MNI US OPEN - China Finds Nvidia Violated Antitrust Law

EXECUTIVE SUMMARY

- CHINA FINDS NVIDIA VIOLATED ANTITRUST LAW AFTER INITIAL PROBE

- BESSENT AND HE MEET FOR SECOND DAY OF TRADE TALKS IN MADRID

- TRUMP EXPECTS A ‘BIG CUT’ FROM FEDERAL RESERVE THIS WEEK

- CHINA'S AUGUST INVESTMENT SLOWS TO FIVE-YEAR LOW

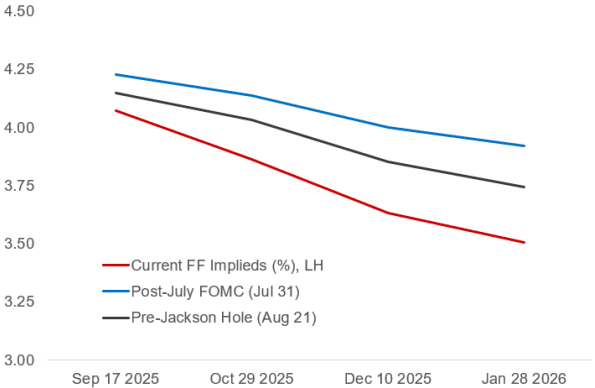

Figure 1: FOMC Meeting-Dated Fed Funds-Implied Rate Paths (%)

x-axis = FOMC decision dates. Source: Bloomberg Finance L.P., MNI

NEWS

MNI FED PREVIEW: A Reluctant Return to Easing

The Federal Reserve is set to resume its easing cycle at the September 16-17 meeting with a 25bp cut to the funds rate range to 4.00-4.25%. The decision to cut after a 5-meeting pause was well-telegraphed by Chair Powell, whose Jackson Hole speech described a “shifting balance of risks” toward a weaker labor market that “may warrant adjusting our policy stance”. The updated quarterly projections aren’t likely to bring many changes to the macroeconomic variables, but as usual the signal sent from the Fed rate “Dot Plot” will garner attention. A Committee split between expecting one or two further cuts this year is likely, keeping each of the remaining meetings of 2025 “live”.

US/CHINA (BBG): China Finds Nvidia Violated Antitrust Law After Initial Probe

China ruled that Nvidia Corp. violated anti-monopoly laws after concluding a preliminary investigation, ratcheting up the pressure on Washington during sensitive trade negotiations. The US chipmaker was found in violation of antitrust regulations, the State Administration for Market Regulation said in a one-sentence statement, without elaborating. The company has previously disclosed it’s facing scrutiny inside China, where regulators demanded it keep supplying local companies in return for regulatory approval of its acquisition of Mellanox.

US/CHINA (MNI): Bessent and He Meet for Second Day of Trade Talks in Madrid

MNI (London) Treasury Secretary Scott Bessent told reporters the US is "not willing to sacrifice national security," in pursuit of a trade deal with China, ahead of a second day of talks with Chinese Vice Premier He Lifeng in Spain, per Reuters. Reuters reports six hours of talks yesterday concluded with "no indication of a breakthrough" in trade or the Sept. 17 deadline for Chinese TikTok divestment. Bessent said the two sides are "very close" to a TikTok resolution but stressed, "it does not affect overall relationship with China."

US (BBG): Trump Expects a ‘Big Cut’ From Federal Reserve This Week

President Donald Trump predicted a “big cut” from the Federal Reserve this week ahead of a pivotal meeting at which the central bank’s governors are expected to ease policy for the first time in nine months. “I think you have a big cut,” Trump told reporters on Sunday on his way back to Washington. “It’s perfect for cutting.”

US/UK (BBG): US-UK Nuclear Pact to Precede Tech, Whisky Deals on Trump Visit

The US and Britain will sign an agreement to make it quicker for companies in both countries to build nuclear power stations when President Donald Trump visits this week, according to the UK government. The nuclear partnership is one of several economic deals that Prime Minister Keir Starmer’s administration intends to announce in an effort to keep Trump’s visit from descending into diplomatic and political difficulty. The president arrives in Britain on Tuesday, takes in a day of pageantry with King Charles III on Wednesday and meets Starmer on Thursday.

