MNI US OPEN - Iran Seeks Diplomacy Push to Avert War With US

EXECUTIVE SUMMARY

- HOUSE’S BID TO END PARTIAL SHUTDOWN GETS TOUGHER – WSJ

- IRAN HOPES MIDDLE EAST DIPLOMACY PUSH WILL AVERT WAR WITH US

- JAPAN’S TAKAICHI CLARIFIES WEAK YEN REMARKS FROM ELECTION RALLY

- CHINA MANUFACTURING PMI FALLS BELOW 50 IN JANUARY

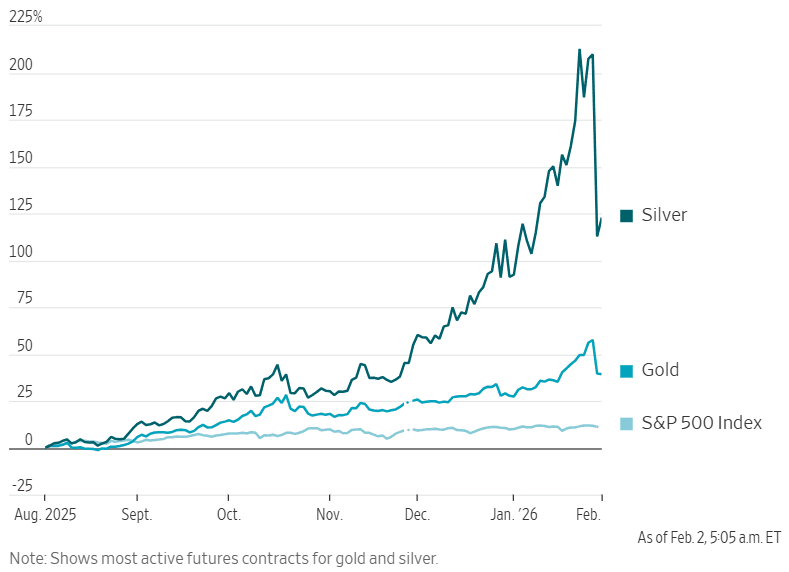

Figure 1: Price performance, past six months

Source: Wall Street Journal, FactSet

NEWS

US (WSJ): House’s Bid to End Partial Shutdown Gets Tougher

Speaker Mike Johnson (R., La.) faces a tougher-than-expected vote to end a partial government shutdown this week, after House Democrats pushing for sweeping changes to immigration enforcement signaled they wouldn’t help Republicans pass any funding measures through the narrowly divided chamber. Johnson, with a 218-213 majority, will need to keep almost all Republicans on board or risk the shutdown that started Saturday stretching deep into the week. The measure, endorsed by President Trump, funds swaths of the government for the rest of the fiscal year, while providing a two-week extension for the Department of Homeland Security—which contains immigration-enforcement agencies. The extension is intended to jump-start talks on reining in enforcement officials’ practices.

US/IRAN (BBG): Iran Hopes Middle East Diplomacy Push Will Avert War With US

Iran hopes that diplomatic efforts to avert a war with the US will bear fruit within days, the Islamic Republic’s foreign ministry said on Monday. Multiple countries in the Middle East have acted as intermediaries to exchange messages with the US, Esmail Baghaei, a spokesman for the ministry, said. He added that any military conflict “won’t be confined to Iran’s geographic boundaries.” “We are reviewing and making decisions on the details of each diplomatic track, which we hope will yield results in the coming days,” he said.

US (WSJ): Texas Election Upset Is a ‘Wake-Up Call’ for Future Elections, Republican Says

A state-level Democratic win in a Texas region that voted for President Trump by 17 points threatens to diminish the GOP’s hopes for the midterm elections, in what one of the state’s most powerful Republicans dubbed a “wake-up call.” Democrat Taylor Rehmet defeated Republican Leigh Wambsganss on Saturday for a state Senate seat by 14 points, in a solidly red district that includes part of Fort Worth. While Republicans including Texas Lt. Gov. Dan Patrick had been sounding alarms about the North Texas race being too close for comfort in recent weeks, the 31-point-swing leftward was a surprise across the board. The loss is a “wake-up call for Republicans across Texas,” Patrick wrote on social media after the race. “Our voters cannot take anything for granted.”

US (WSJ): The Housing Market Is Swinging Toward Buyers

Many home shoppers have given up on the depressed housing market, where sales are stuck at a 30-year low. But those buying are enjoying discounts at the highest rate in years. About 62% of buyers last year purchased a home below the original listing price. That was the highest proportion since 2019, according to a new analysis by the real-estate brokerage Redfin. The average discount for the homes that sold below their original listing price was around 8%—the largest since 2012.

