MNI US OPEN - EUR/USD Back to Parity Pre-ECB

EXECUTIVE SUMMARY:

- EUR/USD EITHER SIDE OF PARITY AHEAD OF CRITICAL ECB MEETING

- UK FOCUS TURNS TO TRUSS' IMMINENT ENERGY ANNOUNCEMENT

- MARKETS SEES LITTLE IN BOJ/FSA/MOF MEETING ON YEN

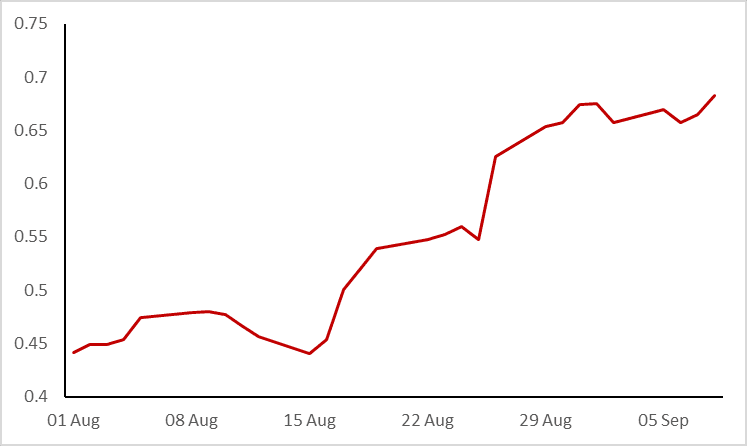

Figure 1: Implied ECB policy rate change creeping higher headed into today's meeting

NEWS

MNI ECB Preview – Hiking By Less Than 75bp Could Be Risky For The ECB

Despite dropping forward guidance given the current heightened degree of uncertainty, the ECB’s position on the policy rate path is relatively clear. There has been a notably hawkish shift since the July meeting, hiking in 25bp increments is no longer being discussed and the terminal rate is likely to be in the 1-2% range. So, we know that the ECB is in tightening mode and we have a reasonable idea of where the GC would like to get to (in the first instance). The two substantial unknowns are the pace of tightening and whether or not the ECB would continue hiking into a recession.

UK (MNI): Major Focus On PM's Energy Price Support Announcement ~1130BST

The eyes of financial markets, Westminster observers, and UK households and businesses will be trained on the House of Commons at around 1130BST (0630ET, 1230CET) as Prime Minister Liz Truss announces her gov'ts plan for alleviating pressures from rising energy prices.

WHITE HOUSE (MNI): Biden To Host Call w/Allies On Ukraine 1030ET

The call is expected to encompass a large number of US-aligned states/organisations, including the leaders of G7 states, as well as EU and NATO heads. Not confirmed if other national leaders are set to join the call.

JAPAN (MNI): BOJ Unmoved by Rising Inflation, Slumping Yen

The Bank of Japan will not relent on its ultra-easy policy settings and yield curve control despite a looming pick-up in inflation and a slide in the yen to its lowest level against the U.S. dollar since 1998, when Japan last intervened to support the currency.

MNI understands BOJ officials believe inflation may be rising faster than predicted despite recent retail price hikes and their pass-through being largely in line with forecasts made in July.

JAPAN (BBG): Kanda: Won’t Rule Out Any Options If FX Moves Continue

Japanese Vice Finance Minister for International Affairs Masato Kanda says Japan won’t rule out any response options if the current forex movements continue. Kanda also says fundamentals alone can’t justify recent yen moves.

AUSTRALIA (MNI): RBA’s Lowe Says Case for Slower Hikes Becoming Stronger

Reserve Bank of Australia governor Philip Lowe opened the door to a slower pace of interest rate rises in a speech: https://www.rba.gov.au/speeches/2022/sp-gov-2022-0... that defended the Bank's inflation-targeting framework.

The governor said the case for slowing the pace of hikes "becomes stronger as the level of the cash rate rises", adding rates had increased "very quickly" amid a normalisation of policy back to its estimated neutral rate of 2.5%.

DATA

JAPAN Q2 GDP REV +0.9% Q/Q; PRELIM +0.5%; MEDIAN +0.7%

JAPAN Q2 ANNUALIZED GDP REV +3.5%; PRELIM +2.2%; MEDIAN +2.9%

AUSTRALIA JUL TRADE BALANCE A$+8733

The July trade balance narrowed more than expected to A$8733 after A$17131 in June. The softer outcome was due to not only a sharper-than-expected fall in exports of 9.9% but also a significantly larger rise in imports of 5.2% on the month.

SWISS AUG UNEMPLOYMENT -0.1% M/M, -27.7% Y/Y

NORWAY JUL MAINLAND GDP -0.3% M/M, AGG GDP +0.3% M/M

FOREX: EUR Holds Recent Rally Ahead of Critical ECB Decision

- EUR/USD is holding the entirety of the Wednesday rally ahead of the ECB rate decision later today, keeping markets honed in on the sustainability of any strength above the parity level. ECB's Lagarde will be closely watched later today for any indications of the ECB's plans into year-end. First upside levels in the pair remain the 1.0090 Aug 26 high as well as 1.0029, the 20-day EMA.

- Antipodean currencies, namely the AUD and NZD, are underperforming ahead of NY hours, putting AUD/USD within range of first support at 0.6699, the Sep 7 Low ahead of the more notable bear trigger of 0.6682.

- The moves follow an appearance from RBA's Lowe overnight, who retained a dovish tilt in contrasting the bank's approach to policy relative to the more hawkish global central bank policy backdrop.

