MNI US OPEN - Trump Ups Tariff Ante, But Talks Ongoing

EXECUTIVE SUMMARY:

- TRUMP LEVELS 30% TARIFFS AGAINST EU, MEXICO - BUT TALKS ARE ONGOING

- EU READY TO USE "ALL TOOLS" ON TRADE, IN TALKS WITH OTHER NATIONS

- 'MAJOR STATEMENT' ON RUSSIA DUE, TRUMP MEETS WITH NATO SECGEN AT 1000ET

- EARNINGS SEASON BEGINS IN EARNEST TUESDAY IN BUSY START TO THE QUARTERLY CYCLE

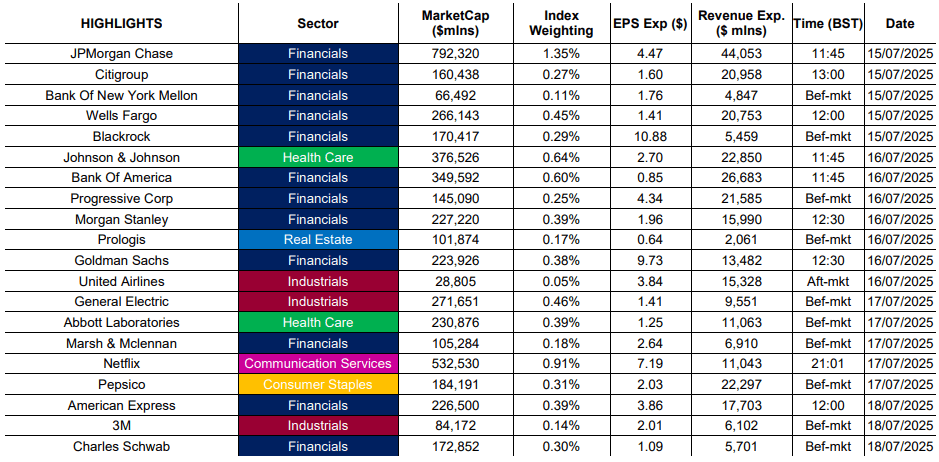

Figure 1: Earnings season kicks off in earnest Tuesday

NEWS

US/EU/MEXICO (BBG): Trump Threatens 30% Tariffs on EU and Mexico as Talks Continue

President Donald Trump unleashed his latest tariff ultimatums, declaring a 30% rate for Mexico and the European Union, as his trade agenda continues to keep allies off balance and inject uncertainty into global financial markets. Trump made the announcement in two letters posted to social media Saturday as he informed key trading partners of new rates that will kick in on Aug. 1 if they cannot negotiate better terms. The EU had been hoping to conclude a tentative deal with the US to stave off higher tariffs, but Trump’s letter punctured the recent optimism in Brussels over the prospects for an 11th-hour agreement between the major economies.

US-RUSSIA (MNI): Trump Expected To Announce UKR Weapons Package, Endorse RU Sanctions

1000ET/1500BST: President Donald Trump will hold a (closed press) White House meeting with NATO SecGen Mark Rutte, where he is expected to finalise a new plan to arm Ukraine "that is expected to include offensive weapons," per Axios. Later today, Trump is expected to make a 'major statement on Russia. No timing has been released.

US-UKRAINE (BBG): Trump Will Send Patriots to Ukraine, US ‘Not Paying’ for Them

President Donald Trump said the US will send more Patriot air-defense batteries to Ukraine, which Kyiv has said it needs to protect itself from Russian airstrikes. “I haven’t agreed on the number yet, but they are going to have some,” Trump told reporters Sunday on his way back to the White House. “We will get them Patriots, which they desperately need.”

US-JAPAN (BBG): Trump Criticizes Japanese Cars Again Ahead of Bessent Visit

US President Donald Trump attacked the car trade imbalance between the US and Japan again on Sunday, days ahead of a scheduled visit by Treasury Secretary Scott Bessent to the Asian country that could apply further pressure to the minority government. “They sell us millions and millions of cars a year. We sell them no cars because they won’t accept our cars. And they won’t accept much of our agriculture either,” Trump told reporters in Washington.

