MNI US OPEN - ECB Expected to Creep Closer to Neutral

EXECUTIVE SUMMARY:

- ECB EXPECTED TO CUT RATES BY A FURTHER 25BPS, LANGUAGE IN FOCUS

- RISKS TO FED'S MANDATE "ON THE UPSWING" - SCHMID

- US, JAPAN TO BEGIN FORMAL TARIFF TALKS WITHOUT DISCUSSING FX

- NVIDIA CEO VISITS BEIJING

- JAPAN DROPS PLANS FOR TARIFF-RELATED CASH HANDOUT

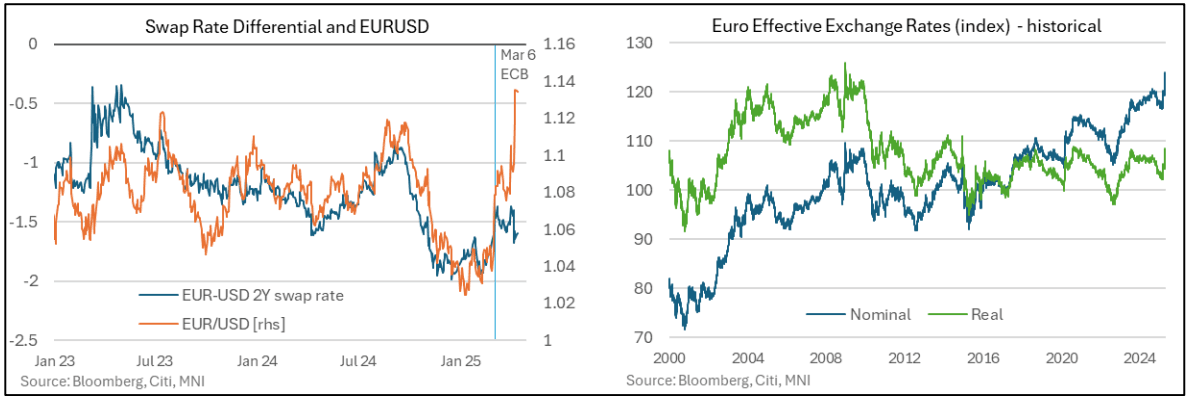

Figure 1: Currency in focus for ECB; EUR strength stands out despite dovish central bank

NEWS:

FED (MNI): Risks To Fed's Mandates 'On The Upswing' - Schmid

Federal Reserve Bank of Kansas City President Jeff Schmid said Wednesday the risks of veering away from full employment and price stability are "on the upswing," though the U.S. economy is starting from a good position.

US/CHINA (WSJ): U.S. Tries to Crush China’s AI Ambitions With Chips Crackdown

New chip restrictions for Nvidia and AMD show the Trump administration’s determination to battle China on tech advances as well as trade.

US/JAPAN (BBG): US, Japan Begin Formal Tariff Talks Without Discussing Forex

The US and Japan kicked off tariff negotiations with an aim to reach a deal as soon as possible but did not discuss currency issues, Japan’s top negotiator Ryosei Akazawa said. The talks did not result in an immediate halt on the tariffs, but preparations are underway for the second round of talks to take place later this month, Akazawa said in Washington Wednesday.

US/UK (The Times): Keir Starmer risks stand-off with Trump over EU carbon levies

Sir Keir Starmer is offering to align with EU carbon levies as part of a wider reset with Brussels, threatening to drag the UK into a trade stand-off with President Trump. The prime minister will host an EU-UK summit on May 19 in London as he seeks to ease trade barriers with Brussels. He is proposing deeper co-operation with Brussels on the EU carbon border adjustment mechanism (CBAM), a way of calculating taxes on high-polluting industries.

CORPORATE (BBG): Nvidia CEO Visits Beijing After US Bars AI Chip Sales to China

Nvidia Corp. Chief Executive Officer Jensen Huang arrived in Beijing Thursday, shortly after the Trump administration barred the company from selling H20 AI chip to China. Huang, a frequent visitor to the country, flew to Beijing at the invitation of the China Council for the Promotion of International Trade, according to a post by Yuyuantantian, a social media account affiliated with state-run China Central Television.

JAPAN (Mainichi): Japan Govt. Drops Plan for Tariff Cash Handouts

The government and the ruling parties have made arrangements to postpone the implementation of the proposal for a flat cash transfer of 30,000 ~ 50,000 yen for the entire population, which was being considered as a measure against high tariffs and high prices.

CHINA (MNI): Expectations For China Stimulus To Underpin Steel Futures

Chinese analysts give their view on the outlook for steel prices - On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (MNI): April LPR To Hold As Tariff Impact Contained

China's Loan Prime Rate is likely to remain unchanged in April after strong first-quarter economic data and as official support for capital markets has succeeded in lowering volatility amid tariff tensions.

RBNZ (MNI): RBNZ OCR Below 1% Possible On Trade Woes

On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (MNI): BOJ Ueda, Uncertainties Linked to Tariffs Surge

Bank of Japan Governor Ueda warned on Thursday that uncertainties linked to U.S. tariffs have increased sharply and the bank will assess their impact on the economy and prices without preconditions, and conduct policy appropriately.

