MNI US OPEN - Ueda Does Little to Dispel BOJ Hike Expectations

EXECUTIVE SUMMARY

- RBA BOARD SEES 2026 HIKE RISKS, CUTS RULED OUT

- UEDA INTERVIEW WITH FT DOES LITTLE TO DISPEL BOJ HIKE EXPECTATIONS

- TRUMP EYES TARIFFS OVER CANADIAN FERTILIZER, INDIAN RICE

- UK BRC RETAIL SALES CONTINUE SLOWING, PROPPED UP BY FOOD INFLATION AGAIN

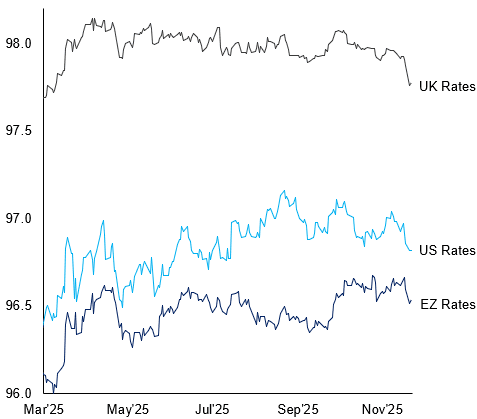

Figure 1: H7 rates markets show little sign of a bounce

NEWS

RBA (MNI): Board Sees 2026 Hike Risks, Cuts Ruled Out

The Reserve Bank of Australia Board sees the balance of risks tilted toward a potential rate hike in 2026 to contain inflation, with cuts firmly off the table, Governor Michele Bullock said, adding that policymakers will reassess the restrictiveness of the 3.6% cash rate in the new year. Bullock’s comments at a press conference followed the Board’s unanimous and widely expected decision to hold the cash rate at 3.6% on Tuesday, marking a third consecutive pause. The Board’s discussion centred on the likelihood of a prolonged hold and the potential need for a hike sometime in 2026, she added. RBA overnight index swaps rose sharply after her remarks, with markets fully pricing in a 25 basis point increase by June and a 4.32% cash rate by September.

BOJ (MNI): Ueda Interview With FT Does Little to Dispel BOJ Hike Expectations

BOJ Governor Ueda's has spoken in an interview with the FT. A reminder that Ueda's comments last week increased expectations for a December BOJ hike significantly. Markets now almost fully priced a 25bp move next Friday. This interview does little to push back on prior comments. Some highlights from the FT piece as follows: The governor has previously said that the BoJ would consider the "pros and cons" of a rate rise at its December meeting - which market participants have interpreted as signalling a likely move. The central bank governor's comments did nothing to dispel those expectations, though Ueda did not repeat the "pros and cons" language, he said that "the real side of the economy is doing OK" and underlying inflation is "continuing to rise towards our 2 per cent target".

JAPAN (BBG): Japan’s Katayama Says Watching Market Trends as Yields Near 2%

Japanese Finance Minister Satsuki Katayama said she is closely watching market trends, as the yield on 10-year government debt hovers near 2%, a level not seen since 2006. “We are monitoring market trends very closely,” Katayama told reporters on Tuesday when asked about the recent rise in yields. “We will manage government bonds appropriately through close communication with the market” she said, while refraining from commenting on any specific level.

US (BBG): Trump Eyes Tariffs Over Canadian Fertilizer, Indian Rice

President Donald Trump signaled he could impose fresh tariffs on agricultural products, including Canadian fertilizer and Indian rice, the latest sign that protracted negotiations with two US trading partners could drag on. Trump spoke Monday at a White House event to announce billions in new aid for US farmers, some of whom said cheaper imports were making it difficult for their products to compete in the marketplace. The president said he would “take care” of alleged dumping of Indian rice into the US. Some farmers have blamed imports for falling rice prices, saying countries such as India, Vietnam and Thailand are undercutting their crops.

US/CHINA (BBG): Nvidia Wins Trump’s Approval to Sell H200 AI Chips in China

President Donald Trump granted Nvidia Corp. permission to ship its H200 artificial intelligence chip to China in exchange for a 25% surcharge, a move that lets the world’s most valuable company potentially regain billions of dollars in lost business from a key global market. The decision was announced by Trump in a post on his Truth Social network, capping weeks of deliberations with advisers about whether to allow H200 exports to China. Trump said he informed Chinese President Xi Jinping about the move and that Xi had responded favorably.

