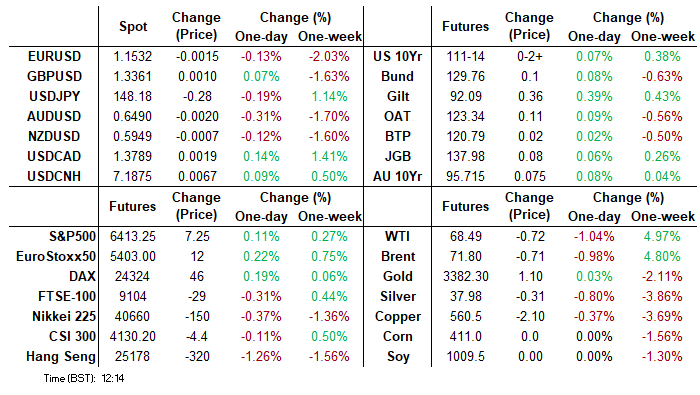

MNI US MARKETS ANALYSIS - Tsys Press Higher Ahead of Busy Day

Highlights:

- Treasuries testing resistance ahead of busy session

- FOMC decision, Quarterly refunding to be carefully watched

- USD Index higher for the fifth consecutive session

US TSYS: TYA Tests Resistance Ahead Of Important Docket

- Treasuries have recently firmed, helped by a contained bid in EGBs seemingly following German budget figures, modestly extending yesterday’s sizeable bull flattening.

- It’s ahead of a busy session that sees ADP employment, flash GDP estimates for Q2, Treasury’s Quarterly Refunding Announcement and then the FOMC (preview links below). President Trump will also make a final call on yesterday’s touted China tariff truce extension.

- Cash yields are 0.3-0.8bp lower on the day, with the long-end lagging declines. 10Y yields of 4.314% still target a test down to 4.30%.

- TYU5 has recently nudged up to a session high of 111-14+ (+ 03) having earlier kept to a narrow range of 111-09+ to 111-13, on modest cumulative volumes of 275k.

- It tests resistance at 111-14+ (Jul 22 high) after which lies 111-28 (Jul 3 high). To the downside, support is seen at 110-19+ (Jul 24 low).

- Data: ADP employment Jul (0815ET), GDP/PCE 2Q A (0830ET), Pending home sales Jun (1000ET)

- Fed Preview: FOMC decision 1400ET, presser 1430ET. https://media.marketnews.com/Fed_Prev_Jul2025_With_Analysts_002622ac0e.pdf

- QRA Preview: 0830ET. https://media.marketnews.com/MNI_US_Deep_Dive_Issuance_2025_07_Refunding_e2af296ce5.pdf

- Monday’s Treasury borrowing estimates were almost exactly in line with MNI's estimates. We would characterize the current quarter as slightly on the high side of the median analyst expectation, with the latter quarter fairly close to expectations given what is usually a wide range for the further-out quarter. It should have little to no impact on expectations for Wednesday's Refunding announcement.

- Bill issuance: US Tsy $65B 17W bill auction (1130ET)

- Politics: Trump to make final call on a China tariff truce extension today. He also signs a Congressional Bill at 1330ET (closed press) and delivers remarks on Making Health Technology Great Again (1600ET)