- Focus turns to the ECB rate decision and press conference, at which markets remain split in their view as to whether the bank will raise rates by 50 or 75bps. A similar scenario for the Fed's next rate decision raises the importance of a speech from the Fed Chair Jay Powell later today, who speaks shortly after the beginning of the ECB press conference.

- Additionally, the newly installed UK PM Truss is due to unveil some details on her plan to combat energy bills in the UK, with markets looking for clues on how her strategy could impact the UK Gilt remit going forward.

BOND SUMMARY: Three big events to drive price action

- Core fixed income is a little lower across the board with curves bear flattening - but moves have been limited ahead of three big events today.

- The ECB policy decision will be announced at 13:15BST/ 8:15ET with the press conference to follow at 13:45BST/ 8:45ET. Markets are pricing in 68bp for the decision (i.e. around a 72% probability of 75bp with 50bp fully priced). It is a close call, but the MNI Markets team expect a 75bp hike today. With inflation getting closer to double digits and the ECB already well behind it peers, hiking by ‘only’ 50bp could risk undermining the perceived commitment to restoring price stability. For the full MNI ECB preview see here.

- UK energy price cap: New PM Liz Truss is expected to confirm the broad outline of the plan to cap UK energy costs at around 11:15-11:30BST / 6:15-6:30ET. This is not expected to take the form of a formal ministerial statement - but is still expected to be announced in the House of Commons first. If it is not a formal statement, there will be no scheduled time for debate. It also suggests that although we will get the broad strokes of the plan, the announcement may be light on details. It may therefore be difficult to know the full fiscal implications of the plan.

- Fed Chair Powell is due to take part in a moderated discussion hosted by the Cato Institute at 14:10BST / 15:10CET. The subject of the conference will be "The State of Monetary Policy after 40 Years". Note that this will overlap with the ECB press conference.

- We will also hear from the Fed's Evans and Kashaki today.

- TY1 futures are up 0-2 today at 116-07+ with 10y UST yields down -0.9bp at 3.256% and 2y yields up 1.0bp at 3.444%.

- Bund futures are down -0.30 today at 144.86 with 10y Bund yields up 2.2bp at 1.595% and Schatz yields up 3.6bp at 1.122%.

- Gilt futures are down -0.36 today at 105.79 with 10y yields up 2.5bp at 3.055% and 2y yields up 2.7bp at 3.007%.

EQUITIES: Futures Indicate a Flat Open on Wall Street

- Japan's NIKKEI 225 closed up 634.98 pts or +2.31% at 28065.28 and the TOPIX ended 41.97 pts higher or +2.19% at 1957.62. China's SHANGHAI COMP closed down 10.708 pts or -0.33% at 3235.586 and the HANG SENG ended 189.68 pts lower or -1% at 18854.62.

- Across Europe, the German DAX down 4.77 pts or -0.04% at 12907.32, FTSE 100 up 20.42 pts or +0.28% at 7257.85, CAC 40 up 10.62 pts or +0.17% at 6114.28 and Euro Stoxx 50 up 1.59 pts or +0.05% at 3502.66.

- In US futures space, Dow Jones mini down 17 pts or -0.05% at 31564, S&P 500 mini up 1 pts or +0.03% at 3975.75, NASDAQ mini up 6.5 pts or +0.05% at 12268.

COMMODITIES: Bearish Threat Remains Present for WTI

A bearish threat in WTI futures remains present and this was reinforced yesterday as price traded through key support at $85.37, the Aug 16 low. The breach confirms a resumption of the downtrend that started Jun 8 and also highlights the end of a broad sideways move that has been in place since mid-July. Gold remains in a clear downtrend and short-term gains are considered corrective. Support at $1727.8, Aug 22 low has recently been breached to confirm a resumption of the bear cycle that started Aug 10.

- WTI Crude up $0.4 or +0.49% at $82.16

- Natural Gas down $0.02 or -0.19% at $7.823

- Gold spot up $1.1 or +0.06% at $1718.07

- Copper up $3.55 or +1.03% at $346.2

- Silver up $0.12 or +0.66% at $18.5686

- Platinum up $2.7 or +0.31% at $874.24

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/09/2022 | 1215/1415 | *** |  | EU | ECB Deposit Rate |

| 08/09/2022 | 1215/1415 | *** |  | EU | ECB Marginal Lending Rate |

| 08/09/2022 | 1215/1415 | *** |  | EU | ECB Main Refi Rate |

| 08/09/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 08/09/2022 | 1245/1445 |  | EU | ECB Post-Meeting Press Conference | |

| 08/09/2022 | 1310/0910 |  | US | Fed Chair Jerome Powell | |

| 08/09/2022 | 1400/1000 | * |  | US | Services Revenues |

| 08/09/2022 | 1415/1615 |  | EU | ECB President Lagarde's Podcast | |

| 08/09/2022 | 1430/1030 | ** |  | US | Natural Gas Stocks |

| 08/09/2022 | 1500/1100 | ** |  | US | DOE weekly crude oil stocks |

| 08/09/2022 | 1525/1125 |  | CA | BOC Deputy Rogers "Economic Progress Report" speech | |

| 08/09/2022 | 1530/1130 |  | US | New York Fed's Patricia Zobel | |

| 08/09/2022 | 1600/1200 |  | US | Chicago Fed's Charles Evans | |

| 08/09/2022 | 1900/1500 | * |  | US | Consumer Credit |