CORPORATE (BBG): Oracle to Raise Up to $50 Billion This Year for Cloud Push

Oracle Corp. plans to raise $45 billion to $50 billion this year through a combination of debt and equity sales to build additional cloud infrastructure capacity, reflecting the scale of financing needed to feed AI’s growth. Oracle is raising money to build additional capacity to meet the contracted demand from the company’s largest cloud customers, including Advanced Micro Devices Inc., Meta Platforms Inc., Nvidia Corp., OpenAI, TikTok Inc. and xAI Corp., the company said in a statement Sunday.

BITCOIN (BBG): Bitcoin Flirts With Lowest Price Since Trump’s Return to Office

Bitcoin fell to a 10-month low in Asia trading Monday following a weekend selloff, with sentiment fragile amid broader market turbulence. The largest cryptocurrency fell as much as 2.5% to $74,541, just shy of its lowest level since Donald Trump retook the White House a little more than a year ago. That was $74,425 recorded on April 7. It remained below $76,000 at 6:30 a.m. in London.

JAPAN (BBG): Japan’s Takaichi Clarifies Weak Yen Remarks From Election Rally

Japanese Prime Minister Sanae Takaichi sought to clarify her comments about the weak yen, emphasizing that she only intended to argue for a need to create an economy that can withstand currency fluctuations. “I did not say that a strong yen is good or that a weak yen is bad,” the prime minister said on Sunday in a post on X. “I said that I want to build a strong economic structure that is resilient to exchange-rate fluctuations.”

BOJ (MNI): Early Rate Hikes, Upside Risks to Prices - BOJ Opinions

Several Bank of Japan board members saw the need to raise the policy interest rate relatively early, with one favouring hikes at intervals of a few months, according to the summary of opinions from the Jan. 22-23 meeting released Monday. “It is appropriate for the Bank to raise the policy interest rate at intervals of a few months, while examining the impact of rate hikes on firms' and households' behaviour through anecdotal information and assessing the current policy interest rate relative to the neutral rate,” said one member at the meeting, which saw the policy rate hold at 0.75%.

CHINA (MNI EXCLUSIVE): Yuan in Slow Rally Amid Dollar Weak Cycle - Advisors

Chinese policy advisors give their latest outlook for the yuan. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

DATA

EUROZONE JAN FINAL MANUF PMI 49.5 (49.4 FLASH, 48.8 DEC) (MNI)

GERMANY JAN FINAL MANUF PMI 49.1 (48.7 FLASH, 47.0 DEC) (MNI)

FRANCE JAN FINAL MANUF PMI 51.2 (51.0 FLASH, 50.7 DEC) (MNI)

UK JAN FINAL MANUF PMI 51.8 (51.6 FLASH, 50.6 DEC) (MNI)

GERMANY DATA (MNI): Christmas Retail Sales Net Positive

- GERMANY DEC RETAIL SALES +0.1% M/M, +1.5% Y/Y (VS -0.5% M/M, +1.3% Y/Y NOV)

German headline December retail sales were as expected in December, although there was a downward revision of the November data. Christmas business was overall net positive this year compared to last according to Destatis. Retail sales volumes were 0.1% M/M (cons +0.1%) in December on a seasonally and calendar adjusted basis after a 0.5% decrease (initial -0.6% but a first revision to -0.3% was already known) in November. For 2025 as a whole, Destatis now estimate a 2.7% real gain vs 2024, after a 2.4% projection following the November figures.

SPAIN DATA (MNI): Jan Manuf PMI Below Consensus on Weak New Orders

- SPAIN JAN MANUF PMI 49.2 (49.9 EXP, 49.6 DEC)

The Spanish manufacturing PMI was weaker-than-expected at 49.2 (vs 49.9 cons, 49.6 prior), the lowest since April 2025. A decline in new orders was the main driver of the pullback, with the EUR/USD exchange rate noted as one factor weighing on export orders. Note that in Friday's Q4 flash GDP report, INE wrote that the construction and services sectors were the primary growth engines of Spain's economy at the end of 2025. Manufacturing value added fell 0.3% Q/Q (vs +0.1% prior).

ITALY DATA (MNI): Abrupt Pullback in Manufacturing PMI Momentum Persists

- ITALY JAN MANUF PMI 48.1 (48.5 EXP, 47.9 DEC)

The Italian manufacturing PMI remained in contractionary territory in January, printing below consensus at 48.1 (vs 48.5 cons, 47.9 prior). Note that ISTAT's manufacturing confidence series also remained comfortably below the long-term average in January. According to the PMI, the manufacturing sector has seen a fairly abrupt pullback over the last few months, after hovering around neutral levels in Q3/Q4 2025. That suggests the positive contribution made by industry to Q4 gross value added may only be a temporary dynamic.

