MNI US OPEN - NFP Growth Seen at 104k in July

EXECUTIVE SUMMARY

- MNI US PAYROLLS PREVIEW - EARLY TEST OF LATEST POWELL PATIENCE

- TRUMP RAISES TARIFFS ON CANADA TO 35%, KEEPS USMCA EXEMPTION

- JAPAN’S KATO VOICES CONCERN WITH YEN AT WEAKEST SINCE MARCH

- EUROZONE JULY HICP MARGINALLY ABOVE CONSENSUS

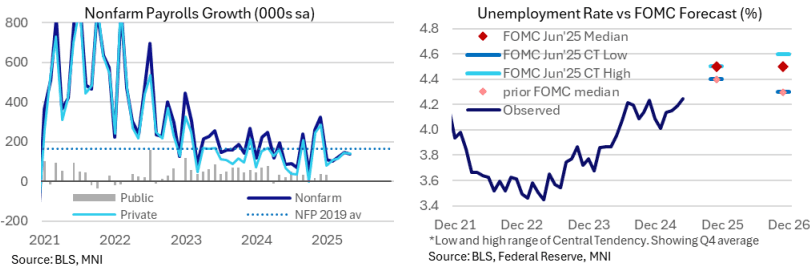

Figure 1: Recent US labour market developments

NEWS

MNI US PAYROLLS PREVIEW: Early Test of Latest Powell Patience

Nonfarm payrolls growth is seen at 104k in July (sa) per the broad Bloomberg survey after 147k in June. The median primary dealer analyst eyes 100k whilst the Bloomberg whisper currently sits at 115k after little net reaction to the stronger than expected ADP report for July. Government payroll growth is expected to be much softer after a surprise 73k surge in June, which we think was more likely down to seasonal adjustment quirks. There’s a wide range of primary dealer estimates for public payrolls growth in July, from +20k to -55k.

US (BBG): Trump’s 40% Penalty for Tariff Dodging Still Missing Key Details

President Donald Trump has threatened to pile an additional 40% tariff on any product that Washington determines to be “transshipped” through another country, a punishment aimed at stopping goods mainly from China dodging US duties. That penalty was included in the White House announcement Thursday evening that laid out global tariff rates from 10% to 41%. But many countries are still missing the “rules of origin” details necessary to determine what the US considers transshipped.

US/CANADA (BBG): Trump Raises Tariffs on Canada to 35%, Keeps USMCA Exemption

President Donald Trump said the US will put a 35% tariff on some imports from Canada, escalating the tensions between two countries that have impaired one of the world’s largest trading relationships. The new rate represents an increase from the 25% tariffs Trump imposed in early March under an emergency law. “Canada has failed to cooperate in curbing the ongoing flood of fentanyl and other illicit drugs, and it has retaliated against the United States” for Trump’s earlier tariffs, the White House said in a fact sheet published Thursday evening.

US/JAPAN (BBG): Japan to Seek Car Tariff Cut, Secure Automakers’ Competitiveness

Japan will keep pressing the US to cut tariffs on cars and auto parts to 15% as promised in a trade deal and work to ensure the nation’s automakers remain competitive against their rivals, according to the nation’s chief trade negotiator. “We will continue to urge the US side to promptly take measures to implement the recent agreement, including the reduction of tariffs on cars and car parts,” Ryosei Akazawa said on Friday in Tokyo. “We want the US to fulfill its commitments, and Japan will also do what we promised to do.”

US/RUSSIA (BBG): Trump Says Witkoff to Visit Russia, Expects to Impose Sanctions

US President Donald Trump said special envoy Steve Witkoff would be headed to Russia after wrapping up a visit to Israel ahead of a new deadline for Moscow to halt its fight with Ukraine. “Yeah, going to Israel and then he’s going to Russia, believe it or not,” Trump told reporters at the White House on Thursday. Trump also said he expected to impose sanctions once a new deadline he set earlier this week expires, but did not foresee that it would alter Russian President Vladimir Putin’s behavior.

US/CHINA (MNI EXCLUSIVE): China Likely to Insist U.S. Tariffs Drop to 10% - Advisors

Chinese policy advisors detail their expectations for continuing trade talks with the U.S. after the Stockholm round. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

US/CHINA (BBG): China Says US Exploited Old Microsoft Flaw for Cyberattacks

China accused the US of exploiting a flaw in Microsoft Corp.’s email servers to steal military data and launch cyberattacks on its defense sector. The Cyber Security Association of China said in a statement Friday that US actors had been linked to two major cyberattacks on Chinese military companies, without naming them. They exploited flaws in Microsoft Exchange to control the servers of a key company in the defense sector for nearly a year, it added.