US (WSJ): Jamie Dimon Forms Adviser Supergroup for $1.5 Trillion American Resiliency Pledge

He is assembling a group of national titans and close friends, from Jeff Bezos to Condoleezza Rice, to help him get it ready. The head of JPMorgan Chase, the biggest U.S. bank, announced a $1.5 trillion initiative focused on national security in October, meant to bolster American self-sufficiency for critical technologies including rare earths and artificial intelligence.

EUROPE/UKRAINE (The Times): Deal to Release £100bn for Ukraine Close, Keir Starmer Says

A deal to release up to £100 billion of frozen Russian assets in Europe to aid Ukraine is just days away, Sir Keir Starmer believes, as he said negotiations to end the war had reached a “critical stage”. The prime minister held talks with President Zelensky on Monday, along with his French and German counterparts, to discuss the latest US peace proposals.

FRANCE (BBG): France’s Budget Process Teeters on Social Security Bill Vote

French Prime Minister Sebastien Lecornu faces a key vote on the social security budget on Tuesday that risks fueling political turbulence and uncertainty over how the country will plug holes in its public finances. The National Assembly will vote on the bill, which covers spending on welfare, health and pensions for 2026 and contains key concessions Lecornu’s minority government made to opposition groups to allow it to stay in power.

S.KOREA (BBG): Korea’s Pension Fund Sells Dollars to Support Won

South Korea’s National Pension Service has recently started selling US dollars to bolster the won, according to a person familiar with the matter, reviving earlier efforts to support the currency. The NPS, which held about $542 billion of foreign assets as of the end-September, started its sales as part of a tactical hedging strategy, the person said, asking not to be identified because the information is private. The move comes as the won has slid nearly 8% in the second half of the year, making it Asia’s worst-performing currency amid concerns about capital outflows and trade uncertainty. NPS had conducted such strategic hedges between January and May this year.

DATA

GERMANY OCT TRADE BALANCE EUR +16.9 BLN (MNI)

GERMANY OCT EXPORTS +0.1% M/M; IMPORTS -1.2% M/M (MNI)

GERMANY DATA (MNI): Truck Toll Index Points Towards Soft November IP

Destatis has released its monthly data for November for its truck toll index, which printed -0.8% on a sequential comparison. The data comes after yesterday's October IP release (1.8% M/M) was on the stronger side, following a positive September (1.3%) but a very weak August (-3.7%). There is a "clear correlation between the truck toll mileage index and indices of economic activity, particularly industrial production. As the truck toll mileage index is available around a month earlier than the production index, it is suitable as an early indicator of economic development", Destatis comments on the publication.

UK DATA (MNI): BRC Retail Sales Continue Slowing, Propped Up By Food Inflation Again

- UK NOV BRC TOTAL RETAIL SALES 1.4% Y/Y

BRC Retail Sales saw a third consecutive slowdown in November, posting a 1.4% Y/Y increase in value terms (vs 1.6% October). This was the weakest reading since May and, once again, the positive growth rate was driven almost entirely by food inflation (with non-food close to flat in volume terms). Note that this reporting period included Black Friday and the following Saturday (but not the Sunday of that weekend or Cyber Monday). Last year the survey period ended the week prior to Black Friday so didn't include any of this major weekend. Given that this data is not adjusted, sales would expect to be boosted this year by including this busy period.

AUSTRALIA DATA (MNI): Q4 Conditions Up On Q3, Q4 Business Inflation Series Moderate

November NAB business conditions moderated to 7 from an upwardly-revised 10, while the more volatile confidence fell to 1 from 6, the lowest since April. Conditions remained in line with Q3 outcomes and at this stage looks like normalisation rather than slowing as the sharp rise in WA in October unwound. In line with Governor Bullocks assessment that the output gap had likely closed, the NAB capacity utilisation measure rose to 83.6%, the highest in a year and a half. Capacity constraints could put upward pressure on already elevated inflation.

FOREX: USDJPY Recovery Extends, AUD Outperforming Post-RBA

- USDJPY extended overnight gains through the European open, briefly printing 156.43, but stalling ahead of 156.58 resistance, the November 28 high. While interest rate correlations have been weaker in recent months, this week's corrective strength has been underpinned by hawkish repricing across core FI markets. A subsequent 30 pip fade off highs coincided with a downtick in the US 10y yield, followed by a Ueda interview which does little to dispel BOJ hiking expectations for December.

