MNI US OPEN - Expect Greater Sensitivity to a Soft NFP Print

EXECUTIVE SUMMARY

- MNI US PAYROLLS PREVIEW: A TEST OF TWO CUTS EYED FOR 2025

- JAPAN, US START TARIFF TALKS AMID REPORTS ON CARS, RARE EARTHS

- TRUMP AND CARNEY IN TALKS ON TRADE AHEAD OF G-7 SUMMIT

- RBI SURPRISES MARKETS WITH LARGER-THAN-EXPECTED 50BP CUT

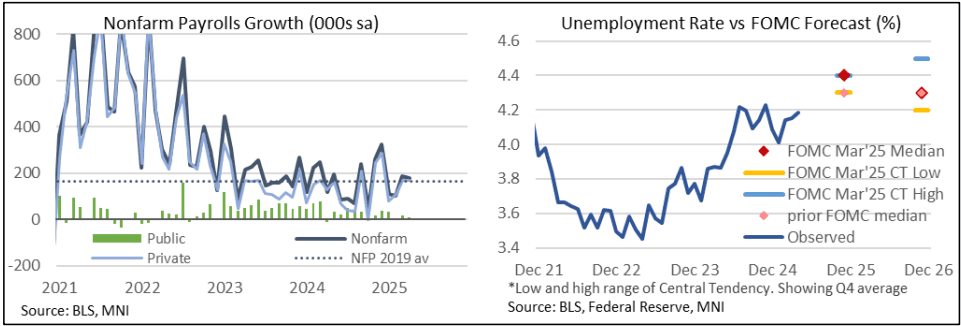

Figure 1: Recent US labour market developments

NEWS

MNI US PAYROLLS PREVIEW: A Test of Two Cuts Eyed for 2025

Nonfarm payrolls are seen increasing a seasonally adjusted 126k in May in the Bloomberg survey after a stronger than expected 177k in April (albeit one that was more than offset by negative revisions). Primary dealer analysts also see 125k whilst the Bloomberg whisper is weaker again, currently at 119k after Wednesday’s weak ADP release continued a clearly moderating trend. More analysts than not expect limited impact from the weather but that’s not a unanimous view. The industry breakdown will be watched for any weakness in trade & transportation after a strong April - likely on rapid inventory builds on tariff front-running - plus broader implications for discretionary demand.

US/JAPAN (BBG): Japan, US Start Tariff Talks Amid Reports on Cars, Rare Earths

Japan and the US have begun the latest round of trade negotiations, with media reports suggesting Tokyo’s delegation is trying to win a reprieve from the tariffs by pledging to make more cars in the US and enhancing cooperation on rare earths. Japan’s top trade negotiator Ryosei Akazawa met with US Commerce Secretary Howard Lutnick on Thursday in Washington, exchanging specifics on non-tariff barriers, expanding trade and cooperating on economic security, Japan’s cabinet secretariat said in a release. Akazawa is expected to return to Japan Sunday after finishing what could be the last round of cabinet level discussions before Group of Seven leaders convene for a summit in Canada later this month.

US/CANADA (BBG): Trump and Carney in Talks on Trade Ahead of G-7 Summit

US President Donald Trump and Canadian Prime Minister Mark Carney have been in direct contact trying to reach a trade deal, but the two sides still have work to do to find agreement, according to people familiar with the discussions. Trump is planning to attend the Group of Seven leaders’ summit in Canada that begins June 15, and some Canadian officials hope to reach a deal to lower or eliminate tariffs before then. The US has punishing import taxes in place on Canadian-made steel, aluminum and autos, and Canada has imposed retaliatory tariffs on a range of American-made goods.