CHINA (MNI): China CPI Could Be Rebounding - NBS

MNI (Beijing) China’s Consumer Price Index (CPI) could be rebounding, supported by stronger consumer demand and seasonal factors, according to Fu Linghui, spokesperson for the National Bureau of Statistics. Upcoming holidays such as the Mid-Autumn Festival and National Day are expected to boost spending, while cooler weather may lift food demand, Fu said. However, careful analysis was needed to determine the overall trend, Fu cautioned, after August CPI reached minus 0.4% year‑on‑year, with core CPI up 0.9% year-on-year, an increase of 0.1 percentage point from July, marking the fourth consecutive month of growth.

RBA (MNI EXCLUSIVE): Wage Strength Key Risk to RBA Inflation Outlook

MNI looks at the key risks that could impact the RBA's outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

S.KOREA (BBG): South Korea Scraps Capital Gains Tax Plans After Retail Backlash

South Korea has abandoned a controversial plan to lower the capital gains tax threshold for stock investors, marking President Lee Jae Myung’s first major policy reversal since taking office in June. The decision follows months of opposition from Lee’s core voter base, many of whom are retail investors. Proposed changes — including lowering the capital gains tax threshold on stock holdings to 1 billion won ($717,535) from 5 billion won — raised questions about the government’s commitment to reviving the stock market and triggered a selloff in August that erased billions in value.

THAILAND (BBG): Thailand Said to Weigh Tax on Gold Trades to Slow Baht Rally

Thai authorities are considering a tax on physical gold trading to slow a rally in the nation’s currency that has threatened exports and tourism. The baht fell the most in six weeks. The Bank of Thailand and Ministry of Finance are discussing ways to tax gold bought and sold through various online channels and settled in baht, according to people familiar with the matter, who asked not to be identified as the information isn’t public. Any such levy may exempt gold traded in US dollars, on futures exchanges, or purchases made from bullion shops, the people said.

TURKEY (MNI): Local Stocks Rally, Yields Fall as Court Adjourns Key CHP Ruling

It had been widely expected that the Ankara court would issue a ruling of "absolute nullity" against the CHP's 38th Congress - which would have seen Chairman Ozgur Ozel ousted from his post - so today's decision to adjourn the case will provide some short-term relief to the CHP and markets. The next hearing is scheduled for October 24. Yields on local bonds have fallen over 30bps across the curve while the Borsa Istanbul 100 Index has rallied around 4%. 5-year CDS spreads - often cited by Turkish officials as a barometer for perceived risk - have fallen 5bps to their lowest level since March.

DATA

CHINA DATA (MNI): China’s August Investment Slows to Five-Year Low

- CHINA YTD FIXED-ASSET INVESTMENT +0.5% Y/Y VS MEDIAN +1.5%

- CHINA AUG INDUSTRIAL OUTPUT +5.2% Y/Y VS MEDIAN +5.6% Y/Y

- CHINA AUG RETAIL SALES +3.4% Y/Y VS MEDIAN +3.8% Y/Y

- CHINA AUG UNEMPLOYMENT RATE +5.3% VS JUL +5.2%

MNI (Beijing) China’s fixed-asset investment growth decelerated to 0.5% y/y in the Jan–Aug period from the previous 1.6%, marking the slowest pace since Aug 2020 and missing an expectation of 1.5%, National Bureau of Statistics data showed Monday. Property investment fell 12.9% in the first eight months, the sharpest drop since Feb 2020, after a 12.0% decline in Jan-Jul. Infrastructure and manufacturing investment grew 2.0% and 5.1%, down from 3.2% and 6.2%.