SOUTH KOREA (MNI): Governor Flags Cut, But Timing Unclear

Bank of Korea Governor Rhee Chang-yong on Thursday signalled an upcoming rate cut on the back of downside risks to economic growth and elevated levels of global uncertainty but offered no guidance as to its likely timing or size.

ECB: MNI ECB Preview: Neutral Beckons But Markets Firmly Dovish

- We have published and e-mailed to subscribers the MNI ECB Preview, including MNI analysis plus analyst views on what to expect at this month's meeting.

- Please find the full report here: https://media.marketnews.com/ECB_Preview_Apr2025_443aa6f923.pdf

TURKEY: MNI CBRT Preview - Easing Cycle Hits Major Roadblock

- Following the bank’s unscheduled overnight lending rate hike in late March, the CBRT’s easing cycle has hit a significant roadblock, and cuts to the one-week repo rate are unlikely in the very near-term.

- This confirms financial stability as the policy preference over slowing headline CPI.

- The vast majority of analysts surveyed see no change in policy at this month’s meeting, although a not insignificant minority see a real risk of policy tightening this week. Full preview here: Download Report Here

DATA:

**MNI:AUSTRALIA MAR UNEMPLOYMENT RATE +4.1%

AUSTRALIA MAR LABOR PARTICIPATION RATE +66.8%

AUSTRALIA MAR F-T EMPLOYED PERSONS CHANGE 15K

AUSTRALIA MAR EMPLOYED PERSONS CHANGE 32.2K

EGBS: German Curve Bear Flattens Ahead of ECB Decision

The German curve has bear flattened, with Schatz yields up 4.5bps to 1.79% and 30-year Bund yields up 1bp to 2.92%. Hawkish repricing in front-end EUR rates ahead of this afternoon’s ECB decision has driven the weakness in Schatz, which likely represents pre-decision positioning rather than a reassessment of Eurozone fundamentals. Meaningful headline flow has been relatively light.

- A 25bp cut is firmly expected from the ECB at 1315BST/1415CET, with more focus on whether wording tweaks will be made in the policy statement, and President Lagarde's description of balance of the balance of risks to inflation and growth in light of the German fiscal announcement and US reciprocal tariffs.

- Bund futures are -24 ticks at 131.02, with morning volumes relatively subdued. Initial support is 130.75 (Apr 15 low), which shields the 20-day EMA at 129.97. Resistance is seen at 131.57 (Apr 15 high).

- Today’s MT OAT auction was decent, with the top of the E10-12bln range sold and healthy bid-to-covers across lines. IL OAT supply is due at 1050BST.

- 10-year EGB spreads to Bunds are within 1bp of yesterday’s close, with European equity futures retracing late-Wednesday weakness overnight.

GILTS: Off Lows, Macro Cues Eyed

Gilts reverse their early downtick with equities and oil off session highs.

- Little of note when it comes to UK-specific news flow, leaving cross-market cues at the fore.

- Futures traded as low as 91.73 before recovering towards 92.00 shortly after the open, holding a narrow range in the time since.

- Initial support and resistance defined at the April 15 low (91.43) and the April 16 high (92.32), with recent gains still deemed corrective at this stage.

- Yields little changed to 2bp higher, 5s under the most pressure.

- Some light outperformance vs. Bunds leaves the 10-Year spread ~1.5bp tighter on the day at ~208.5bp, ~10bp below last week’s highs.

- BoE-dated OIS little changed to ~2bp less dovish on the day, showing 25bp of easing for next month, 34bp through June, 52bp through August and 78.5bp through year-end. We continue to lean towards the idea of quarterly cuts, with the next coming in May.

- A reminder that ~87.5bp of cuts were briefly priced through year-end following yesterday’s CPI release.

- UK markets will be closed on Friday & Monday, which could limit activity and liquidity today, unless we get some meaningful news flow.

- The major scheduled macro risk event comes in the form of the latest ECB decision. A rate cut is fully discounted, leaving focus on the rhetoric deployed surrounding the stance of interest rates.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

May-25 | 4.205 | -25.3 |

Jun-25 | 4.117 | -34.2 |

Aug-25 | 3.940 | -51.9 |

Sep-25 | 3.843 | -61.5 |

Nov-25 | 3.713 | -74.6 |

Dec-25 | 3.674 | -78.5 |

FOREX: USDJPY Recovers from Cycle Lows, DXY Consolidating ~99.50

- The majority of the focus for G10 currency markets on Thursday has been for the Japanese yen following the initial US-Japan trade talks taking place. The weaker greenback trend had prompted USDJPY to fall to a fresh cycle low overnight at 141.62, however positives emanating from these discussions then appeared to provide a boost to USDJPY.

- The pair now stands roughly 100 pips off the lows, having bounced as high as 143.08 in European trade. Furthermore, US equity futures are holding onto their session gains and combined with the higher US yields, appear to have provided a yen headwind on Thursday. Initial resistance for USDJPY is not seen until 144.64 the Apr 11 high.

- Amid the slightly firmer US dollar, the likes of AUD and NZD are struggling to extend their most recent recoveries. AUDUSD has failed on the approach to 0.6400 once more as a lower-than-expected employment change was countered by the unemployment rate coming in a tenth below expectations. Higher than forecast inflation data in New Zealand prompted a moderate bounce for NZDUSD, however so far, prior highs at 0.5944 have capped the upside.

- In similar vein, EURUSD made another attempt above 1.14 but has since subsided to the 1.1375 area. EURUSD vols are generally contained headed into today's ECB decision, where a 25bps rate cut is broadly expected. Key focus remains on 1.1495, the Feb 10 2022 high.

- Despite the moderate uptick on Thursday, the USD index has fallen sharply in recent weeks as a rotation out of US assets seems to be gathering momentum and normal correlations with yields have broken down. Positioning dynamics will be closely monitored as we approach the long holiday weekend.

FOREX: Progress with Japan Pressures JPY, While EUR Vols Look Contained into ECB

- EUR/USD vols are generally contained headed into today's ECB decision - overnight implied opened at 15 points, well below recent highs - although infitting with the April theme of higher underlying levels of volatility (month-to-date average overnight implied is ~14.8 points vs. Q1's ~8.5 points). A 25bps rate cut is broadly expected - with market focus on language and where the ECB consider rates within their view of neutral monpol.

- JPY weakness is evident across G10, with Trump noting the "big progress" made with Japan in trade talks helping inject some risk. As a result, EUR/JPY is through yesterday's highs and correlating well with US stock futures. USD/JPY now trades within close proximity to a larger options strike rolling off today at Y142.80-00, amounting to $1.1bln notional.

- The USD Index remains below 100.00 having found some support ahead of a test on the 99.014 low having de-linked with the recovery in equities as well as the base in front-end yields, as well as the slope of the US curve - leaving the USD lagging cross-markets.

EQUITIES: Eurostoxx Futures Hold Above Recent Lows

A reversal higher in S&P E-Minis on Apr 9 highlights the start of a corrective cycle. The trend condition has been oversold following recent weakness and the move higher is allowing this set-up to unwind. Initial resistance to watch is 5479.72, the 20-day EMA. Eurostoxx 50 futures continue to trade above their recent lows. The latest bounce highlights a corrective cycle and this is allowing an unwinding of the recent oversold trend condition. Resistance levels to watch are 4989.86, the 20-day EMA.

- Japan's NIKKEI closed higher by 457.2 pts or +1.35% at 34377.6 and the TOPIX ended 32.2 pts higher or +1.29% at 2530.23.

- Elsewhere, in China the SHANGHAI closed higher by 4.337 pts or +0.13% at 3280.341 and the HANG SENG ended 338.16 pts higher or +1.61% at 21395.14.

- Across Europe, Germany's DAX trades lower by 94.72 pts or -0.44% at 21218.81, FTSE 100 lower by 69.12 pts or -0.84% at 8206.48, CAC 40 down 45.42 pts or -0.62% at 7284.91 and Euro Stoxx 50 down 29.77 pts or -0.6% at 4937.3.

- Dow Jones mini up 297 pts or +0.75% at 40145, S&P 500 mini up 49.5 pts or +0.93% at 5355, NASDAQ mini up 189.75 pts or +1.03% at 18575.

COMMODITIES: WTI Weakness Puts Prices Through Support

Wednesday’s extension in Gold reinforces current bullish conditions. The yellow metal has traded to another fresh all-time high and confirmed a resumption of the primary uptrend. Note too that moving average studies are unchanged. A bearish theme in WTI futures remains intact and the rally on Apr 9 is - for now - considered corrective. The move higher is allowing an oversold trend condition to unwind. Recent weakness has resulted in the breach of a number of important support levels, reinforcing a bearish threat.

- WTI Crude up $0.49 or +0.78% at $62.94

- Natural Gas up $0.03 or +0.83% at $3.273

- Gold spot down $19.43 or -0.58% at $3324.68

- Copper down $9.25 or -1.95% at $464.45

- Silver down $0.33 or -1.01% at $32.4382

- Platinum down $9.89 or -1.02% at $962.76

| Date | GMT/Local | Impact | Country | Event |

| 17/04/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 17/04/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 17/04/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 17/04/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 17/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 17/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/04/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/04/2025 | 1230/0830 | *** | Housing Starts | |

| 17/04/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 17/04/2025 | 1245/1445 | ECB Monetary Policy press conference | ||

| 17/04/2025 | 1400/1000 | * | US Bill 08 Week Treasury Auction Result | |

| 17/04/2025 | 1400/1000 | ** | US Bill 04 Week Treasury Auction Result | |

| 17/04/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 17/04/2025 | 1530/1130 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 17/04/2025 | 1545/1145 | Fed Governor Michael Barr | ||

| 17/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 17/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 18/04/2025 | 2330/0830 | *** | CPI | |

| 18/04/2025 | 1500/1100 | San Francisco Fed's Mary Daly |