- AUD outperforms in the aftermath of the RBA, with the latest downtick for the DXY propelling AUDUSD back towards session highs. 0.6650 has continued to hold across the last three sessions, and a break above would likely prompt some momentum demand. Alongside the RBA’s expected hold at 3.6%, the board sees the balance of risks tilted toward a potential rate hike in 2026 to contain inflation, with cuts firmly off the table, according to Governor Bullock. 0.6707 remains the key AUDUSD resistance, the Sep 17 high.

- It is worth highlighting that NZDUSD has traded all the way back to its medium-term pivot at 0.5800, potentially providing an opportunity to re-establish longs in AUDNZD, which has been in a very strong uptrend across the second half of 2025. The cross has remained well supported by the 50-day EMA, intersecting around the 1.14 mark.

- Ahead of the AUD, the Swedish Krona tops the G10 leaderboard amid the stable risk backdrop Tuesday. Recent domestic data has suggested an economic recovery is taking hold in Sweden, helping EURSEK narrow the gap to support at 10.8815.

- BOE Deputy Governors Lombardelli and Ramsden, and external rate-setters Mann and Dhingra speak at Parliament's Treasury Committee later today. The data calendar sees the US weekly ADP release, NFIB small business index, weekly redbook retail sales, and JOLTS job openings ahead of tomorrow's FOMC.

EGBS: Recoveries in Bund Futures Considered Corrective for Now

Bund futures have moved away from multi-week lows this morning, currently +37 ticks at 127.66. Recoveries are still considered corrective for now, with initial resistance not seen till 128.08 (Dec 8 high). Volumes have been very healthy, seemingly reflecting a mix of views around whether the recent selloff can extend, or if a relief rally is more likely.

- 10-year Bund yields are down 2bps to 2.84%, after briefly reaching 2.88% this morning. The 2.90% figure presents the initial topside target, shielding the March 12 high of 2.94%.

- The German 10s30s curve is ~0.5bps steeper at ~60bps, after flattening around 5bps yesterday. The EUR 10s30s swaps curve is little changed at ~29bps. Given recent hawkish repricing in EUR rates has been primarily driven by the front-end, flattening further out the curve may represent unwinds of popular steepener positions related to the Dutch pension fund transition.

- 10-year EGB spreads to Bunds are up to 1bp wider on the session, with BTP/Bund spread back above 70bps. However, widening in the BTP/Bund spread has still been fairly contained considering the sharp uptick in EUR rates vol.

- In France, focus remains on this afternoon's National Assembly vote on the 2026 Social Security budget. The outcome remains very close to call.

- Ireland plans to issue E10-14bln of bonds with one syndication in 2026. This is a bit higher than expected, but there has so far been limited reaction in Irish bond markets.

- Today’s regional data calendar has been light, with some focus on US job openings data this afternoon ahead of tomorrow’s Fed decision.

GILTS: Off Lows as Equities Falter & Wider Sell Off in Bonds Stalls

Gilts have rallied from early session lows as European equities pullback from highs and the recent sell off in wider core global FI markets stalls.

- Futures tested yesterday’s low at the open before recovering to trade +40 at 91.10 last.

- On the technical front, support is clustered at 90.62/53, while resistance comes in at 91.16.

- While the rally has removed some of the acute bearish pressure, our technical analyst has noted that a break of the support cluster would deepen the recent bearish move and negate a bullish technical theme.

- Yields are 2-4bp lower, curve is flatter.

- 2s10s 3bp above post-Budget closing lows, while 5s30s is last trading 121.5bp, narrowing in on the June closing low at 118.15bp.

- The GBP750mln tender of the 4.25% Jun-32 gilt passed smoothly, generating strong demand.

- SONIA futures flat to 4bp firmer, terminal rate pricing 3.42% vs. a recent range of 3.285-3.465%. SFIZ6 recovers after registering the lowest level seen since mid-October.

- BoE-dated OIS shows ~22bp of easing for December vs. 21bp early today. We still expect a cut at that meeting.