US/CHINA (MNI): U.S. Firms in China Not Planning Home Production

MNI (Beijing) The majority of U.S. firms operating in China are focused on localising operations or shifting some production to third countries rather than exiting the country, a recent flash survey of 112 firms by the American Chamber of Commerce in China published on Friday showed, with zero respondents reporting plans to shift output back to the US. The potential impact of rare-earth export restrictions was severe, with 75% of effected members stating stocks would run out within three months. However, the chamber cautioned that although rare earths attracted significant news and policymaker attention, they only affected a niche group of respondents.

US/S.KOREA (BBG): South Korea to Keep Discussing Forex With US After Currency List

South Korea will continue to discuss its foreign exchange policy with the US to promote mutual understanding, after the Treasury kept the Asian ally on its watchlist and called for curbing currency intervention. The Treasury Department, in a semiannual foreign-exchange report released Thursday, didn’t label any country a currency manipulator but kept South Korea on its monitoring list for currency practices alongside China and Japan, among other countries. South Korea’s finance ministry issued a statement Friday saying it will seek to foster “mutual understanding and trust” over exchange rate policy through regular communication and ongoing currency talks with the US.

US (POLITICO): Trump, White House Aides Signal a Possible Détente With Musk

Signs of a truce are emerging in the increasingly bitter clash between two of the world’s most powerful men. President Donald Trump projected an air of nonchalance in an interview Thursday with POLITICO during a day of sparring over social media with Elon Musk. Separately, White House aides, after working to persuade the president to temper his public criticism of Musk to avoid escalation, scheduled a call Friday with the billionaire CEO of Tesla to broker a peace.

CANADA/CHINA (BBG): Carney, Li Hold Talks on Fentanyl, Trade in Sign of Warming Ties

Canadian Prime Minister Mark Carney spoke with Chinese Premier Li Qiang on Thursday in a sign that the tense relationship between the two nations might be improving. The two covered a range of topics including trade, fentanyl and efforts to make communication between the two countries more regular, the Canadian government said in a statement. Canada brought up trade concerns that are impacting agricultural exports, particularly canola and seafood. The call came after the trade ministers from both countries met in Paris this week, with Chinese Commerce Minister Wang Wentao saying they should work to get economic and trade relations back on track.

ECB (BBG): ECB Should Take Timeout With Cuts ‘Nearly Done,’ Stournaras Says

The European Central Bank should take a break from lowering interest rates to give officials a chance to assess recent shocks, particularly from trade, according to Governing Council member Yannis Stournaras. “Now the best thing is wait and see,” the Greek central-bank chief told Bloomberg Television. “It’s nearly done but with such uncertainty worldwide you can never say it’s done.” The comments echo President Christine Lagarde on Thursday after the ECB reduced its deposit rate for an eighth time, to 2%. That move left policymakers “in a good position to navigate the uncertain conditions that will be coming up,” she said.

RUSSIA/UKRAINE (NYT): Russia Launches Broad Assault on Kyiv and Other Cities in Ukraine

Explosions rocked Kyiv, the Ukrainian capital, before dawn on Friday as air defense crews raced to combat a large-scale Russian bombardment, the authorities said. The Ukrainian Air Force reported that Russia had begun launching ballistic missiles, cruise missiles and drones at the capital and other cities overnight. Multiple fires were reported across Kyiv, including at a 16-story apartment block. Mayor Vitali Klitschko said at least three people had been injured, and officials cautioned that the toll could rise as the attack was still underway.

SNB (MNI): Unlikely to Be Deterred From FX Tools Despite US Monitoring

Late yesterday, the US Treasury placed Switzerland on the US currency manipulator "monitoring list" and this morning's SNB reaction statement raises questions on any impact for near-term SNB policy. The Trump administration labelled Switzerland a currency manipulator already in 2020 - to which the SNB back than mentioned that their "monetary policy approach remains unchanged". Our view is that barring major retaliation from the US, which appears to not be on the table for now, the SNB would not want to let slip one of their two monetary policy tools.