SWITZERLAND DATA (MNI): December Retail Sales Overall Solid

- SWISS DEC RETAIL SALES +1.0% M/M, +2.9% Y/Y (VS -0.1% M/M, +1.7% Y/Y NOV)

Today's retail sales data underpin the narrative that the Swiss consumer is in solid shape and, barring new shocks, the SNB is likely to hold its policy rate at 0% for the foreseeable future. The series closed off last year growing in a solid fashion, at 1.0% M/M in December (however that comes after a downwardly revised November, by 0.2pp to -0.1%). Looking at the drivers of the release shows food, beverages and tobacco as well as the "other" category notably strong, while clothing and footwear as

well as auto fuel were on the weaker side (see table below). Over the last couple of months, none of the main subcomponents have exhibited a clear directional trend on a M/M basis.

CHINA DATA (MNI): China Jan Manufacturing PMI Falls Below 50

MNI (Beijing) China's Manufacturing Purchasing Managers Index dropped by 0.8 points to 49.3 in January from December, falling below the breakeven 50 mark, mainly due to traditional off-season and insufficient demand, data from the National Bureau of Statistics showed on Saturday. The production sub-index declined by 1.1 points to 50.6, remaining in the expansionary zone. But new orders sub-index fell further into the contraction territory, by 1.6 points to 49.2.

CHINA DATA (MNI): Jan RatingDog China Mfg. PMI Rises to 50.3

- CHINA JAN RATINGDOG MANUFACTURING PMI 50.3 VS 50.1 IN DEC

MNI (Beijing) China's RatingDog manufacturing PMI, previously known as the Caixin manufacturing PMI, came in at 50.3 in January, up from December's 50.1, remaining in the expansionary zone above the 50 mark, the publisher said on Monday. The production sub-index rose further as the new orders sub-index expanded for the eighth consecutive month. Notably, new export orders returned to expansion territory after a contraction in December, primarily buoyed by increased demand from Southeast Asia.

RATINGS: Italy Positive at S&P, Finland Downgraded at Scope

Rating reviews of note from after hours on Friday include:

- Fitch affirmed the European Union at AAA; Outlook Stable

- Moody's affirmed Israel at Baa1, outlook changed to Stable from Negative

- S&P affirmed Italy at BBB+; Outlook revised to Positive from Stable

- S&P affirmed the European Stability Mechanism (ESM) at AAA; Outlook Stable

- Scope Ratings downgraded Finland to AA; Outlook Stable

- Scope Ratings affirmed Norway at AAA rating; Outlook Stable

FOREX: DXY Consolidates Recovery as Precious Metals Fragility Remains Focus

- The most recent action for G10 currencies has remained a sideshow to the aggressive moves seen in the precious metals space. Price action this morning saw spot silver extend its decline from last Thursday’s peak to as much as 41%, while gold followed suit in plummeting 20% at its worst point as positional dynamics have exacerbated sentiment.

- Key questions surrounding how Fed Chair appointee Warsh is planning to square a smaller balance sheet with lower rates, and expectations for the government shutdown to resolve this week, are helping the DXY consolidate around 1.7% off last week’s cycle lows.

- This is further dampening the recent enthusiasm for EURUSD, which after spiking to 1.2080 early last week, now finds itself trading in a more stable manner around 1.1850. The latest strengthening of the Euro (particularly against the dollar) has reignited downside inflation concerns amongst more dovish GC members, of interest ahead of this Thursday’s ECB.

- The weaker commodity complex, with oil also down 5%, did weigh on the likes of AUD and NZD to start the week, although both have stabilised across the European morning. Positioning dynamics will also be a consideration for AUD as we approach the RBA decision tomorrow, where surveyed analysts lean towards a 25bp hike.

- Elsewhere, markets pounced on latest remarks from PM Takaichi regarding the yen as we approach the Japanese election, where she stated a weak currency can be a major opportunity for export industries. USDJPY rose to 155.51 recovery highs before the weaker risk sentiment and a walking back of the rhetoric assisted a reversal back below 155.

- ISM Manufacturing will show if Friday's outperformance in the MNI Chicago PMI can be seen across the US. The February Refunding round starts today with the Treasury’s update on financing requirements; the full refunding will follow Wednesday.