RATINGS: France Downgraded at Fitch, Iberians Receive Upgrades

Sovereign rating reviews of note from Friday include:

- Fitch downgraded France to A+; Outlook Stable

- Fitch upgraded Portugal to A; Outlook Stable

- Fitch affirmed South Africa at BB-; Outlook Stable

- S&P affirmed Croatia at A-; Outlook Positive

- S&P upgraded Spain to A+; Outlook Stable

- Morningstar DBRS confirmed Ireland at AA, Stable Trend

- Scope Ratings affirmed Austria at AA+; Outlook changed to Negative

- Scope Ratings affirmed Germany at AAA; Outlook Stable

- Scope Ratings affirmed the Netherlands at AAA; Outlook Stable

FOREX: AUD and GBP Moderately Outperforming

- The dollar index has operated within a 21 pip range on Monday, as markets await a stacked data and central bank calendar this week, headlined by the Fed. While moves remain moderate, the likes of AUD and GBP are outperforming early Monday.

- This has allowed AUDUSD to rise back towards cycle highs. Last week’s gains plus the breach of 0.6625, the Jul 24 high and bull trigger, confirmed a resumption of the technical uptrend, and the pair has narrowed the gap substantially to the US election related highs at 0.6688.

- It is worth noting that EURAUD sits over 3% below the late August highs, with a breach of trendline support and the July 31 low bolstering bearish momentum. Targets on the downside would include 1.7462 (Jun 10 low) and 1.7248 (May 14 low).

- GBPUSD broke above last Friday’s highs this morning to reach an intra-day high of 1.3599, briefly breaching the bull trigger located at 1.3595, the August 14 high. The rally that started Sep 3 has retraced the steep Sep 2 sell-off and highlights a stronger bullish development. This suggests the corrective cycle between Aug 14 - Sep 3 is over. UK Labour market figures, CPI data and the BOE will place a huge amount of attention on sterling this week.

- USDJPY is also a touch lower since the open, however, spot levels of 147.40 are not far from the mid-point of the recent 146.20-149.15 range. The Bank of Japan will also meet this week.

- US Empire State manufacturing data headlines a relatively quiet economic calendar on Monday. No surprises are expected from ECB President Lagarde, due to speak at Montaigne Institute’s 25th anniversary event, in Paris.

EGBS: Upside Bias for Futures This Morning; Ratings Decisions Digested

Major EGB futures have drifted higher through the morning, with Bunds +21 ticks at 128.77. Initial firm resistance is the Sep 12 high at 129.09.

- Early focus for EGBs was on the digestion of Friday’s ratings decisions. OATs modestly underperform Bunds after Fitch downgraded France’s rating to A+. The 10-year OAT/Bund spread reached an opening high of almost 81bps this morning, but has since eased back to 79.5bps (+0.5bps today). While a net-negative for OATs, the ratings decision didn’t come as a massive surprise.

- Meanwhile, upgrades for Spain (S&P to A+) and Portugal (Fitch to A) have contributed to SPGB and PGB outperformance. The 10-year SPGB/Bund spread is 1bp tighter at 56bps, while the PGB/Bund spread is 0.5bps tighter at 40bps.

- German yields are 1.5-2.5bps lower, with the belly of the curve outperforming.

- Early ECBspeak has not been market moving, with new Austrian CB Governor Kocher outlining his pragmatic stance to policy. The median respondent to the ECB’s latest Survey of Monetary Analysts still sees one more 25bp cut this cycle.

- The Eurozone July trade surplus was smaller-than-expected at E5.3bln (vs E12.0bln cons, E3.7bln prior).

GILTS: Parralel Downtick in Yields After Friday's Low in Futures Holds

Gilts continue to edge away from session lows after Friday’s base in futures held (91.14) and as wider core global FI markets trade on the front foot, last 91.40.

- The recent bullish cycle in the contract remains intact, with support and resistance of note located at 90.65 & 91.82.

- Yields ~3bp lower across the curve.

- Last week’s flattening left 2s10s and 5s30s 13bp & 11bp off their respective September closing highs as of Friday’s close.

- SONIA futures unchanged to +2.5.

- BoE-dated OIS continues to price ~8bp of easing through year-end.

- As noted earlier, we have plenty of domestic risk events of note this week, with labour market data (Tuesday), inflation readings (Wednesday) and the BoE decision (Thursday) all due.