UK (FT): Labour Wins Pivotal Scottish By-Election Over SNP and Reform

Scottish Labour defied predictions to defeat the ruling Scottish National party in a key Scottish by-election where Reform UK finished in third place. Davy Russell took the Hamilton, Larkhall and Stonehouse seat for Labour with 8,559 votes, beating the SNP’s Katy Loudon by 602 votes on a turnout of 44 per cent. Labour secured a vote share of 31.6 per cent, with the SNP on 29.4 per cent and Reform on 26.1 per cent. The Conservatives were down at 6 per cent. The contest comes less than a year before the next elections to the Scottish parliament, when the SNP will seek to extend what will by then be a 19-year stay in power.

GERMANY (MNI): Merz Says Trump Admin 'Open to Discussions' on Tariffs, Security & NATO

Reuters reports comments from Chancellor Freidrich Merz following his talks on 5 June with US President Donald Trump. Merz says that the Trump administration "is open to discussions" and to hearing other opinions. The chancellor confirms he and Trump discussed the war in Ukraine, tariff policies, and the future of NATO. Merz: "Trump was clear about not taking the US out of NATO, I have no doubts the US will stick with NATO."

ITALY (MNI): Referendums Likely to Fail on Low Turnout

Voters go to the polls on Sunday, 8 and Monday, 9 June to vote in five 'abrogative' referendums. PM Giorgia Meloni's coalition gov't opposes the measures, and they are unlikely to pass. Their unexpected success would come as a blow to the government's prestige, but would not cause any lasting damage to the coalition's stability. As EurActiv reports, "Four of the five questions focus on labour law, ranging from reinstating unfairly dismissed workers and removing compensation caps in small firms, to curbing fixed-term contract abuse and restoring joint liability for workplace injuries. The fifth and most prominent referendum proposes reducing the residency requirement for non-EU citizens applying for Italian citizenship from 10 to five years."

EU/RUSSIA (FT): EU Weighs Adding Russia to Money Laundering ‘Grey’ List

The EU is weighing whether to add Russia to its “grey list” of countries with lax money laundering controls, as Brussels’ lawmakers aim to increase financial pressure on Moscow. European Commission officials said they were considering adding Russia, a move that a majority of members of the European parliament have been advocating. But no decision has been taken, officials stressed.

CHINA (BBG): PBOC Eases Liquidity Jitters With Surprise Cash Disclosure

China’s central bank added 1 trillion yuan ($139 billion) of three-month funds into markets on Friday, following a surprise mid-month disclosure for the operation likely aimed at preempting a seasonal cash crunch. The People’s Bank of China made the cash injection via so-called outright reverse repurchase agreements, effectively short-term loans to banks, after announcing the move late Thursday. The disclosure broke the pattern of revealing details of the operation only at the end of a month since the PBOC unveiled the additional monetary policy tool in October.

RBI (MNI): RBI Surprises Markets With Larger-Than-Expected 50bp Cut

The RBI surprised markets with a 50bps cuts on the back of ongoing softness in inflation, describing the fall as 'significant'. Given the outlook for monsoon season the RBI described the outlook for Core inflation as 'benign' and projects FY 2026 inflation at 3.7% (April CPI 3.16%). The RBI governor suggested that the growth / inflation dynamic called for front loading of cuts and puts monetary policy stance to neutral, suggesting that future cuts should not be expected. The RBI Governor described the global backdrop as fragile and highly fluid and that this last period of downward pressure on prices (CPI) being protracted.

IRAN/CHINA (WSJ): Iran Orders Material From China for Hundreds of Ballistic Missiles

Iran has ordered thousands of tons of ballistic-missile ingredients from China, people familiar with the transaction said, seeking to rebuild its military prowess as it discusses the future of its nuclear program with the U.S. Shipments of ammonium perchlorate are expected to reach Iran in coming months and could fuel hundreds of ballistic missiles, the people said. Some of the material would likely be sent to militias in the region aligned with Iran, including Houthis in Yemen, one of the people said.