US/CHINA (WSJ): Congress Looks to Punish China While Trump Pursues Trade Deal

Lawmakers in both houses of Congress introduced legislation targeting China on Thursday, a reminder of Capitol Hill’s deep-seated desire to punish Beijing over human rights even as President Trump gives priority to a trade deal. The bipartisan bills touch on issues that have long vexed American policymakers, namely signs that Beijing tries to stifle Chinese dissent in the U.S. and that, at home, it has abused ethnic minorities including Uyghurs.

US (BBG): Trump Demands Drugmakers Slash US Prices in Blow to Industry

President Donald Trump escalated his campaign to pressure pharmaceutical companies to lower drug prices, sending letters to 17 of the world’s largest drugmakers demanding they charge the US what other countries pay for new medicines. In the letters, sent to Eli Lilly & Co., Novo Nordisk A/S, Pfizer Inc. and others, Trump insisted companies immediately lower what they charge Medicaid for existing drugs. He also asked them to guarantee that future medicines be launched and remain at prices on par with what they cost overseas.

JAPAN (BBG): Japan’s Kato Voices Concern With Yen at Weakest Since March

Japan’s Finance Minister said he’s worried by movements in the yen, which weakened to levels last seen in March following dovish messaging on interest rates from the Bank of Japan. “The government is deeply concerned about trends in the currency market, including speculative movements,” Finance Minister Katsunobu Kato told reporters on Friday. “It’s important for exchange rates to remain stable, reflecting economic fundamentals,” he added.

BOJ (MNI): BOJ Warns of Drop in Corp Profts; Impact on Wages

The Bank of Japan warned on Friday that corporate profits are increasingly likely to decline in fiscal 2025 due to the direct and indirect effects of U.S. tariff hikes, according to the full text of its Outlook Report. In the June 2025 Tankan survey, while nonmanufacturing firms’ forecasts for current profits in fiscal 2025 remained resilient, manufacturers – particularly in the processing sector – projected a decline in earnings, the report said.

SWITZERLAND (MNI): KOF Sees 0.3% - 0.6% Negative GDP Impact of Announced US Tariffs

The Swiss KOF institute has given a first view on the potential impact of the 39% tariff rate announced overnight by the US administration on Switzerland: The "impact would depend largely on whether the pharmaceutical industry, which accounts for by far the largest share of exports to the US, would also be affected by tariffs of a similar magnitude." "With reciprocal tariffs of 39% on Swiss goods exports to the US (excluding pharmaceuticals) and 15% on exports from the European Union (EU), as well as a 10% tariff on pharmaceutical products from Switzerland, a significant reduction in gross domestic product (GDP) is to be expected. Depending on the possibility of trade diversion and the time horizon, these would range from 0.3% of GDP to 0.6% of GDP per year. A decline in GDP of at least 0.3% is therefore to be expected."

SWITZERLAND (MNI): Gov't Does Not Expect 39% Tariffs to Hit Pharma Sector

A spox for the Federal Department of Economic Affairs has told Reuters that the gov't does not expect the 39% 'reciprocal' tariffs to come into effect from 7 August on Swiss exports to the US to include the pharmaceuticals sector. The 39% rate puts Switzerland among the most heavily-penalised nations worldwide under the 'reciprocal' tariff regime, behind only Brazil (with whom's leader US President Donald Trump is involved in a bitter verbal spat), Syria, Laos and Myanmar.

CORPORATE (FT): Apple Posts Strong Earnings but Tariff Fears Spook Investors

Apple posted much better than expected revenue on Thursday for the quarter to the end of June, despite the threat of President Donald Trump’s trade war, as iPhone sales surged. Revenue was up about 10 per cent year on year to $94bn, well above consensus estimates of $89.3bn. Global iPhone sales were up 13.5 per cent year on year at $44.6bn. The strong earnings are a boost to Apple which has been heavily hit by Trump’s trade and tariff agenda since his “liberation day” announcements in April, which wiped about $700bn off its market capitalisation.

DATA

EUROPEAN DATA (MNI): Eurozone July HICP Marginally Above Consensus

- EUROZONE JUL FLASH HICP +2% Y/Y

- EUROZONE JUL FLASH CORE HICP +2.3% Y/Y

Eurozone July flash HICP Y/Y inflation came in at 2.02%, 12 hundredths above the rounded consensus of 1.9% (vs 1.99% June). On a monthly basis, Eurozone inflation came in at 0.00% (-0.1% cons). Core HICP was broadly in line with consensus, at 2.29% Y/Y and -0.18% M/M (2.3% Y/Y cons; June 2.31% Y/Y). Looking at the individual categories: Services inflation printed lower than previously at 3.13% (3.32% June) - the rounded 3.1% print was the lowest since March 2022. The median analyst looked for a 3.2% reading ahead of the national-level data, so that was a marginal downward surprise for the category.

EUROZONE JULY MANUF PMI 49.8 (49.8 FLASH, 49.5 JUNE) (MNI)

GERMANY JULY MANUF PMI 49.1 (49.2 FLASH, 49.0 JUNE) (MNI)

UK JULY MANUF PMI 48.0 (48.2 FLASH, 47.7 JUNE) (MNI)

SPAIN DATA (MNI): Manuf PMI Broadly in Line; Output Picking Up, Confidence Soft

- SPAIN JULY MANUF PMI 51.9 (51.8 FCAST, 51.4 JUNE)

Spanish manufacturing PMI broadly in line with expectations at 51.9 (51.8 consensus, 51.4 June). For output "The solid improvement in operating conditions was the best of the year so far and represented a third successive month of growth." It was a mixed report: "jobs in the sector were added for a fifth successive month, with [employment] growth improving to its strongest since December 2024" while there was "another monthly increase in production, which was linked by firms to the start of new projects plus a rise in demand. Overall new orders increased modestly, but growth was the best recorded since the end of 2024."

ITALY DATA (MNI): Manufacturing PMI Marginally Below 50 but Encouraging Factors

- ITALY JULY MANUF PMI 49.8 (48.7 FCAST, 48.4 JUNE)

Italian PMI manufacturing came in stronger than expected at 49.8 in July (48.7 exp, 48.4 June). This is the highest print since March 2023 and only marginally below the 50 breakeven threshold. The details were marginally encouraging. The following from the press release: "There were signs that the downturn had subsided at the start of the third quarter. New orders declined at a marginal rate, while output fell to a softer degree compared to the month prior."

CHINA DATA (MNI): S&P China Mfg. PMI Falls Into Contraction in July

- CHINA JUL S&P MANUFACTURING PMI 49.5 VS 50.4 IN JUN

MNI (Beijing) China's S&P manufacturing PMI, previously known as the Caixin manufacturing PMI, came in at 49.5 in July, up from June's 50.4, falling back into the contraction zone below the 50 mark, as factory output scaled back amid a slower increase in new orders, the company said on Friday. After rising in June, the production sub-index declined during July, marking the second time in which production has fallen since October 2023, though the rate of contraction was only modest. The new order sub-index growth slowed since June, with the new export order sub-index contracted for a fourth straight month and at a faster pace than in June.

JAPAN DATA (MNI): Jobless Rate Steady, but Job-To-Applicant Ratio Falls to Fresh Lows

- JAPAN JUNE JOBLESS RATE UNCHANGED FROM MAY AT 2.5%

Earlier data showed mixed June labor market conditions. The unemployment rate was steady at 2.5%. This was in line with market forecasts. The unemployment rate has been steady at 2.5% since March of this year. This is just up from cycle lows of 2.4%. However, the job to applicant ratio rose fell to 1.22 from 1.24 prior, which was also below the 1.25 consensus expectation. This is the lowest job-to-applicant ratio since 2022.

FOREX: CHF the Worst Performer on Tariff Import to the US

- The Dollar was mostly mixed overnight going into the European session, but the big risk off tone seems to have provided some buying interest in the greenback, it is now back in the green versus all G10s, only the Yen is up 0.16%.

- While the manufacturing PMIs had no impact on cross assets, there might have been some early positioning ahead of the US NFP, bonds also sold off in early trade, keeping the yields elevated but futures contracts have since pared some of their losses.

- The main mover in G10 is the Swissy, which is now down 0.58% following the announcement that the US will put 39% tariffs on Swiss imports to the US.

- USDCHF remains near the session high at the time of typing, and next upside resistance will be eyed at 0.8216.

- The Second worst performer within G10s is the Kiwi, down 0.44% to trade at its worst level since mid May.

- Next immediate support in NZDUSD will be at 0.5847, this is May's low and lowest print since mid April.

- Looking ahead, US NFP is the main focus, US ISM will also be watched, while the Mfg PMI and Michigan are final reading.

- US NFP Range, 0k/170k, median 104k, Whisper 120k.

BONDS: Off Lows, Bear Steepening Holds

EGBs recover from session lows, with weakness in equities (albeit initially aided by higher yields) and a downtick in crude oil providing some background support.

- No clear fresh fundamental driver for the initial weakness in core global FI, with cues from the U.S., digestion of the U.S. tariff announcements and the impending NFP release front and centre for participants.

- Initial support in Bund futures (129.19) is intact, German yields flat to 2bp higher, curve steeper.

- EGB spreads to Bunds flat to 3bp wider, peripherals & OATs see the most meaningful 10-Year spread moves.

- EUR 3m10y vol. is little changed to a touch higher today after the 60bp level held. Note that the measure registered the lowest level seen since February ’22. The trend lower has provided background support for EGB spread tightening vs. Bunds for some time, albeit with this morning’s weakness in equities seemingly spilling over into a modest uptick in the measure/light EGB spread widening.

- Elsewhere, there has been ongoing demand for the ERH6 98.31/98.43 call spread vs. the ERH6 97.93/97.81 put spread, with turnover in that strategy taking volume to ~50K of new risk on the week.

- No meaningful impact from slightly firmer-than-expected Eurozone HICP.

- The removal of yesterday’s month-end support and cues from wider core global FI markets has resulted in ~3bp of gilt widening vs. Bunds.

- Gilt futures stick to the range witnessed so far this week, last -50 at 91.66.

- Yields 2.5-5.5bp higher, 10s still trade in the middle of the range in play since early Feb.

- BoE-dated OIS showing ~45bp of cuts through year-end.

EQUITIES: Trend Condition in Eurostoxx Futures Bullish, S/T Weakness Corrective

The trend condition in Eurostoxx 50 futures is bullish and S/T weakness appears corrective. Support at 5281.00, the Jul 1 / 4 low, has been pierced. A clear break of it would strengthen a bearish threat and expose the reversal trigger at 5194.00, the Jun 23 low. For bulls, a stronger resumption of gains would refocus attention on 5486.00, the May 20 high. It has recently been pierced, a clear breach of it would resume the bull cycle and open 5500.00. The trend set-up in S&P E-Minis remains bullish and short-term weakness is considered corrective. A fresh cycle high this week maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, a Fibonacci projection. Key support is at the 50-day EMA, at 6189.50. Support at the 20-day EMA is at 6333.64.

- Japan's NIKKEI closed lower by 270.22 pts or -0.66% at 40799.6 and the TOPIX ended 5.58 pts higher or +0.19% at 2948.65.

- Elsewhere, in China the SHANGHAI closed lower by 13.256 pts or -0.37% at 3559.952 and the HANG SENG ended 265.52 pts lower or -1.07% at 24507.81.

- Across Europe, Germany's DAX trades lower by 419.81 pts or -1.74% at 23645.28, FTSE 100 lower by 62.08 pts or -0.68% at 9070.75, CAC 40 down 141.3 pts or -1.82% at 7630.67 and Euro Stoxx 50 down 91.38 pts or -1.72% at 5228.54.

- Dow Jones mini down 408 pts or -0.92% at 43897, S&P 500 mini down 61.25 pts or -0.96% at 6313.75, NASDAQ mini down 259 pts or -1.11% at 23106.75.

Time: 10:00 BST

COMMODITIES: WTI Futures Holding Onto the Bulk of This Week’s Gains

WTI futures are holding on to this week’s gains. The climb marks an extension of the current corrective cycle. $69.41, the 50.0% retracement of the Jun 23-24 downleg, has been cleared. A continuation higher would open $70.96 next, the 61.8% retracement point. On the downside, support to watch is the 50-day EMA, at $65.37. The average has been pierced, a clear break of it would expose $58.17, the May 30 low. Gold has pulled back from its Jul 23 high. Short-term weakness is considered corrective - for now - and a bull cycle that started Jun 30 remains intact. However, the yellow metal has traded through support at $3319.9, the 50-day EMA. A clear break of this level signals scope for a deeper retracement and exposes the next key support at $3248.7, the Jun 30 low. Key near-term resistance is $3439.0, the Jul 23 high. A break of this hurdle would be bullish.

- WTI Crude down $0.36 or -0.52% at $68.91

- Natural Gas down $0.01 or -0.19% at $3.1

- Gold spot up $4.53 or +0.14% at $3294.09

- Copper up $2.7 or +0.62% at $438.1

- Silver down $0.28 or -0.76% at $36.4326

- Platinum down $25 or -1.93% at $1267.13

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 01/08/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/08/2025 | 1230/0830 | *** | Employment Report | |

| 01/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/08/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/08/2025 | 1400/1000 | * | Construction Spending | |

| 01/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 01/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 01/08/2025 | 1400/1000 | * | Construction Spending | |

| 01/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |