MNI US MARKETS ANALYSIS - Weaker Equity Picture Holds

Highlights:

- GBP softer, Gilts rally as Reeves gives strongest signal yet of "unpopular" tax policy

- Government shutdown in focus on reports of Senate Dems & GOP discussing off-ramps

- Quiet data schedule today, but picks up with private sector numbers Wednesday

US TSYS: Off Highs But Bull Steeper Amidst Broad Risk-Off

- Treasuries have traded bull steeper overnight, supported by broad risk-off moves with equity and crude oil futures under pressure throughout the session.

- Today sees a thin docket, headlined by Fed VC Supervision Bowman and a weekly retail sales indicator update. There is likely continued attention on corporate issuance after recent heavy supply from major names including Alphabet and Meta.

- Government shutdown proceedings will also be watched closely after leading Senate Republicans and Democrats talked of a possible off-ramp yesterday.

- Yesterday saw Treasury borrowing estimates below MNI expectations and at the lower end of most estimates seen. Current quarter borrowing requirements were lowered to $569B from August's $590B estimate and the initial estimate of Jan-Mar requirements saw a slight further uptick to $578B. The full QRA will as usual follow tomorrow (MNI preview here).

- Cash yields are 1.5-3bp lower, led by 2s. 2Y yields at 3.576% are off a session low of 3.564% but that still only pared about half of the push higher after a hawkish Powell last Wednesday.

- 2s10s at 51.7bp (+1bp) continues to lift off last week’s low of 46.4bp at what was its lowest since early August.

- TYZ5 trades at 112-25+ (+04) on solid cumulative volumes of 335k, off an overnight high of 112-28+.

- The earlier increase pushed it closer to resistance at 113-03 (20-day EMA) after which lies 113-18+ (Oct 28 high) but markets are likely still attentive to further declines with support seen at 112-16 (Oct 30 low).

- Data: Redbook retail sales the sole data release today. Trade, JOLTS and factory orders are all postponed under the government shutdown.

- Fedspeak: Bowman (0635ET)

- Bill issuance: US Tsy $95B 6W bill auction (1130ET)

- Politics: Trump has no public events scheduled. Press briefing by WH Press Sec Leavitt (1300ET)

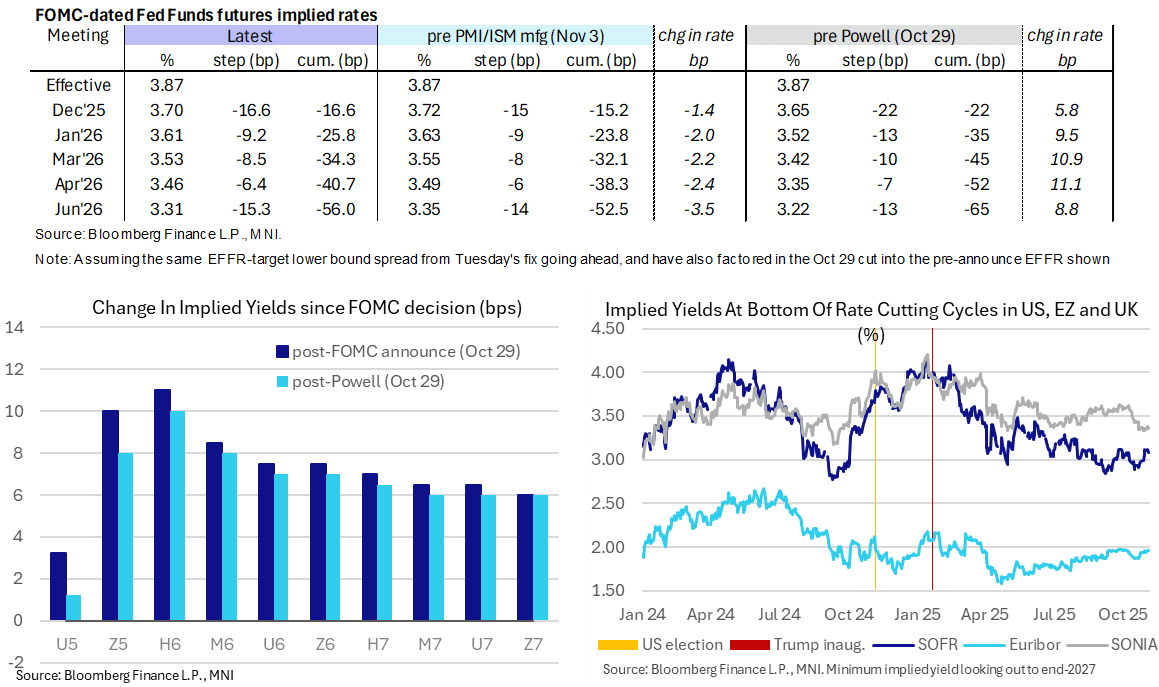

STIR: Fed Rate Path Softens, Bowman Next Up In Early Remarks From Spain

- Fed Funds implied rates have more than unwound yesterday’s increase, dipping 1bp for Dec, 1.5bp for Mar and 3bp for June in steady moves through European hours.

