attack on Ukraine. Xi welcomed Putin to the sitdown on Tuesday by calling him an “old friend.” He added that “China-Russia relations have withstood the test of changing international circumstances” and said they were a good example of “amicableness among neighbors, comprehensive strategic coordination and mutually beneficial cooperation.”

CHINA/RUSSIA (BBG): Russia, China Agree on Long-Awaited Gas Pipeline, Gazprom Says

Russia’s Gazprom PJSC said it signed a legally binding agreement to build the long-anticipated Power of Siberia 2 gas pipeline to China via Mongolia and would expand deliveries through other routes, in what will be seen by the Kremlin as a major political win. In comments made to Russian wires from Beijing, Chief Executive Officer Alexey Miller said the gas producer could ship as much as 50 billion cubic meters a year via the Power of Siberia 2 for 30 years. Miller said the price for the fuel will be lower than what Gazprom currently charges customers in Europe, according to the reports.

CHINA (MNI EXCLUSIVE): China's Fiscal Expansion Needs Decrease as 5% GDP Eyed

Chinese advisors share their fiscal policy outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

INDIA (BBG): Indian Banks Tell RBI They’ve Limited Room to Buy State Bonds

Some of India’s biggest banks have told the central bank that they are running out of room to buy bonds issued by states, people familiar with the matter said. The lenders recently approached the Reserve Bank of India, warning that the share of state bonds in their investment portfolios has risen sharply and is nearing internal limits, according to people familiar with the matter, who declined to be identified as the discussions are private.

DATA

EUROZONE DATA (MNI): EZ August HICP Marginal Downside vs Consensus From Energy

- EUROZONE AUG FLASH HICP +2.1% Y/Y, +0.2% M/M

- EUROZONE AUG FLASH CORE HICP +2.3% Y/Y, +0.3% M/M

- EUROZONE AUG FLASH SERVICES HICP +3.1% Y/Y, +0.3% M/M

Eurozone August HICP came in at 2.05% Y/Y, 5 hundredths below rounded initial consensus of 2.1% Y/Y and marginally higher than we would have expected the print following national-level data released over the last couple of days (vs 2.04% prior). The marginal downside surprise vs consensus on headline was energy-driven: the category printed -1.89% Y/Y (-1.6% MNI median, -2.39% prior) while core inflation was slightly higher than expected at 2.27% (2.2% consensus, 2.31% prior) driven by NEIG.

JAPAN DATA (MNI): Japan Q2 GDP Seen Higher on Public Investment

Japan’s economy in the April–June quarter is likely to have grown slightly faster than the initial estimate as public investment improved, though capital spending and private consumption were little changed, according to economists surveyed after a key government release. The median forecast of seven economists puts revised Q2 GDP at +0.3% q/q, or an annualised +1.2%, compared with the preliminary +0.3% q/q, or +1.0% annualised.

AUSTRALIA DATA (MNI): Current Account Deficits Continue, Net Exports Added 0.1ppt

- AUSTRALIA Q2 CURR ACCT BALANCE -13654M

While Q2 recorded its ninth consecutive quarterly current account deficit, it narrowed from Q1 driven by the primary income deficit. Q2 printed at -$13.7bn after $14.1bn with primary income at -$16.8bn down from Q1's -$18bn but the goods and services surplus was down $1.2bn at $3.1bn, the lowest in 7 years. Net exports contributed 0.1pp to Q2 growth, as expected.

FOREX: Early Dose of Risk-Off Triggers Losses for GBP, JPY

- Following generally steady Asia-Pac trade, markets underwent a sharp dose of risk-off alongside the European open as a sustained shoot higher in longer-end yields unsettled sentiment across equities, currencies and bond markets. The mix this morning of: political uncertainty in Japan (various resignations across the LDP), a window-dressing UK reshuffle (not expected to resolve Starmer's popularity crisis in the near-term) and acute pressure on the longer-end of the UK, US and European yield curves - has reignited fiscal, financing and politic risk concerns around higher borrowing costs - driving sentiment through the European open.

- Sizeable down-move in GBP/USD comes despite the bullish technical backdrop that stemmed from the bullish engulfing candle posted on August 22nd. With spot showing through the lows already today, this somewhat undermines the recovery off 1.3391 and instead retracement support expected into 1.3315 and 1.3369 is of more importance.

- Gains for the USD Index put the currency on for a strong start to September. The daily candle chart has the USD Index on course to form downtrendline resistance drawn off the early August high at today's 98.389 print.

- Today's price action serves as a further reminder of the pressure on governments from bond markets, particularly as Summer concludes. Today's Gilt price action shows markets are not satisfied with floated proposals so far for the UK Treasury to raise indirect taxes through property, capital gains, landlords, or otherwise. Given the internal party opposition to spending cuts, this places additional pressure on the Chancellor's pledge not to raise VAT, income tax or national insurance this parliament - a topic that will likely be a market focus into the Autumn Budget - and may have to become a more palatable option the longer yields stay higher.

- Focus for the duration of Tuesday trade remains on the volatility in the longer-end of the curve, as well as the ISM manufacturing print for August. The release will be watched carefully for clues or signals headed into this Friday's highly consequential NFP print.

BONDS: Curves Under Renewed Steepening Pressure Amid Political/Issuance News

Global core FI curves are facing renewed steepening pressure this morning, with political/fiscal concerns in the likes of Japan and the UK helping push long-end yields higher. The UK is also launching its new 10-year Gilt via syndication.

- In Japan, there have been various resignations across the LDP. 30-year yields closed at 3.23%, just shy of the 3.24% all-time-high seen last week.

- In the UK, PM Starmer’s window-dressing reshuffle is not expected to resolve him and his party’s popularity crisis in the near-term. Although today’s 10-year syndication has attracted a healthy book size of GBP140bln, that has culminated in a record GBP14bln size (above MNI’s original expectations). These drivers see 10-year Gilt yields up 4bps to 4.79%, having met resistance around the 4.80% level earlier.

- Meanwhile, Bund yields are up 3.3bps at 2.78%, with the 2.80% level capping upside there.

- That leaves the 10-year Gilt/Bund spread 0.7bps wider at 201bps, shy of last week’s 203bps closing multi-week high.

- Today’s E4.5bln Schatz auction saw somewhat weaker demand metrics than last months outing, but was on balance digested smoothly.

- Eurozone flash August core HICP inflation was a little higher than expected at 2.27% Y/Y (vs 2.2% MNI median, 2,31% prior). It wasn’t a major market mover.

- ECB Executive Board member Schnabel gave a characteristically hawkish interview with Reuters this morning, but Euribor futures have pared associated early weakness (aided by a somewhat more dovish interview from ECB’s Simkus).

- The 10-year OAT/Bund spread is 1bp wider today at ~80bps, with intraday price action seemingly a function of broader core FI moves rather than any domestic developments. While the spread is off last week's closing extremes of 81.5bps, political/fiscal-related widening pressures remain in focus. A reminder that the spread was hovering around ~70bps prior to Bayrou's no-confidence vote announcement.

EQUITIES: E-Mini S&P Remains in Bullish Cycle of Higher Highs and Higher Lows

The trend set-up in Eurostoxx 50 futures is bullish and the pullback from the Aug 22 high appears corrective - for now. Note that support at 5375.94, the 50-day EMA, has been pierced. A clear break of this average would strengthen a S/T bearish threat and signal scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, resistance to watch is 5522.00, the Aug 22 high. A break of it would resume the uptrend. A bull cycle in S&P E-Minis remains intact and the contract traded to a fresh cycle high last week. This maintains the bullish price sequence of higher highs and higher lows. Moving average studies are in a bull-mode position too, highlighting a clear uptrend and positive market sentiment. Attention is on 6543.75, a Fibonacci projection. Support to watch lies at 6332.30, the 50-day EMA. The latest pullback appears corrective.

- Japan's NIKKEI closed higher by 121.7 pts or +0.29% at 42310.49 and the TOPIX ended 18.69 pts higher or +0.61% at 3081.88.

- Elsewhere, in China the SHANGHAI closed lower by 17.398 pts or -0.45% at 3858.133 and the HANG SENG ended 120.87 pts lower or -0.47% at 25496.55.

- Across Europe, Germany's DAX trades lower by 235.44 pts or -0.98% at 23802.08, FTSE 100 lower by 37.18 pts or -0.4% at 9159.32, CAC 40 up 7.7 pts or +0.1% at 7715.6 and Euro Stoxx 50 down 22.27 pts or -0.41% at 5344.81.

- Dow Jones mini down 169 pts or -0.37% at 45432, S&P 500 mini down 29 pts or -0.45% at 6443.75, NASDAQ mini down 138.75 pts or -0.59% at 23323.75.

Time: 10:00 BST

COMMODITIES: Gold Extends Current Bull Cycle, Breaches Key Resistance at $3500

A bear cycle in WTI futures remains intact and recent gains are considered corrective. A key support at $61.99, the Jun 30 low, has recently been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $66.56, the Aug 4 high. Gold is trading sharply higher this week as the metal extends its bull cycle. Today’s gains have resulted in breach of key resistance at $3500.1, the Apr 22 high, and delivered a fresh all-time high. This confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3547.9, a Fibonacci projection. Initial firm support to watch lies at $3381.8, the 20-day EMA.

- WTI Crude up $1.67 or +2.61% at $65.68

- Natural Gas down $0.02 or -0.6% at $2.979

- Gold spot up $1.43 or +0.04% at $3477.25

- Copper down $3.1 or -0.68% at $456.05

- Silver down $0.45 or -1.11% at $40.2417

- Platinum down $22.35 or -1.59% at $1385.23

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 02/09/2025 | 1130/1330 | ECB Elderson and Machado Panel at ECB Legal Conference | ||

| 02/09/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/09/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 02/09/2025 | 1400/1000 | * | Construction Spending | |

| 02/09/2025 | 1400/1000 | * | Construction Spending | |

| 02/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 52 Week Bill | |

| 03/09/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/09/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/09/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/09/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/09/2025 | 0130/1130 | *** | Quarterly GDP | |

| 03/09/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 03/09/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 03/09/2025 | 0700/0300 | * | Turkey CPI | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0730/0930 | ECB Lagarde Speaks at ESRB Conference | ||

| 03/09/2025 | 0730/0830 | BOE Mann at Signum's London Westminster Day roundtable | ||

| 03/09/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/09/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/09/2025 | 0815/0915 | BOE Breeden at Innovation in Money and Payments Conference | ||

| 03/09/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/09/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/09/2025 | 0900/1100 | ** | EZ PPI | |

| 03/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 03/09/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/09/2025 | 1300/0900 | St. Louis Fed's Alberto Musalem | ||

| 03/09/2025 | 1315/1415 | BOE testify at TSC: Bailey, Greene, Lombardelli, Taylor | ||

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/09/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/09/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/09/2025 | 1730/1330 | Minneapolis Fed's Neel Kashkari | ||

| 03/09/2025 | 1800/1400 | Fed Beige Book |