DATA

EUROZONE DATA (MNI): Q1 GDP Upwardly Revised to Joint Highest Since Q2'22

- EUROZONE Q1 GDP +0.6% Q/Q, +1.5% Y/Y

Eurostat upwardly revised Q1 GDP according to their third estimate of the data, to +0.6% Q/Q (cons 0.4) following 0.3% in the previous estimate and 0.3% in Q4. That is the joint highest sequential pace seen since Q2 2022. On a Y/Y basis, growth was 1.5% (upwardly revised from 1.2%). The stronger figures follow ECB President Lagarde saying at yesterday's press conference she would "not be surprised" about an upward revision to Q1 growth. Despite the strong performance last quarter, the ECB yesterday saw 2025 overall growth unchanged from their last projection, at 0.9% overall.

EUROZONE APR RETAIL SALES +0.1% M/M, +2.3% Y/Y (MNI)

FRANCE DATA (MNI): Trend in Industrial Production Remains Weak

- FRANCE APR INDUSTRIAL PRODUCTION -1.4% M/M, -2.1% Y/Y

- FRANCE APR MANUFACTURING OUTPUT -0.6% M/M, -1.6% Y/Y

The trend in French industrial production remains weak. In April, headline IP fell 1.4% M/M (vs +0.1% prior), while manufacturing IP also fell 0.6% M/M (vs 0.5% prior). Surveys present a mixed picture ahead. The manufacturing PMI almost reached the neutral 50 handle in May (49.8 vs 48.7 prior), but INSEE's industrial confidence series dipped to 96.9 from 99.8. Looking across major sub-components, intermediate goods production remains extremely sluggish, and has fallen in five of the last six months. Durable consumer goods saw a 1.4% M/M rise in April (vs -2.8% prior), but the 3m/3m rate remains weak at 0.3%.

ITALY DATA (MNI): ISTAT Revises 2025 GDP Projection Lower as Trade and Consumption Drag

ISTAT has revised its 2025 domestic GDP projection down to 0.6% from 0.8% in the December forecast round. This is in line with domestic media reports back in April. Given the impressive BTP/Bund tightening observed in recent weeks, it's important to keep Italian macroeconomic expectations and outturns in mind. A weaker GDP outlook would make it harder for the Government to achieve its 3.3% 2025 budget deficit projection, all else equal.

JAPAN DATA (MNI): Real Household Spending Back Negative in April, Below Forecasts

- JAPAN APRIL HOUSEHOLD SPENDING -0.1% Y/Y; MARCH +2.1%

- JAPAN APRIL HOUSEHOLD SPENDING -1.8% M/M; MARCH +0.4%

Japan April household spending was notably weaker than forecast, printing 0.1%y/y in real terms, versus a +1.5% consensus forecast (the March outcome was +2.1%y/y). Note spending was down 1.8%m/m. This outcome continues the recent see-saw y/y pattern for real spending. as we oscillate around flat (the Dec/Jan period we saw back to back positive gains). This print comes after yesterday's April labor earnings data, which showed headline outcomes slightly weaker than forecast. We did see scheduled pay (on a same base period) improve further but real earnings remain entrenched in negative territory.

RATINGS: Array of Updates Due After Hours, Mix of Outlooks

Potential sovereign rating reviews of note scheduled for after hours on Friday include:

- Fitch on Austria (current rating: AA+; Outlook Negative), Estonia (current rating: A+; Outlook Stable) & Hungary (current rating: BBB; Outlook Stable)

- Moody’s on Norway (current rating: Aaa, Outlook Stable) & South Africa (current rating: Ba2, Outlook Stable)

- S&P on Malta (current rating: A-; Outlook Stable) & Slovenia (current rating: AA-; Outlook Positive)

- Morningstar DBRS on Austria (current rating: AAA, Stable Trend) & Estonia (current rating: AA (low), Stable Trend)

Please use this link to access the indicative sovereign rating review schedule covering the five most notable rating agencies for 2025. Note that this schedule is indicative only and ratings can be reviewed on an ad-hoc basis. Rating agencies may also adjust their schedules during the year.