- With Bank Rate expected to be left unchanged, focus should quickly move to the BoE’s QT decision.

- Expect our full previews in due course, but overviews of the 3 events can be found in our Global Week Ahead.

- Elsewhere, local headline flow points to the potential for VAT cuts on energy bills as part of the Budget, with the Chancellor reportedly leaving “all options on the table” when it comes to easing the cost-of-living burden, despite the ongoing fiscal headwinds.

- Elsewhere, U.S. investment intentions re: the UK have gotten some airtime.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Sep-25 | 3.976 | +0.9 |

Nov-25 | 3.935 | -3.2 |

Dec-25 | 3.884 | -8.3 |

Feb-26 | 3.770 | -19.7 |

Mar-26 | 3.738 | -22.9 |

Apr-26 | 3.669 | -29.8 |

EQUITIES: E-Mini S&P Remains in a Bullish Price Sequence

A corrective bear cycle in Eurostoxx 50 futures remains in play. Recent weakness resulted in a breach of 5370.21, the 50-day EMA. A clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, the contract has recovered above the 20-day EMA - a bullish development for now. The next resistance to watch is 5445.00, Aug 26 high. A bull cycle in S&P E-Minis remains intact and last week’s fresh cycle highs reinforce current conditions. The move higher confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on the 6685.25, a Fibonacci projection, and the 6700.00 handle. On the downside, initial support to watch is 6547.03, the 20-day EMA.

- In China the SHANGHAI closed lower by 10.094 pts or -0.26% at 3860.504 and the HANG SENG ended 58.4 pts higher or +0.22% at 26446.56.

- Across Europe, Germany's DAX trades higher by 137.47 pts or +0.58% at 23836.41, FTSE 100 lower by 2.69 pts or -0.03% at 9280.55, CAC 40 up 93.41 pts or +1.19% at 7918.65 and Euro Stoxx 50 up 47.55 pts or +0.88% at 5438.26.

- Dow Jones mini up 114 pts or +0.25% at 45967, S&P 500 mini up 7 pts or +0.11% at 6595, NASDAQ mini down 10.5 pts or -0.04% at 24102.75.

Time: 10:00 BST

COMMODITIES: Gold in a Clear Bull Cycle, Close to Recent Record Highs

The trend condition in WTI futures is unchanged - a bear cycle remains intact short-term gains are considered corrective. The pullback from the Sep 2 high highlights a possible recent reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would open $57.71, the May 30 low. Gold remains in a clear bull cycle and continues to trade at its recent highs. The yellow metal traded to a fresh all-time high once again, last week. The break higher confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, a Fibonacci projection. Initial firm support lies at $3504.1, the 20-day EMA.

- WTI Crude up $0.26 or +0.41% at $62.94

- Natural Gas up $0.02 or +0.82% at $2.964

- Gold spot up $1.54 or +0.04% at $3644.05

- Copper up $0.35 or +0.08% at $465.5

- Silver up $0.02 or +0.05% at $42.199

- Platinum up $3.49 or +0.25% at $1400.63

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 15/09/2025 | 1130/1330 | ECB Schnabel At EIB Chief Econ Meeting | ||

| 15/09/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/09/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/09/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/09/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 15/09/2025 | 1810/2010 | ECB Lagarde at Institut Montaigne Paris | ||

| 15/09/2025 | - | FOMC Meetings with S.E.P. | ||

| 16/09/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/09/2025 | 0800/1000 | *** | HICP (f) | |

| 16/09/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 16/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 16/09/2025 | 0900/1100 | ** | EZ Industrial Production | |

| 16/09/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/09/2025 | 1230/0830 | *** | CPI | |

| 16/09/2025 | 1230/0830 | *** | Retail Sales | |

| 16/09/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/09/2025 | 1230/0830 | *** | Retail Sales | |

| 16/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 16/09/2025 | 1315/0915 | *** | Industrial Production | |

| 16/09/2025 | 1400/1000 | * | Business Inventories | |

| 16/09/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 16/09/2025 | 1400/1000 | * | Business Inventories | |

| 16/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond |