EUROPEAN INFLATION: Eurozone July HICP Marginally Above Consensus

Aug-01 09:02

Eurozone July flash HICP Y/Y inflation came in at 2.02%, 12 hundredths above the rounded consensus of 1.9% (vs 1.99% June). On a monthly basis, Eurozone inflation came in at 0.00% (-0.1% cons).

- Core HICP was broadly in line with consensus, at 2.29% Y/Y and -0.18% M/M (2.3% Y/Y cons; June 2.31% Y/Y).

- Looking at the individual categories:

- Services inflation printed lower than previously at 3.13% (3.32% June) - the rounded 3.1% print was the lowest since March 2022. The median analyst looked for a 3.2% reading ahead of the national-level data, so that was a marginal downward surprise for the category.

- Non-energy industrial goods, at 0.75% (0.52% June), were notably firmer than the 0.5% Y/Y analysts had been looking for. Some national-level data points towards either changing seasonality in or a lower magnitude of clothing summer sales than last year here.

- Energy inflation was little changed vs June, at -2.46% (June -2.59%).

- Food, alcohol and tobacco inflation meanwhile accelerated again in July, to 3.27%, with the unrounded 3.3% reading the highest since February 2024 (3.07% June). Analysts were looking for a softer 3.1% reading in the category.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

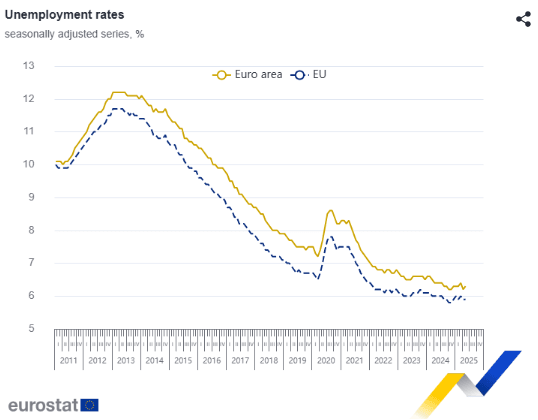

MNI: EUROZONE MAY UNEMPLOYMENT RATE 6.3%

Jul-02 09:00

- MNI: EUROZONE MAY UNEMPLOYMENT RATE 6.3%

EUROZONE DATA: Unemployment Rate Ticks Up To 6.3%

Jul-02 09:00

The Eurozone unemployment rate unexpectedly ticked up to 6.3% in May but remains close to the 6.2% cycle lows seen in April (consensus was for an unchanged print).

GERMAN AUCTION PREVIEW: 2.60% Aug-35 Bund

Jul-02 08:37

This morning, Germany will open its new on-the-run 10-year 2.60% Aug-35 Bund (ISIN: DE000BU2Z056) for E6bln.

- The size of this auction was increased by E1bln from E5bln in the Q3 calendar update. The E6bln auction size is the largest for a non-Schatz German auction since 2011 (and the largest of any German auction since September 2023). This is also the only E6bln German auction scheduled for Q3.

- Demand metrics in German auctions have recovered recently after a phase of weakness towards the beginning of Q2, and that also applies to the 10-year segment. At the last June 11 auction of the (previous on-the-run) 2.50% Feb-35 Bund, the bid-to cover came in at 2.69x and the bid-to-offer at 2.09x - a significant improvement from the 1.38x bid-to-cover / 1.06x bid-to-offer seen at a weak auction in late April. These metrics compare to a 1.38x - 2.84x range for bid-to-covers and a 1.06x - 2.17x range for bid-to-offers seen in German 10y auctions this year.

- At the last two 10y auctions (Jun 11, May 21), the secondary market mid-price has also been below the lowest accepted price again - contrary to the two 10y auctions ahead of that.

- Germany last week announced its 2025 budget details and 2026-29 broad financial plans, with the resulting issuance ramp-up, on balance, being perceived as quicker than expected by analysts previously. For our view on the events, see here.

- The next German auction will be E5bln of the new Oct-30 Bobl (ISIN: DE000BU25059) on June 8, while the 2.60% Aug-35 Bund will be re-opened on July 23, also for E5bln.

- Timing: Results will be available shortly after the bidding window closes at 10:30GMT / 11:30CET.

Trending Top

May-22 16:54