- Broader risk-off plays a role with equity and crude oil futures under pressure, the latter with WTI -1.6%.

- Cumulative cuts from assumed 3.87% effective: 16.5bp Dec, 26bp Jan, 34.5bp Mar, 40.5bp Apr, 56bp Jun.

- SOFR futures are up to +0.03 on the day through M6-M7 contracts, with the terminal implied yield of 3.085% (H7) pulling back a touch off yesterday’s highest close since August.

- Today's sole Fedspeak comes from VC Supervision Bowman (voter), earlier than usual at 0635ET being in Spain. She will speak on supervision and mon pol but with no prepared text.

- Second only to Miran as the most dovish FOMC member, we expect similar rhetoric to pre-FOMC meeting remarks that bigger and faster cuts may be warranted with the possibility that the Fed has fallen behind the curve on weakening labor market conditions. She’s one of the 9 rate dots at 3.6% and we would guess one of the 5 who are either at 2.6% or 2.9% for 2026.

- Updating on latest notable Fedspeak, Gov. Cook in long-awaited remarks yesterday supported last week’s cut as “the downside risks to employment are greater than the upside risks to inflation”. Keeping rates “modestly restrictive” is “appropriate given that inflation remains somewhat above our 2 percent target."

SOFR: Mix Of Long And Short Setting Dominates In Futures On Monday

OI data points to net long setting dominating in the whites on Monday (only interrupted by net long cover in SFRU5), while net short setting dominated in the reds, greens and blues. Contracts finished mixed, flat to -/+1.0 vs. Friday's close.

| 03-Nov-25 | 31-Oct-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,379,509 | 1,395,480 | -15,971 | Whites | +96,944 |

SFRZ5 | 1,521,053 | 1,461,382 | +59,671 | Reds | +29,396 |

SFRH6 | 1,195,353 | 1,161,013 | +34,340 | Greens | +20,464 |

SFRM6 | 1,094,766 | 1,075,862 | +18,904 | Blues | +15,164 |

SFRU6 | 1,081,294 | 1,071,525 | +9,769 |

|

|

SFRZ6 | 1,149,298 | 1,147,647 | +1,651 |

|

|

SFRH7 | 815,079 | 809,080 | +5,999 |

|

|

SFRM7 | 769,754 | 757,777 | +11,977 |

|

|

SFRU7 | 746,529 | 734,862 | +11,667 |

|

|

SFRZ7 | 794,763 | 800,131 | -5,368 |

|

|

SFRH8 | 413,813 | 403,438 | +10,375 |

|

|

SFRM8 | 401,001 | 397,211 | +3,790 |

|

|

SFRU8 | 327,677 | 321,296 | +6,381 |

|

|

SFRZ8 | 319,872 | 316,348 | +3,524 |

|

|

SFRH9 | 207,758 | 205,365 | +2,393 |

|

|

SFRM9 | 185,027 | 182,161 | +2,866 |

|

|

US TSY FUTURES: Mix Of Positioning Swings On Monday

OI data points to a mix of net long setting (TU), short cover (FV), long cover (UXY & US) and short setting (WN) as the curve twist steepened on Monday.

- TY futures were unchanged at settlement, which makes it difficult to provide any real inference outside of a reduction in exposure in that contract as OI fell on the day.

| 03-Nov-25 | 31-Oct-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,619,373 | 4,591,349 | +28,024 | +1,061,144 |

FV | 6,793,050 | 6,803,885 | -10,835 | -466,585 |

TY | 5,446,807 | 5,478,536 | -31,729 | -2,126,931 |

UXY | 2,476,446 | 2,483,642 | -7,196 | -647,931 |

US | 1,890,063 | 1,904,279 | -14,216 | -1,817,484 |

WN | 2,134,510 | 2,124,699 | +9,811 | +1,844,231 |

|

| Total | -26,141 | -2,153,556 |

SCANDIS: Global Risk Backdrop More Relevant For Scandi FX Than CBs This Week

- The global risk backdrop is likely to exert more influence on Scandi FX than domestic central bank decisions this week. Both NOK and SEK trade poorly owing to this morning’s pullback in European and US equities, with an associated fall in crude futures placing additional pressure on NOK. Technical and fundamental factors continue to suggest the risk in NOKSEK is skewed to the downside, for now.

- EURSEK is +0.4% at 10.97, still within the 10.90-11.10 range that has contained price action since September. Modest gains over the last 8 sessions are considered corrective, with resistance seen at the 50-day EMA of 11.0007.

- EURNOK is +0.55% at 11.73, piercing the 50-day EMA and narrowing the gap to resistance at 11.8320 (Oct 17 high).

- Upside in NOKSEK continues to be capped by the historically important 0.9500 level, which coincides closely with trendline resistance drawn from the March 2022 highs. Moving average studies also returned to a bear-mode setup in October. Improving Swedish growth signals (alongside some softness in recent Norwegian data) may argue in favour of further SEK outperformance vs NOK in the coming months.

- Both the Riksbank and Norges Bank are expected to hold rates steady and make minimal guidance changes this week.

- MNI’s Riksbank preview ahead of tomorrow’s decision is here

- Our Norges Bank preview will be released later today.

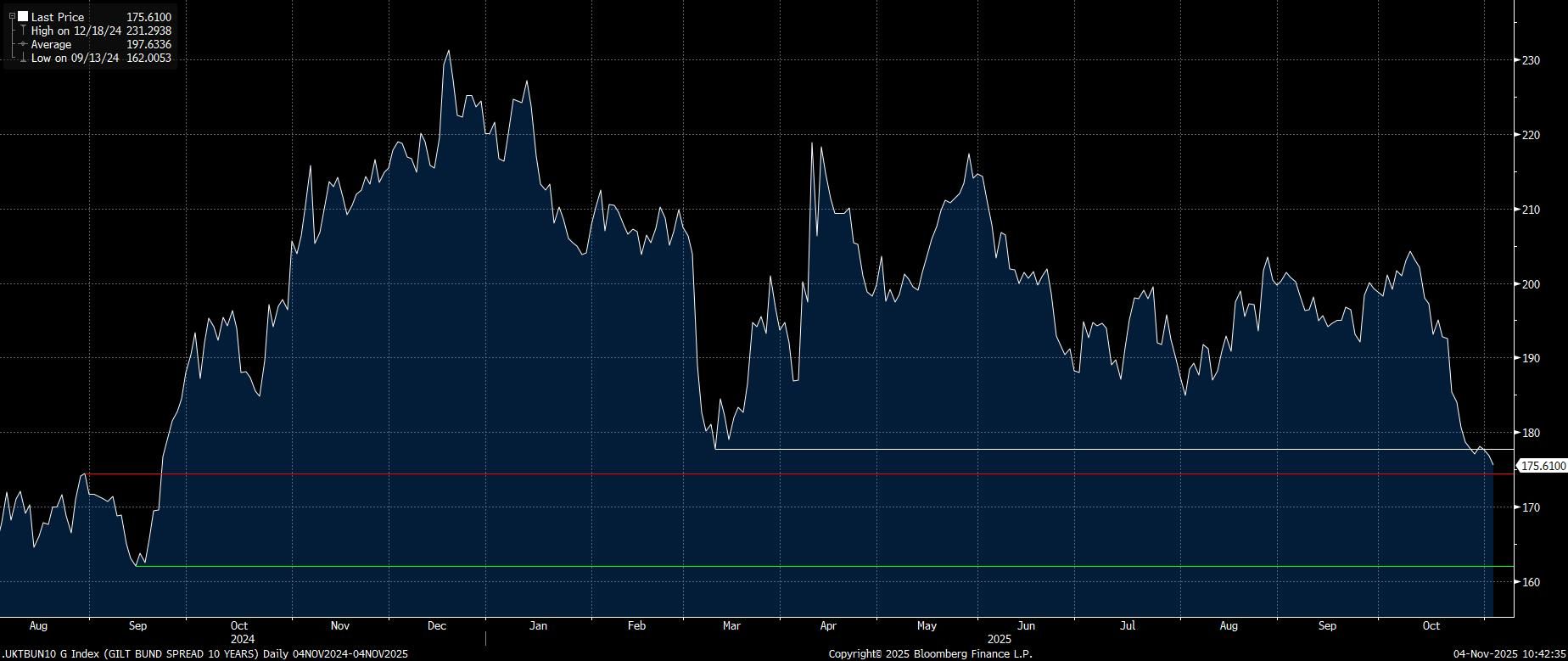

BONDS: Next Triggers Eyed As Gilts/Bunds On Track For Lowest Close Of 2025

We think the space for gilt outperformance vs. Bunds has narrowed following this morning's appearance from UK Chancellor Reeves.

- However, there are some potential triggers for further UK outperformance in the pipeline:

- A BoE rate cut this week. We have already characterised the decision as closer to 50/50 (cut/hold), while the market prices ~7bp of easing.

- A combination of lowering the threshold for the higher rate of tax as well as increases to higher and additional tax rates in the Budget.

- Reeves’ choice to drop the pledge to not hike taxes on working people may open the way for NI/basic tax rate increases. This would be gilt positive, via funding channels and the economic hit that it would deliver, which could deepen BoE easing.

- The latter could be bolstered by energy bill and administrative cost cuts, which would further contain inflation.

- Elsewhere, continued skew away from long end issuance in the updated DMO gilt remit (which will be published as the Budget concludes) is at least partly in the price. We will look at GEMM expectations ahead of the Budget to establish a benchmark here.

- Next downside closing levels of note for the gilt/Bund spread: Aug 29 '24 close (174.4bp) & Sep 13 '24 close (162.0bp).

Fig. 1: Gilt/Bund Spread (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

EUROPE ISSUANCE UPDATE:

RAGB Results

- E863mln (E750mln allotted) of the 2.95% Feb-35 RAGB. Avg yield 2.891% (bid-to-cover 2.36x; bid-to-issue 2.05x).

Schatz Results

- E5bln (E3.766bln allotted) of the 2.00% Dec-27 Schatz. Avg yield 1.98% (bid-to-offer 1.26x; bid-to-cover 1.67x).

Gilt Results:

- Decent long 3-year gilt auction but the lowest accepted price of 100.489 only matched the pre-auction midprice (rather than exceeding). However, with GBP5bln sold and a bid-to-cover of 3.06x that can't be described in any way as a disappointing auction.

- GBP5bln of the 4.00% May-29 Gilt. Avg yield 3.845% (bid-to-cover 3.06x, tail 0.4bp).

EFSF Dual Tranche Syndication:

- E3bln of the new 5-year Nov 30 bond (MNI expected E2.5-3.5bln). Spread set at MS+22bps (guidance was MS+24 bps area). Books in excess of E13bln (ex JLM interest)

- E1.5bln tap of the 2.875% Jan-2035 bond (MNI expected E1.0-2.0bln). Spread set at MS+39bps (guidance was MS+42 bps area). Books in excess of E19bln (ex JLM interest)

FOREX: GBP Soft on Clearest Signal Yet of "Unpopular" Tax Policy Ahead

- GBP traded softer on the back of another pre-Budget appearance from UK Chancellor Reeves. While not drawn into details on the Budget measures specifically - it was certainly her clearest signal yet that sizeable tax rises are incoming (suggested by the statement of working in the national interest, rather than political popularity), as well as indicating her intention to pave the way with fiscal policy to allow for further BoE rate cuts.

- What does this mean for GBP? GBPUSD has broken to a new pullback low - trading at comparable levels with the Liberation Day rally in April. This makes 1.3041, the Apr 14 low the area of interest ahead of 1.2971, the 1.382 proj of the Sep 17 - 25 - Oct 1 price swing.

- Outside of GBP, risk-off trade pervades after slippage in US equity futures held through overnight trade and remains the dominant theme into the crossover. Palantir is set to drop over 7% at the open as markets caution on extreme valuations and the scale of the recent rally - a move mirrored in South Korea's SK Hynix overnight - a key supplier to Nvidia.

- Resultantly, the best performing currency today is JPY, rallying against all others, will risk proxy currencies slide - namely the NZD. Initial support in USD/JPY comes in at 153.27, followed by 152.06. The technical trend structure in the pair remains bullish at this stage.

- JOLTs, trade balance and durable goods orders data were originally set for release today - but the extension of the government shutdown will keep focus on private sector data and corporate earnings as the best bellwether for the state of the economy. As such, tomorrow's ADP employment change, S&P Global final PMI and ISM services index are of utmost importance.

OPTIONS: Expiries for Nov4 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1475(E651mln), $1.1525(E1.1bln), $1.1635-40(E1.3bln)

- GBP/USD: $1.3150(Gbp510mln)

- AUD/USD: $0.6625-30(A$1.2bln)

EQUITIES: Short-Term Weakness for Eurostoxx Futures Considered Corrective

Short-term weakness in Eurostoxx 50 futures is considered corrective. The contract has breached the 20-day EMA, signalling scope for a deeper retracement towards support at the 50-day EMA, at 5567.19. Support below the EMA lies at 5549.50, the base of a bull channel drawn from the Aug 1 low. A breach of this level and the 50-day EMA, is required to highlight a stronger reversal. Key resistance and bull trigger is 5742.00, the Oct 29 high. The trend condition in S&P E-Minis is unchanged, it remains bullish and the latest pullback appears corrective. Attention is on support at the 20-day EMA, at 6804.03. A clear break of this level average would signal scope for a deeper retracement and expose the 50-day EMA at 6698.11 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the uptrend.

