MNI US MARKETS ANALYSIS - Tsys Firmer After Long Weekend

Highlights:

- Treasuries open stronger following Presidents' Day closure, Iran-US talks in focus

- GBP softer, BoE rate cut pricing brought forward on highest unemployment rate since COVID

- Weekly ADP, three Fedspeakers and bill issuance in focus

US TSYS: Gains Pared After Latest Clearance Of TYH6 Resistance

Treasuries sit firmer from Friday’s close across the curve, with cash open again after Presidents’ Day, although have pared latest gains overnight which included a clearer breach of latest resistance for TYH6. Geopol risks were touted as drivers behind yesterday's net gains for futures whilst the second round of indirect US-Iran nuclear talks has got underway in Geneva today. Headlines aside, today sees data focus on weekly ADP, three Fedspeakers and heavier than usual bill issuance.

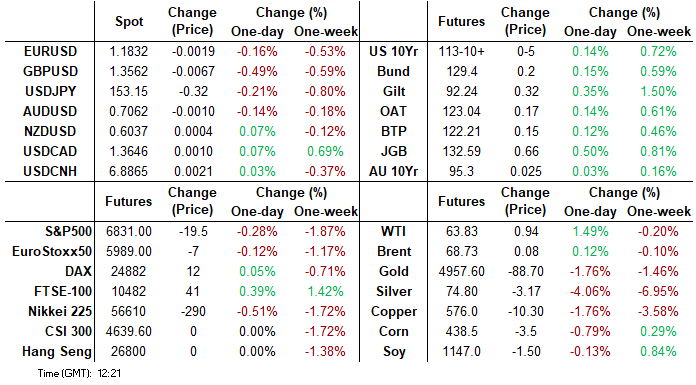

- Cash yields are 0.4-2.9bp lower across the curve, led by 30s.

- 10Y yields sits at 4.07% (-2.1bp) off an earlier low of 4.0178%, having last pushed below 4% in late November.

- TYH6 trades at 113-11 (+05+ from Friday’s settle, +03+ from yesterday’s early close) off an earlier high of 113-14, on solid cumulative volumes of ~455k (allowing for yesterday’s reasonable 489k for a US holiday).

- It more clearly breaches resistance at 113-11 (Dec 1, 2025 high) after yesterday’s 113-12, supporting an impulsive bull-wave with focus on a key 113-22+ (Nov 22, 2025 high). Before then, there could be some resistance around 113-15, roughly tallying with a 4.00% 10Y yield.

- Data: Weekly ADP (0815ET), Empire mfg Feb (0830ET), NAHB Feb (1000ET)

- Fedspeak: Goolsbee on CNBC (0830ET), Barr on AI & labor market (1245ET) and Daly on AI (1430ET) – see STIR bullet

- Bill issuance: US Tsy $89B 13W & $77B 26W bill auctions (1130ET), US Tsy $90B 6W & $50B 52W bill auctions (1300ET)

- Politics: Trump in ambassador credentialing (1400ET), Trump in policy meetings (1600ET & 1700ET)