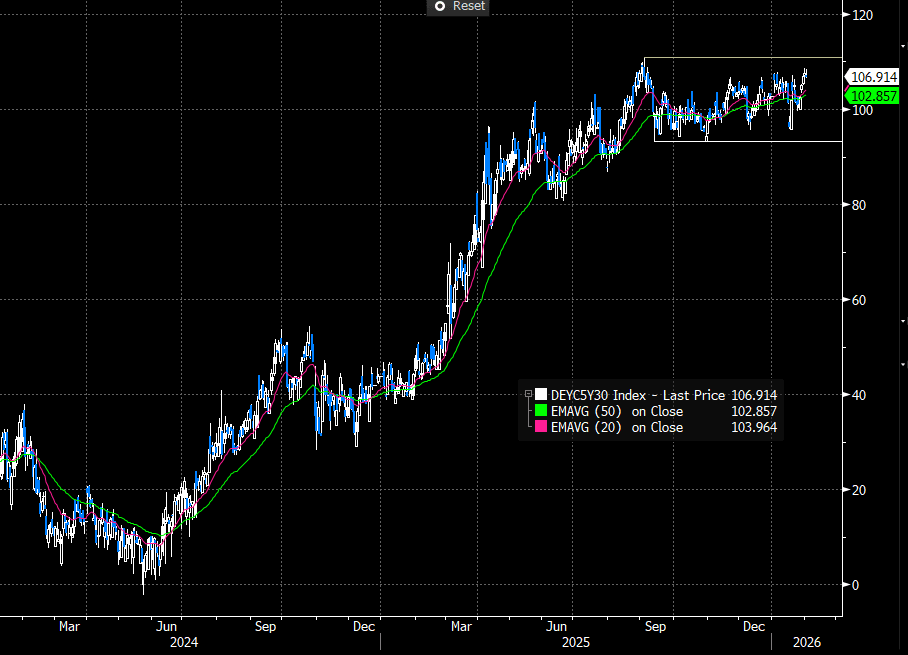

EGBS: Bund Futures Pare Early Gains, Trend Outlook Still Bearish For Now

- Bund futures are now -2 ticks at 128.15, off session highs of 128.38 as global equity benchmarks and precious metals rebound. Last Thursday’s 128.40 high hasn't been tested today. The trend outlook in Bund futures remains bearish - for now - and recent gains are considered corrective. Key short-term resistance to watch is 128.58, the Jan 19 high.

- German yields are up to 1bps higher, with a light bear flattening bias noted. The 5s30s curve is down 0.5bps to 107bps. While the spread has been rangebound between ~93bps and ~111bps since September 2025, a modest steepening trend remains intact. Further evidence supporting Germany’s ongoing fiscal expansion should keep this trend in place in the medium term.

- The 10-year BTP/Bund spread has widened 1.5bps to 63bps, despite the impressive intraday rebound for European equity futures and an S&P outlook tweak to Positive on Friday.

- This week’s regional focus is on the January flash inflation round (Eurozone wide reading on Wednesday) and Thursday’s ECB decision.

Figure 2: German 5s30s Since 2024

Source: Bloomberg Finance L.P

GILTS: Off Highs as Risk Stabilises & PMI Marked Higher, Curve Flatter

Stabilisation in wider risk sentiment (equity index futures and precious metals off lows) and the modest upward revision in the final UK manufacturing PMI have helped gilts away from session highs after risk-off Asia-Pac trade drove a rally at the open.

- Futures ultimately stick within the range established over the prior couple of sessions, last +23 at 91.08 after topping out at 91.21.

- Initial support and resistance located at the Jan 29 low (90.48) and 20-day EMA (91.43), respectively, bearish technical cycle intact.

- Yields little changed to 1-2bp lower, curve flatter. 10s still failing to move definitively away from 4.50%.

- GBP STIRs back from dovish session extremes, SONIA last flat to +2.5, BoE-dated OIS pricing ~38.5bp of cuts through November (~0.5bp more dovish on the day).

- Thursday’s BoE decision is set to headline this week.

- There will be focus on the vote (which from the early previews we have read is expected to be 7-2 with risks of 6-3) but the main focus is likely to be twofold: firstly on the Agents' Annual Pay Survey which will be announced alongside the decision and which the MPC have already been privy to and will be used as a guide for how sticky wage inflation is expected to be through 2026.

- Secondly, the individual member paragraphs will be watched - particularly Governor Bailey, Breeden and Ramsden (assuming neither of the latter two vote for a sequential cut). Any hints guiding towards a March cut will be key here.