US-UK (WaPo): King Charles III to Host Trump in September for Second U.K. State Visit

President Donald Trump will make a three-day state visit this fall to the United Kingdom, where he will be hosted by King Charles III, giving him the unprecedented distinction of being granted a second visit of the kind. Buckingham Palace announced Monday that Trump had accepted the king's invitation to visit Britain from Sept. 17-19. He and his wife, first lady Melania Trump, will be hosted at Windsor Castle, the palace added, with further details to be announced later.

EU-US (MNI): EU Ready To Use "All Tools" If Needed - Rasmussen

Now is not the time for the EU to escalate trade tensions with the US, but the bloc's trade ministers who meet Monday should get ready to use all the "tools in its toolbox," Danish Foreign Minister Lars Rasmussen said. Speaking ahead of the meeting which he will chair, Rasmussen said that he hoped to get agreement on a second package of EU countermeasures, now estimated at around EUR70bn worth of US exports, in addition to the already agreed EUR20bn which was suspended at the weekend.

EU (BBG): EU Plans to Engage More With Other Nations Hit by US Tariffs

The EU is preparing to step up its engagement with other countries hit by Donald Trump’s tariffs following a slew of new threats to the bloc and other US trading partners, according to people familiar with the matter. The contacts with nations including Canada and Japan could include the potential for coordination, said the people, who spoke on condition of anonymity to discuss private deliberations.

BoE (The Times): Bank of England could cut interest rates if jobs market slows down

The Bank of England is ready to make larger cuts to interest rates if the jobs market shows signs of a pronounced slowdown, its governor has said. Andrew Bailey told The Times there was “consistent” evidence of businesses “adjusting employment” after Rachel Reeves increased employers’ national insurance contributions (NICs). He said Britain’s economy was growing behind its potential, opening up “slack” that would help to bring down inflation, which is expected to rise above 3.4 per cent when official figures for June are published this week.

BoJ (BBG): BOJ Is Said Likely to Consider Raising Price Outlook on Food

Bank of Japan officials are likely to consider raising at least one of their inflation forecasts at a policy meeting later this month, after rice and food-related prices rose more than expected, according to people familiar with the matter. The central bank will probably weigh increasing its key price forecast from 2.2% for this fiscal year after food inflation proved stronger than they expected at the beginning of May when the last quarterly outlook report was released, according to the people. Higher oil prices provide another reason for considering an upward revision, they said.

The People’s Bank of China will continue inplementing its moderately accommodative policy and boost existing measures in a bid to ensure hitting the annual economic growth target, deputy governor Zou Lan told reporters on Monday in a brief.

CHINA (MNI): China Not Seeking Yuan Depreciation Advantage

China does not seek international competitive advantage through yuan depretiation and remains committed to the decisive role of the market in the exchange rate, Zou Lan, vice governor of the People’s Bank of China, told reporters on Monday.

CRYPTO (BBG): Bitcoin Soars Past $120,000 as US Congress Starts ‘Crypto Week’

Bitcoin breached $120,000 for the first time, with investor enthusiasm showing few signs of dimming as the US House of Representatives prepares to consider key industry legislation during its “Crypto Week” starting Monday. The cryptocurrency bellwether rose as much 3.4% to $123,205 as of 9:10 a.m. in London as digital assets staged a broad advance. Ether, the second-largest token, also gained, along with a host of smaller coins. The crypto gains came as stock markets across Europe retreated.

EQUITIES: An Unusually Busy Start to Quarterly Earnings Season

Quarterly earnings season kicks off in earnest today, and it's an unusually busy start to the quarter. 9.4% of the S&P 500's market cap is set to report, with the usual early focus on big banks and financials. Our full quarterly earnings schedule found here, including EPS, revenue expectations and full timings: https://mni.marketnews.com/44tWRA8

Highlights are:

- TUES: JP Morgan, Citigroup, BNY Mellon, Wells Fargo, Blackrock

- WEDS: Johnson & Johnson, Bank of America, Morgan Stanley, Goldman Sachs

- THURS: General Electric, Netflix, PepsiCo

- FRI: American Express, 3M, Charles Schwab

DATA

China's total social financing rose by CNY4.2 trillion in June to hit a three-month high, nearly doubling May's CNY2.29 trillion, mainly driven by accelerated government bond sales, data released on Monday by the People's Bank of China showed.