FOREX: USD Off Lows, Shrugs Off Political Tumult

- After a tumultuous Thursday close, the greenback is recovering off lows, firming against all others in G10 ahead of the May jobs report. This has helped drag EUR/USD further off the post-ECB high at 1.1495, but losses at present are not sufficient to counter the underlying uptrend as defined by the 50-dma, which today highs 1.1259 - the highest since Q1 2022.

- Meanwhile, the recovery in equities overnight (e-mini S&P is higher by 0.4% at pixel time) is working further against the JPY, which keeps USD/JPY north of Y144.00 and EUR/JPY on track for a test of mid-May highs at Y165.21. The shape of the JGB yield curve remains a key driver here, with markets increasingly of the view that the finance ministry will tweak bond sale plans as soon as next month in order to compensate for stretched longer-end of the curve, and take advantage of the greater relative demand for shorter-dated securities.

- The recovering USD and stronger EUR post-ECB is putting GBP/USD on the backfoot. Moves look corrective at these levels, particularly as markets looked through the over-estimation of April UK CPI and the more dovish overtones from BoE Deputy Governor Breeden earlier in the week. As such, the technical picture remains bullish GBP/USD. Thursday’s climb resulted in a fresh cycle high, confirming a resumption of the uptrend and an extension of the price sequence of higher highs and higher lows.

- Markets expect job gains of 126k over the month and the industry breakdown will be watched for any weakness in trade & transportation after a strong April - likely on rapid inventory builds on tariff front-running - plus broader implications for discretionary demand. We expect greater sensitivity to a soft print in the event of a large surprise, although longer-term reaction would likely be capped by the FOMC not wanting a repeat of September’s (with hindsight) overreaction to a sharp but short-lived uplift in the u/e rate.

EGBS: Bunds Retrace Half of Yesterday's Selloff; BTP Tightening Persists

The German curve has bull flattened, with Schatz yields down 2bps and 10/30-year Bund yields down 4bps. That sees the 2s10s curve unwind the bear steepening seen following yesterday’s ECB decision and Trump/Xi phone call headlines (2s10s is 1.5bps flatter at 69bps).

- Weak French and German industrial production data will have lent support to EGBs this morning, but the rally started in earnest just ahead of the cash equity open. The US NFP print at 1330BST remains the primary focus for global markets today.

- Eurozone Q1 GDP was revised up to 0.6% (vs 0.3% second release), while compensation per employee at 3.8% Y/Y was above the ECB’s June projection. However, the market reaction was limited.

- Bund futures are +51 ticks at 130.70, retracing almost half of yesterday afternoon’s selloff. A bullish theme in Bund futures remains intact and yesterday’s pullback is - for now - considered corrective.

- 10-year EGB spreads to Bunds are biased a little wider with the exception of BTPs (and GGBs), where tightening momentum remains at the fore. The spread is 0.5bps narrower at 94bps at typing.

- ISTAT has revised its 2025 domestic GDP projection down to 0.6% from 0.8% in the December forecast round. This is in line with domestic media reports back in April. Given the impressive BTP/Bund tightening observed in recent weeks, it's important to keep Italian macroeconomic expectations and outturns in mind.

- There have been a host of ECB speakers today, most doing little to move markets. Holzmann confirmed that he dissented at yesterday’s decision – an unsurprising development.

GILTS: Early Uptick Holds, Curve Flatter

Gilts hold the early uptick after looking to a rally in EGBs.

- Soft German industrial production data and some seemingly dovish ECB speak was noted ahead of the open, although that would usually promote bull steepening of EGB curves.

- Market may still be heavily positioned in steepeners (similar to gilts), potentially helping explain the EGB curve bias.

- Gilt futures see a much more modest reaction than Bunds.

- Futures as high as 92.36 today after the bullish cycle extended yesterday.

- Initial resistance located at yesterday’s high (92.63), which protects a Fibonacci level (92.79).

- Yields 0.5-3.5bp lower, curve flatter.

- 5s30s trades further below 120bp.

- 2s10s back below 60bp, that curve has failed to push decisively below that level in recent days.

- 10-Year yields remain within the wedge we have outlined in recent weeks, defined by the short-term downtrend drawn off the year-to-date highs and the longer run uptrend drawn off the Dec ’21 lows. Benchmark hovering around 4.60%.

- 10s ~2bp wider vs. Bunds around 205bp, recent run of narrowing has failed to generate a break back below 200bp.

- BoE-dated OIS shows 41bp of cuts through year-end vs. ~40bp early today, SONIA futures flat to +4.0.

- Little of note on the UK calendar ahead of the weekend, which will leave focus on macro drivers, most notably in the form of the U.S. NFP release.

EQUITIES: Fresh Cycle Highs Bolster Bullish E-Mini S&P Trend Conditions

The trend cycle in Eurostoxx 50 futures remains bullish and a recent pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen a bull theme. Key support to watch lies at 5274.35, the 50-day EMA. A clear break of this average would signal a possible reversal. The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract traded to a fresh cycle high yesterday. The recent break of 5993.50 last week, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. A continuation would open 6057.00 next, the Mar 3 high. Key support lies at 5780.89, the 50-day EMA.

- Japan's NIKKEI closed higher by 187.12 pts or +0.5% at 37741.61 and the TOPIX ended 12.86 pts higher or +0.47% at 2769.33.

- Elsewhere, in China the SHANGHAI closed higher by 1.26 pts or +0.04% at 3385.358 and the HANG SENG ended 114.43 pts lower or -0.48% at 23792.54.

- Across Europe, Germany's DAX trades lower by 56.16 pts or -0.23% at 24268.49, FTSE 100 higher by 2.61 pts or +0.03% at 8813.63, CAC 40 down 10.64 pts or -0.14% at 7779.63 and Euro Stoxx 50 down 6.28 pts or -0.12% at 5404.27.

- Dow Jones mini up 146 pts or +0.34% at 42515, S&P 500 mini up 22 pts or +0.37% at 5968, NASDAQ mini up 71.5 pts or +0.33% at 21653.75.

Time: 09:50 BST

COMMODITIES: WTI Futures Still Close to Recent Highs But Bear Threat Present

WTI futures continue to trade closer to their recent highs. A bear threat remains present and the recovery since Apr 9 still appears corrective. A key resistance area to monitor is $62.56, the 50-day EMA. It has been pierced, however, a clear break of it would highlight a stronger reversal and open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. A bullish theme in Gold remains intact. Medium-term trend signals are bullish - moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Sights are on $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, key support and the bear trigger to watch has been defined at $3121.0, the May 15 low. First support lies at 3313.2, the May 5 low.

- WTI Crude down $0.29 or -0.46% at $63.09

- Natural Gas up $0.04 or +1.12% at $3.719

- Gold spot up $13.78 or +0.41% at $3366.29

- Copper down $5.65 or -1.15% at $487.8

- Silver up $0.56 or +1.58% at $36.212

- Platinum up $23.28 or +2.04% at $1163.58

Time: 09:50 BST

| Date | GMT/Local | Impact | Country | Event |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1230/0830 | *** | Employment Report | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1900/1500 | * | Consumer Credit | |

| 07/06/2025 | 0730/0930 | ECB's Lagarde Speech In Monaco | ||

| 07/06/2025 | 0940/1140 | ECB's Schnabel in Dubrovnik panel discussion | ||

| 07/06/2025 | 0940/1040 | BOE Greene On Central Bank Decoupling Panel |