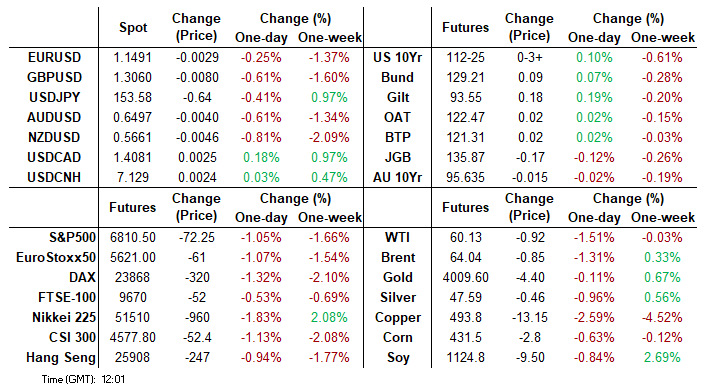

- Japan's NIKKEI closed lower by 914.14 pts or -1.74% at 51497.2 and the TOPIX ended 21.69 pts lower or -0.65% at 3310.14.

- Elsewhere, in China the SHANGHAI closed lower by 16.335 pts or -0.41% at 3960.186 and the HANG SENG ended 205.96 pts lower or -0.79% at 25952.4.

- Across Europe, Germany's DAX trades lower by 425.99 pts or -1.77% at 23708.36, FTSE 100 lower by 102.59 pts or -1.06% at 9598.75, CAC 40 down 127.82 pts or -1.58% at 7981.97 and Euro Stoxx 50 down 89.91 pts or -1.58% at 5589.34.

- Dow Jones mini down 414 pts or -0.87% at 47060, S&P 500 mini down 79 pts or -1.15% at 6803.75, NASDAQ mini down 385.5 pts or -1.48% at 25717.25.

COMMODITIES: WTI Futures Remain in a Corrective Cycle for Now

WTI futures remain in a corrective cycle for now. Note that price has recently traded through the 50-day EMA, currently at $61.05. The breach of this EMA signals scope for a stronger recovery. Note too that a resistance at $62.34, the Oct 8 high, has also been pierced. A clear move through it would expose key resistance at $65.77, the Sep 26 high. First key support and the bear trigger is unchanged at $55.96, the Oct 20 low. Gold is unchanged. A fresh cycle low last week highlights an extension of the bear cycle that started Oct 20. The retracement since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3864.7. Clearance of this EMA would strengthen a short-term bear theme. Initial resistance is at $4161.4, the Oct 22 high.

- WTI Crude down $0.79 or -1.29% at $60.23

- Natural Gas down $0.02 or -0.54% at $4.243

- Gold spot down $7.98 or -0.2% at $3991.65

- Copper down $11.9 or -2.35% at $495

- Silver down $0.3 or -0.63% at $47.749

- Platinum down $16.14 or -1.03% at $1553.83

| Date | GMT/Local | Impact | Country | Event |

| 04/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 04/11/2025 | 2100/1600 | Canada federal budget, release expected just after 4pm EST | ||

| 05/11/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 05/11/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 05/11/2025 | - | Riksbank Meeting | ||

| 05/11/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/11/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 05/11/2025 | 0700/0800 | ** | Manufacturing Orders | |

| 05/11/2025 | 0745/0845 | * | Industrial Production | |

| 05/11/2025 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0830/0930 | *** | Riksbank Interest Rate Decison | |

| 05/11/2025 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0900/1000 | * | Retail Sales | |

| 05/11/2025 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 05/11/2025 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 05/11/2025 | 1000/1100 | ** | EZ PPI | |

| 05/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 05/11/2025 | 1315/0815 | *** | ADP Employment Report | |

| 05/11/2025 | 1330/0830 | *** | Treasury Quarterly Refunding | |

| 05/11/2025 | 1445/0945 | *** | S&P Global Services Index (final) | |

| 05/11/2025 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 05/11/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 05/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 05/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 05/11/2025 | 1610/1610 | BOE Breeden At SALT Blockchain Event | ||

| 06/11/2025 | 2330/0830 | ** | Average Wages (p) |