CHINA (MNI): China's H1 Exports Up 5.9%, Imports Down 3.9%

China's first half exports increased 5.9% y/y, with imports narrowing to a 3.9% decline from the 7.0% drop in Q1, data released by China Customs showed on Monday. Exports in June reached USD325.1 billion, up 5.8% y/y, exceeding Mays 4.8% and the forecasted 5.2%. Imports rose 1.1% in June, the first positive change in four months and beating the market consensus of 0.5%.

JAPAN (MNI): MNI BRIEF: BOJ Survey 5-Yr Inflation Forecast Remains At 5%

Japan's five-year household median inflation forecast remained at 5% in June, unchanged from three months ago, with the number of households anticipating a price rise decreasing to 85.1% from 86.7% previously, the BOJ’s quarterly consumer survey showed on Monday.

MNI: SWEDEN FINAL JUN CPIF +2.8% Y/Y

EGBS: German Curve Twist Steepens, Short End Yields Lower On Tariff Fears

The German curve has lightly twist steepened, with Schatz yields down 2.5bps at 1.87% and 30-year yields up 1bp at 3.24%. Short-end yields have been pulled lower by US President Trump's 30% EU tariff announcement over the weekend. Still, dovish repricing in short-end EUR rates has been limited by (i) an escalated tariff rate already being embedded in expectations ahead of the weekend and (ii) scope for negotiations between now and August 1 resulting in a lower overall tariff rate.

- 30-year Bund yields reached a high of 3.254% this morning, partly a spillover from the latest upward pressure in long-end JGB yields.

- Bund futures are +12 at 129.29, with volumes levelling off somewhat over the last 90 minutes. A bear cycle remains intact, with initial support the intraday low of 129.11. Clearance would expose 128.97, the May 14 low.

- The EU will kick off issuance for the week today with up to E5bln of 3/9/30-year EU-bonds. The auction will be the smallest triple-tranche auction since these were launched in April.

- 10-year EGB spreads to Bunds are biased wider, with Trump’s tariff announcement denting equity risk sentiment. The BTP/Bund and OAT/Bund spreads are 1.5bps wider. There will be some focus on tomorrow’s French budget outline announcement, presenting fresh risks for OATs.

GILTS: Bailey Drives Bull Steepening & Dovish Repricing

Dovish weekend commentary from BoE Governor Bailey, pointing to the potential for easier BoE policy if the labour market deteriorates quicker than the Bank expects, followed by a softer-than-expected REC Labour market report, has driven front end outperformance.

- Gilt futures have hit fresh session highs in recent trade, after briefly piercing Friday’s low early on. Contract last +10 at 91.79.

- Bears remain in technical control and eye the July 8 low (91.42). Conversely, bulls need to clear the July 10 high (92.19).

- Yields flat to 4bp lower, pre-existing July ranges intact across the curve.

- 2s10s registers the highest level since April, 79.2bp, and is on track to register the highest close of ’25. The April 9 high (84.6bp) provides the next major upside target.

- 5s30s trades back above 140bp, with the ’25 intraday high (147.2bp) providing the next upside area of interest.

- GBP STIRs react dovishly to Bailey’s comments and the subsequent REC release.

- SONIA futures now +0.5 to +6.5, SFIZ5 hit a fresh July high.

- BoE-dated OIS shows ~58bp of cuts through year-end. a reminder that moves through 55bp have failed in recent weeks, but fresh dovish signals from the Bank may make this move more meaningful.

- Inflation & labour market data, as well as the Mansion House event, present the key UK risk events this week. Please read our Global Week Ahead email for more colour on those events and expect our full preview in due course.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 3.996 | -22.1 |

Sep-25 | 3.917 | -30.1 |

Nov-25 | 3.735 | -48.2 |

Dec-25 | 3.641 | -57.7 |

Feb-26 | 3.507 | -71.0 |

Mar-26 | 3.475 | -74.2 |

FOREX: EUR and MXN Unfazed by Latest Global Tariff Developments

- Despite President Trump threatening to impose 30% tariffs on the EU and Mexico, both the Euro and the Mexican peso have taken the news in their stride as markets remain cautiously optimistic that more lenient deals may be struck before the August 01 deadline. These limited reactions, and the lack of data on Monday keeps the dollar index within close proximity to Friday’s close.