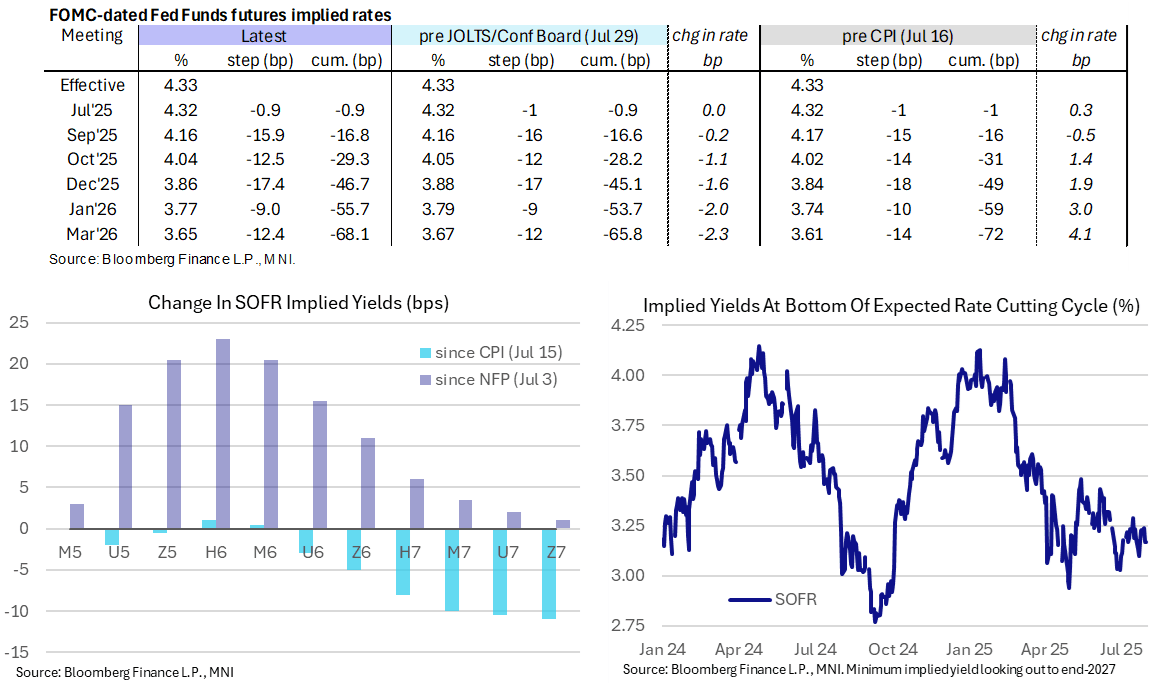

STIR: Next Fed Cut Seen In Oct; FOMC Ahead After ADP and GDP

- Fed Funds implied rates hold yesterday’s decline that was helped by but started before softer 1000ET data including a broadly dovish JOLTS report relative to expectations.

- Cumulative cuts from 4.33% effective: 1bp for today’s decision, 17bp Sep, 29.5bp Oct, 46.5bp Dec, 55.5bp Jan, 68bp Mar.

- The SOFR implied terminal yield of 3.17% (SFRH7) is unchanged on the day, holding yesterday’s 7bp decline to push back towards the middle of the 3.1-3.3% range seen through July.

- MNI Fed Preview for today’s decision: https://media.marketnews.com/Fed_Prev_Jul2025_With_Analysts_002622ac0e.pdf

- Before then, ADP employment (0815ET) and flash Q2 GDP/PCE estimates (0830ET) headline data with the latter landing alongside Treasury’s QRA in case there is any spillover from surprises in shorter-dated issuance plans. In addition, President Trump is set to make a final call on a China tariff truce extension, with one touted option being for 90 days.

SOFR: Mix Of Long Setting & Short Cover In Futures On Tuesday

OI data points to a mix of net long setting and short cover during Tuesday’s rally.

- Overall positioning swings were fairly modest, with net short cover between SFRZ6 and SFRM7 probably providing the most concentrated positioning move.

| 29-Jul-25 | 28-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,260,045 | 1,257,760 | +2,285 | Whites | +5,144 |

SFRU5 | 1,319,492 | 1,316,086 | +3,406 | Reds | -7,186 |

SFRZ5 | 1,342,364 | 1,344,267 | -1,903 | Greens | -6,121 |

SFRH6 | 1,055,323 | 1,053,967 | +1,356 | Blues | +6,060 |

SFRM6 | 864,233 | 858,978 | +5,255 |

|

|

SFRU6 | 837,498 | 834,059 | +3,439 |

|

|

SFRZ6 | 923,717 | 929,569 | -5,852 |

|

|

SFRH7 | 708,192 | 718,220 | -10,028 |

|

|

SFRM7 | 696,469 | 702,617 | -6,148 |

|

|

SFRU7 | 526,478 | 526,555 | -77 |

|

|

SFRZ7 | 452,477 | 453,078 | -601 |

|

|

SFRH8 | 332,005 | 331,300 | +705 |

|

|

SFRM8 | 231,225 | 225,590 | +5,635 |

|

|

SFRU8 | 198,932 | 201,092 | -2,160 |

|

|

SFRZ8 | 201,281 | 199,571 | +1,710 |

|

|

SFRH9 | 144,045 | 143,170 | +875 |

|

|

US TSY FUTURES: Net Long Setting Dominated During Tuesday's Rally

OI data points to net long setting dominating across much of the curve on Tuesday, only interrupted by a modest round of net short cover in FV futures.

- A net $12.6mln of DV01 equivalent was added across the curve, with TY futures seeing the biggest positioning move, likely aided by feedthrough from strong demand at the 7-Year auction.

| 29-Jul-25 | 28-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,420,880 | 4,382,663 | +38,217 | +1,413,708 |

FV | 6,937,480 | 6,956,801 | -19,321 | -825,227 |

TY | 4,936,861 | 4,842,034 | +94,827 | +6,235,175 |

UXY | 2,417,573 | 2,412,794 | +4,779 | +416,224 |

US | 1,789,873 | 1,777,293 | +12,580 | +1,747,295 |

WN | 1,951,782 | 1,931,653 | +20,129 | +3,638,690 |

|

| Total | +151,211 | +12,625,865 |

EU: Commission-18 Countries Apply For EUR127bln In Defence Loans Under SAFE

The European Commission has confirmed that an initial 18 member states have applied for a combined EUR127bln in loans to fund military procurement as part of the Security Action for Europe (SAFE) Defence Instrument. Belgium, Bulgaria, Czechia, Estonia, Greece, Spain, France, Croatia, Italy, Cyprus, Latvia, Lithuania, Hungary, Poland, Portugal, Romania, Slovakia and Finland have all applied under the scheme, with applications running to 30 November.

- Euractiv outlines the process of application, assessment, and disbursal of funds: "Member states now have six months from the entry into force of the Regulation [29 May] to submit their initial national plans, which the Commission will then assess. Following a Commission proposal, the Council is expected to adopt implementing decisions, which will include the size of the loan and any pre-financing. Pre-financing, which can be up to 15% of the loan, will ensure that support can be paid swiftly to cover the most urgent needs, potentially starting in 2025. Member states will need to report on the progress of implementation when they submit their payment requests, which can be done twice a year. The last approval for disbursements can take place until 31 December 2030."

- The SAFE loans are seen as a major component of the 'Readiness 2030' plans (formerly known as 'ReArm Europe', but changed due to political sensitivities in Italy and Spain), alongside allowing the 'national escape clause' of the Stability and Growth Pact to allow for increased defence spending up to an additional 1% of GDP.

ISRAEL: UK To Join France In Palestine Recognition; No Sign Of U-Turn From PM

On the evening of 29 September, UK PM Sir Keir Starmer announced that if Israel does not agree to a ceasefire in Gaza and take “substantive steps” towards a two-state solution, then the UK will recognise a Palestinian state at the upcoming UN General Assembly in September. This mirrors the policy of French President Emmanuel Macron. The French delegation at the UN penned a joint statement late on 29 July, which saw the foreign ministers of 15 nations (including Australia and Canada) call for a two-state solution. All signatories either recognise a Palestinian state or have expressed the intention to do so.

- The Israeli Foreign Ministry posted on X that “The shift in the British government’s position at this time, following the French move and internal political pressures, constitutes a reward for Hamas and harms efforts to achieve a ceasefire in Gaza and a framework for the release of hostages,”. The move has been criticised by the main opposition Conservatives, while released British hostage Emily Damari accused Starmer of "moral failure" on the issue.

- With the Israeli negotiating team having been recalled from Qatar last week, there has been little sign of the US or Israeli gov'ts moving towards ceasefire talks. The words and actions of the UK, France and other European countries has had close to zero impact on the actions of the Netanyahu gov't during the course of the conflict since 7 Oct 2023, and there is little to suggest there will be a change at this time.

FOREX: AUDJPY Tests Support At 20-day EMA; Focus On Heavy NA Calendar Before BOJ

AUDJPY is down 0.5% today, testing initial support at the 20-day EMA of 96.157. This EMA has underpinned price action in the cross since June 4, so a close below it would be an important bearish development. Clearance of 96.157 would expose the July 22 low at 96.632. The reaction in risk assets to this afternoon’s heavy North America calendar (US QRA, US Q2 GDP, BOC decision and of course the FOMC) will be key for the cross in the immediate term.

- News of an earthquake off the coast of Russia (which could be the sixth strongest on record) prompted light safe haven flows into the JPY overnight. However, Japan has since downgraded its tsunami alert in some areas. USDJPY is down 0.3% today at 148.00, but a bull cycle remains in place. Initial support is the 20-day EMA at 147.07.

- The BOJ is expected to maintain its policy rate at 0.5% overnight. Given there is no immediate need to raise rates, the BoJ is expected to maintain a wait-and-see approach. Markets will pay close attention to Governor Ueda’s tone during the post-meeting press conference. Ueda has maintained a cautious stance since May, but if the forecasts and risk assessments are revised higher, there’s a likelihood his tone may shift. MNI’s full BOJ preview is here.

- Meanwhile, the weaker-than-expected Q2 inflation report has applied pressure to AUD today. AUDUSD has pierced support at the 50-day EMA of 0.6505. A close below would signal scope for a stronger bearish reversal.

- The RBA is now fully expected to deliver a 25bp cut at its August 12 decision, with focus on whether further easing can be delivered in September (OIS price 36bps of cuts at typing).

EUROPE ISSUANCE UPDATE:

UK tender results

- GBP0.3bln of the 3.75% Jul-52 Gilt. Avg yield 5.383% (bid-to-cover 4.62x, tail 0.3bp).

Italy auction results

- E1.5bln of the 1.35% Apr-30 BTP. Avg yield 2.6% (bid-to-cover 1.78x).

- E2bln of the 2.70% Oct-30 BTP. Avg yield 2.8% (bid-to-cover 1.72x).

- E3.5bln of the 3.60% Oct-35 BTP. Avg yield 3.52% (bid-to-cover 1.59x).

- E2bln of the 1.05% Apr-34 CCTeu. Avg yield 3.13% (bid-to-cover 1.68x).

Dutch DTCs to become tradable on Euronext Amsterdam

- The DSTA has also announced that "DTCs with a maturity date in 2026 and onwards will become tradeable on Euronext Amsterdam". This is "in order to promote liquidity and broaden investor access to money market instruments issued by the Dutch State."

- 2025 maturity DTCs will still not be exchange-tradable on Euronext.

- The first listed DTC will be the new 6-month Jan 29, 2026 DTC which is due for auction on Monday 4 August.

OPTIONS: Expiries for Jul30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1525(E765mln), $1.1550(E902mln), $1.1700-10(E1.1bln), $1.1800(E1.7bln)

- USD/JPY: Y147.50($878mln), Y148.25-30($989mln), Y148.65($945mln), Y149.00($853mln)

- AUD/USD: $0.6550(A$1.0bln), $0.6600-10(A$1.2bln)

- USD/CAD: C$1.3695-10($969mln), C$1.3770-75($1.7bln)

EQUITIES: E-Mini S&P Remains in a Bullish Price Sequence

- The trend condition in Eurostoxx 50 futures is unchanged, it remains bullish and short-term weakness appears corrective. Support at 5281.00, the Jul 1 / 4 low, remains intact. A clear break of this level would strengthen a bearish threat. For bulls, a resumption of gains would refocus attention on the bull trigger at 5486.00, the May 20 high. It has recently been pierced, a clear breach of it would resume the bull cycle and open 5500.00.

- The trend set-up in S&P E-Minis remains bullish. Recent cycle highs once again confirm a resumption of the uptrend and maintain the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, a Fibonacci projection. Key support is at the 50-day EMA, at 6173.21. Support at the 20-day EMA is at 6322.32.

COMMODITIES: Gold Continues to Trade Close to Support at 50-Day EMA

- WTI futures traded higher yesterday highlighting an extension of the current corrective cycle. $69.41, the 50.0% retracement of the Jun 23-24 downleg, has been pierced. A continuation higher would open $70.96 next, the 61.8% retracement point. On the downside, support to watch is the 50-day EMA, at $65.02. The average has been pierced, a clear break of it would expose $58.17, the May 30 low.

- Gold has pulled back from its Jul 23 high. Short-term weakness is considered corrective - for now - and a bull cycle that started Jun 30 remains intact. However, the yellow metal has traded through support at $3323.0, the 50-day EMA. A clear break of this level would signal scope for a deeper retracement and expose the next key support at $3282.8, the Jul 9 low. Key near-term resistance is $3439.0, the Jul 23 high. A break of this hurdle would be bullish.

| Date | GMT/Local | Impact | Country | Event |

| 30/07/2025 | 1215/0815 | *** | ADP Employment Report | |

| 30/07/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/07/2025 | 1230/0830 | *** | Treasury Quarterly Refunding | |

| 30/07/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 30/07/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 30/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 30/07/2025 | 1430/1030 | BOC press conference | ||

| 30/07/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 30/07/2025 | 1800/1400 | *** | FOMC Statement | |

| 31/07/2025 | 2350/0850 | * | Retail Sales (p) | |

| 31/07/2025 | 2350/0850 | ** | Industrial Production | |

| 31/07/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/07/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 31/07/2025 | 0130/1130 | * | Building Approvals | |

| 31/07/2025 | 0130/1130 | ** | Retail Trade | |

| 31/07/2025 | 0130/1130 | *** | Retail trade quarterly | |

| 31/07/2025 | 0130/1130 | ** | Trade price indexes | |

| 31/07/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 31/07/2025 | 0600/0800 | ** | Import/Export Prices | |

| 31/07/2025 | 0630/0830 | ** | Retail Sales | |

| 31/07/2025 | 0645/0845 | *** | HICP (p) | |

| 31/07/2025 | 0645/0845 | ** | PPI | |

| 31/07/2025 | 0755/0955 | ** | Unemployment | |

| 31/07/2025 | 0800/1000 | *** | Bavaria CPI | |

| 31/07/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 31/07/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 31/07/2025 | 0900/1100 | ** | Unemployment | |

| 31/07/2025 | 0900/1100 | *** | HICP (p) | |

| 31/07/2025 | 1000/1200 | ** | PPI | |

| 31/07/2025 | 1200/1400 | *** | HICP (p) | |

| 31/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 31/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 31/07/2025 | 1230/0830 | * | Payroll employment | |

| 31/07/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 31/07/2025 | 1230/0830 | *** | Employment Cost Index | |

| 31/07/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/07/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 31/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 31/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 31/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result |