- BoE’s Ramsden, Lombardelli, Dhingra & Maan are due to appear in front of a TSC (14:15 London). We do not expect any meaningful changes in tone at the event.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Dec-25 | 3.754 | -22.0 |

Feb-26 | 3.686 | -28.8 |

Mar-26 | 3.623 | -35.1 |

Apr-26 | 3.532 | -44.2 |

Jun-26 | 3.491 | -48.3 |

Jul-26 | 3.435 | -53.9 |

Sep-26 | 3.424 | -55.0 |

EQUITIES: Eurostoxx Futures Holding Onto Gains, Targets Key Resistance at 5825

A bull cycle in Eurostoxx 50 futures remains intact and the contract is holding on to its recent gains. Price has recently cleared the 20- and 50-day EMAs, signalling scope for a stronger recovery. Sights are on 5742.40 next (pierced), 76.4% of the Nov 13 - 21 bear leg. Clearance of this price point would pave the way for an extension towards 5825.00, the Nov 13 high and a key resistance. First key support lies at 5626.00, the 50-day EMA. A bull cycle in S&P E-Minis remains intact and price is trading above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support is at 6802.68, the 20-day EMA.

- Japan's NIKKEI closed higher by 73.16 pts or +0.14% at 50655.1 and the TOPIX ended 0.61 pts higher or +0.02% at 3384.92.

- Elsewhere, in China the SHANGHAI closed lower by 14.557 pts or -0.37% at 3909.521 and the HANG SENG ended 331.13 pts lower or -1.29% at 25434.23.

- Across Europe, Germany's DAX trades higher by 83.21 pts or +0.35% at 24127.81, FTSE 100 lower by 2.36 pts or -0.02% at 9642.53, CAC 40 down 31 pts or -0.38% at 8077.55 and Euro Stoxx 50 down 4.34 pts or -0.08% at 5721.39.

- Dow Jones mini up 27 pts or +0.06% at 47820, S&P 500 mini up 3.5 pts or +0.05% at 6859, NASDAQ mini up 0.5 pts or +0% at 25664.25.

Time: 10:00 GMT

COMMODITIES: Trend Set-Up in Gold Unchanged and Bullish

Short-term gains in WTI futures appear corrective - for now. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction. The trend condition in Gold is unchanged, the set-up remains bullish. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch lies at the 50-day EMA, at $4037.3. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

- WTI Crude down $0.17 or -0.29% at $58.71

- Natural Gas down $0.08 or -1.55% at $4.836

- Gold spot up $13.32 or +0.32% at $4203.5

- Copper down $7.45 or -1.37% at $537.1

- Silver up $0.38 or +0.65% at $58.5407

- Platinum down $9.9 or -0.6% at $1644.15

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 09/12/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 09/12/2025 | - | FOMC Meetings with S.E.P. | ||

| 09/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 09/12/2025 | 1415/1415 | BOE Lombardelli, Ramsden, Dhingra, Mann at TSC | ||

| 09/12/2025 | 1500/1000 | *** | JOLTS Jobs Opening Level | |

| 09/12/2025 | 1500/1000 | *** | JOLTS Quits Rate | |

| 09/12/2025 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 09/12/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/12/2025 | - | Bank of Canada Meeting | ||

| 10/12/2025 | 0130/0930 | *** | CPI | |

| 10/12/2025 | 0130/0930 | *** | Producer Price Index | |

| 10/12/2025 | 0700/0800 | *** | CPI Norway | |

| 10/12/2025 | 0700/0800 | ** | Private Sector Production m/m | |

| 10/12/2025 | 0900/1000 | * | Industrial Production | |

| 10/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 10/12/2025 | 1000/1000 | Chancellor Reeves Testifies at TSC on Budget | ||

| 10/12/2025 | 1045/1045 | BOE Bailey Pre-recorded Chat on Financial Stability | ||

| 10/12/2025 | 1055/1155 | ECB Lagarde Interview on Currencies/Digital Euro | ||

| 10/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 10/12/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 10/12/2025 | - | *** | Money Supply | |

| 10/12/2025 | - | *** | Social Financing | |

| 10/12/2025 | - | *** | New Loans | |

| 10/12/2025 | 1330/0830 | *** | Employment Cost Index | |

| 10/12/2025 | 1445/0945 | *** | Bank of Canada Policy Decision | |

| 10/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 10/12/2025 | 1530/1030 | BOC Press Conference | ||

| 10/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 10/12/2025 | 1900/1400 | ** | Treasury Budget | |

| 10/12/2025 | 1900/1400 | *** | FOMC Statement | |

| 10/12/2025 | 1930/1430 | Fed Chair Powell Press Conference |