- On the supply front, the DMO will come to market with GBP4.25bln of the 4.75% Oct-35 line tomorrow.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Feb-26 | 3.730 | +0.5 |

Mar-26 | 3.678 | -4.7 |

Apr-26 | 3.546 | -17.9 |

Jun-26 | 3.490 | -23.5 |

Jul-26 | 3.411 | -31.3 |

Sep-26 | 3.379 | -34.5 |

Nov-26 | 3.342 | -38.3 |

Dec-26 | 3.347 | -37.8 |

EQUITIES: Short-Term Weakness for Eurostoxx 50 Futures Considered Corrective

A bull cycle in Eurostoxx 50 futures remains intact and S/T weakness is - for now - considered corrective. The next important support to monitor lies at the 50-day EMA at 5851.01. A clear breach of this average would signal scope for a deeper retracement. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. A resumption of gains would open the key resistance and bull trigger at 6072.00, the Jan 14 / 15 high. The trend in S&P E-Minis is bullish and the pullback from last week’s high is considered corrective. However, note that a doji candle pattern on Jan 28 and a hammer candle on Jan 29, continues to signal scope for a deeper retracement near-term. Today’s move down reinforces the importance of these two patterns. A continuation lower would expose key S/T support at 6814.50, the Jan 21 low. The bull trigger is at 7043.00, the Jan 28 high.

- Japan's NIKKEI closed lower by 667.67 pts or -1.25% at 52655.18 and the TOPIX ended 30.19 pts lower or -0.85% at 3536.13.

- Elsewhere, in China the SHANGHAI closed lower by 102.202 pts or -2.48% at 4015.746 and the HANG SENG ended 611.54 pts lower or -2.23% at 26775.57.

- Across Europe, Germany's DAX trades higher by 33 pts or +0.13% at 24573.19, FTSE 100 lower by 6.95 pts or -0.07% at 10216.39, CAC 40 up 2.39 pts or +0.03% at 8128.92 and Euro Stoxx 50 down 13.2 pts or -0.22% at 5934.61.

- Dow Jones mini down 138 pts or -0.28% at 48870, S&P 500 mini down 39 pts or -0.56% at 6926.75, NASDAQ mini down 216 pts or -0.84% at 25454.

Time: 10:00 GMT (05:00 ET)

COMMODITIES: Gold Continues to Unwind Extreme Overbought Condition

A bull cycle in WTI futures remains intact. However, today’s strong bearish start to this week’s session highlights the beginning of a corrective phase. Attention is on support at the 20-day EMA, at $60.89. The 50-day EMA lies at $59.64. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high. A sharp sell-off in Gold confirms a top in the long-term trend - for now - and from a short-term perspective, marks an unwinding of the recent extreme overbought condition. The metal has traded through the 20-day EMA, and has pierced the 50-day EMA, at $4546.7. A break of this average would signal scope for a deeper retracement and open $4274.7, the Dec 31 ‘25 low. Initial firm resistance is at 4885.1, today’s intraday high so far.

- WTI Crude down $3.18 or -4.88% at $62.02

- Natural Gas down $0.68 or -15.66% at $3.667

- Gold spot down $177.02 or -3.62% at $4720.75

- Copper down $10.35 or -1.75% at $581.55

- Silver down $3.33 or -3.91% at $82.0401

- Platinum down $119.66 or -5.45% at $2077.58

Time: 10:00 GMT (05:00 ET)

| Date | GMT/Local | Impact | Country | Event |

| 02/02/2026 | 1145/1145 | BOE Breeden on Payments | ||

| 02/02/2026 | 1445/0945 | *** | S&P Global Manufacturing Index (f) | |

| 02/02/2026 | 1500/1000 | *** | ISM Manufacturing Index | |

| 02/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/02/2026 | 1730/1230 | Atlanta Fed's Raphael Bostic | ||

| 03/02/2026 | 0030/1130 | * | Building Approvals | |

| 03/02/2026 | 0330/1430 | *** | RBA Rate Decision | |

| 03/02/2026 | 0700/0200 | * | Turkey CPI | |

| 03/02/2026 | 0745/0845 | *** | HICP (p) | |

| 03/02/2026 | 0745/0845 | Budget Balance | ||

| 03/02/2026 | 0900/1000 | ** | ECB Bank Lending Survey | |

| 03/02/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 03/02/2026 | 1300/0800 | Richmond Fed's Tom Barkin | ||

| 03/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 03/02/2026 | 1500/1000 | *** | JOLTS Jobs Opening Level | |

| 04/02/2026 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 04/02/2026 | 2200/0900 | ** | S&P Global Final Australia Composite PMI |