- For EUR specifically, the brief bout of initial weakness did prompt a fresh pullback low at 1.1651 and notably, the 20-day EMA has been pierced. However, the lack of follow through shows that these shallow dips remain corrective, keeping bullish sentiment firmly intact for now. The July 01 high of 1.1829 remains the bull trigger for the pair.

- In similar vein, the USDMXN trend remains bearish, reinforced by fresh cycle lows for the pair last week. Potential is seen for a bearish extension towards 18.4302, the Aug 01 low.

- Elsewhere in G10, the likes of AUD and NZD are both underperforming in G10, however, it’s the Kiwi’s relative weakness that is helping AUDNZD extend its most recent upswing. The cross looks set to extend its winning streak to six consecutive sessions, shifting the upside target to 1.1032, the April 01 high.

- Tuesday’s data calendar is stacked with China activity figures kicking things off. The focus will then swiftly turn to US and Canadian inflation data, final inputs before both the Fed and BOC decisions on July 30. We will also have the beginning of quarterly earnings season with financials the usual early focus.

The bull cycle in Gold that started Jun 30, remains intact and the yellow metal is holding on to its recent gains. Note that medium-term trend conditions are bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend. WTI futures maintain a bearish tone following the reversal from the Jun 23 high, and recent gains still appear corrective. Support to watch is the 50-day EMA, at $65.39. The average has been pierced, a clear break of it would signal scope for a deeper retracement.

- WTI Crude up $0.67 or +0.98% at $69.11

- Natural Gas up $0.15 or +4.56% at $3.464

- Gold spot up $10.96 or +0.33% at $3366.52

- Copper down $6.35 or -1.13% at $554.75

- Silver up $0.57 or +1.49% at $38.9868

- Platinum up $4.1 or +0.29% at $1397.08

EQUITIES: Stocks Hold Bullish Poise Into Earnings Season

The trend condition in S&P E-Minis remains bullish and short-term weakness is considered corrective. Recent activity has resulted in a break of resistance at 6128.75, the Jun 11 high. The breach confirmed a resumption of the uptrend that started Apr 7. Eurostoxx 50 futures traded higher last week as the contract extended the recovery that started Jun 23. This exposed key resistance and the bull trigger at 5486.00, the May 20 high. It has been pierced, a clear break of it would confirm a resumption of the medium-term bull cycle.

- Japan's NIKKEI closed lower by 110.06 pts or -0.28% at 39459.62 and the TOPIX ended 0.43 pts lower or -0.02% at 2822.81.

- Elsewhere, in China the SHANGHAI closed higher by 9.473 pts or +0.27% at 3519.65 and the HANG SENG ended 63.75 pts higher or +0.26% at 24203.32.

- Across Europe, Germany's DAX trades lower by 182.55 pts or -0.75% at 24071.87, FTSE 100 higher by 29.05 pts or +0.32% at 8969.34, CAC 40 down 42.86 pts or -0.55% at 7786.04 and Euro Stoxx 50 down 36.81 pts or -0.68% at 5346.2.

- Dow Jones mini down 178 pts or -0.4% at 44422, S&P 500 mini down 21.25 pts or -0.34% at 6267.75, NASDAQ mini down 73.25 pts or -0.32% at 22887.25.

| Date | GMT/Local | Impact | Country | Event |

| 14/07/2025 | 1230/0830 | ** | Wholesale Trade | |

| 14/07/2025 | 1500/1700 | ECB Cipollone At EU Parliament | ||

| 14/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 14/07/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/07/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 15/07/2025 | 0200/1000 | *** | GDP | |

| 15/07/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 15/07/2025 | 0200/1000 | *** | Retail Sales | |

| 15/07/2025 | 0200/1000 | *** | Industrial Output | |

| 15/07/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 15/07/2025 | 0700/0900 | *** | HICP (f) | |

| 15/07/2025 | 0900/1100 | ** | Industrial Production | |

| 15/07/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/07/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 15/07/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/07/2025 | 1315/0915 | Fed Vice Chair Michelle Bowman | ||

| 15/07/2025 | 1645/1245 | Fed Governor Michael Barr | ||

| 15/07/2025 | 1845/1445 | Boston Fed's Susan Collins | ||

| 15/07/2025 | 2000/2100 | Mansion House: Chancellor Reeves and BOE Bailey | ||

| 15/07/2025 | 2245/1845 | Dallas Fed's Lorie Logan |