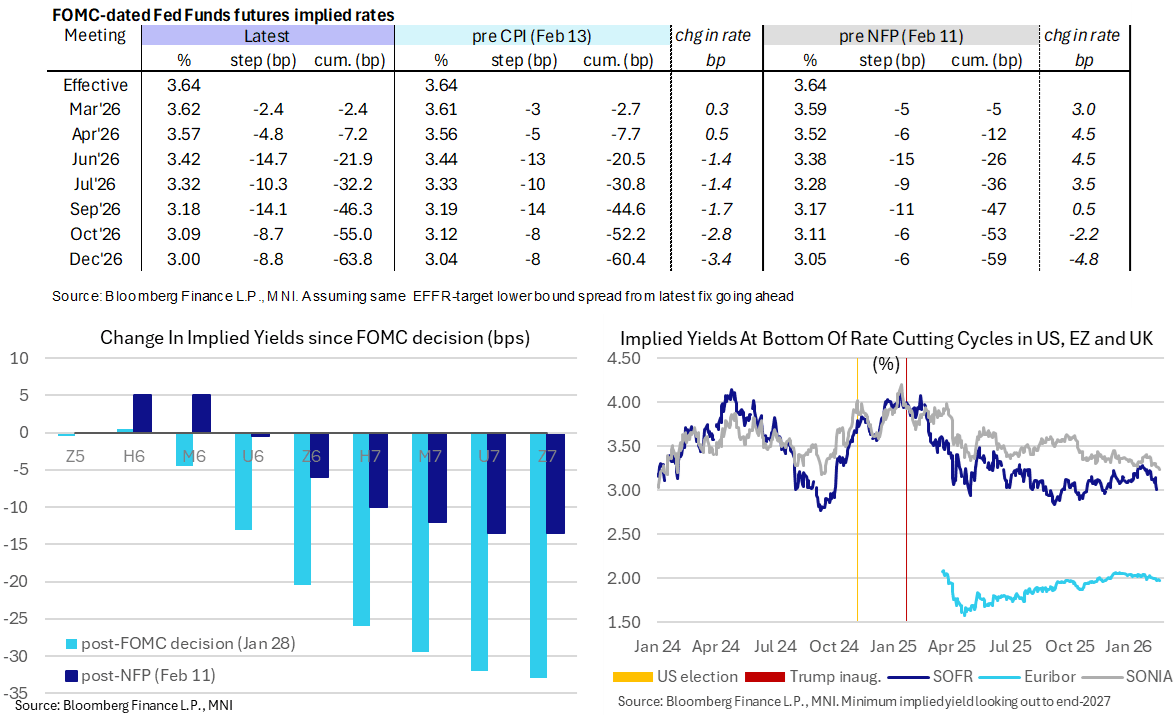

STIR: Next Fed Cuts Seen In July (But June Close) and October

- US rates have pared overnight gains but still sit at the dovish end of Friday’s range, reflecting softer-than-expected CPI for January, after little material movement through yesterday’s holiday-shortened session.

- FF cumulative cuts from 3.64% effective: 2.5bp Mar, 7bp Apr, 22bp Jun (vs 20.5bp pre-CPI), 32bp Jul, 46.5bp Sep (vs 44.5bp), 55bp Oct and 64bp Dec (vs 60.5bp).

- SOFR futures range from 1 tick lower (M6-U6) to 2 ticks firmer (U7-Z7) from Friday’s close, whilst the current terminal implied yield of 2.995% (H7, -1bp) would mark a fresh lowest close since late November if sustained today.

- Today sees data likely headlined by the weekly ADP update and is followed by three separate Fedspeakers, with first NFP and CPI comments from Barr and Daly:

- 0830ET - Chicago Fed’s Goolsbee (’27 voter) on CNBC’s squawk box. He said after Friday’s CPI report that it had some encouraging bis but also some concerns, with still pretty high services inflation. He still think it would have been wiser to wait rather than cut in December but still thinks interest rates can still go down a fair bit more.

- 1245ET – Gov. Barr (voter) in a moderated discussion on AI and the labor market. We estimate he was one of the four dots looking for one cut across 2026 back at the Dec SEP (the median view).

- 1430ET – SF Fed’s Daly (’27 voter) in a moderated discussion on AI. She told Reuters on Feb 6 that one or two more rate cuts may be needed as she sees weakness in the labor market.

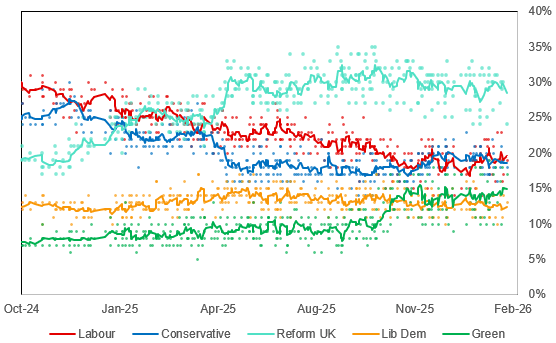

UK: Reform UK Looks To Present 'Alternative Gov't' As It Announces Shadow Roles

The right-wing populist Reform UK, which has held a consistent lead in GB-wide opinion polling for nearly a year, is unveiling a 'shadow cabinet' in an effort to present itself as an alternative gov't. The two most notable announcements are that of Robert Jenrick, MP for Newark, as 'shadow chancellor', and Richard Tice, MP for Boston and Skegness, as shadow Deputy PM and Secretary for Business, Trade, Energy and Housing.

- There may be increased market focus on the announcement, given the notable likelihood that Reform UK could win an outright majority, or at least emerge as the largest party, at the next election.

- Farage says the department under Tice will be “a new super economics and business department, in many ways modelled on what the Germans did after World War II”. Tice announces that Reform UK would set up a sovereign wealth fund, saying that he will give more details 'this time next week' at a speech in the Midlands.

- Jenrick, who joined Reform UK in January after being thrown out of the centre-right Conservatives ahead of an anticipated defection, says more details on Reform's economic policies will be forthcoming at a press conference on 18 Feb. He highlights Labour's "crazy energy policies" and tax hikes caused by a "ballooning welfare bill" as major issues, and says private sector involvement in decision making is crucial in reviving the British economy.

- Conservative defector, former Home Secretary and MP for Fareham and Waterlooville, Suella Braverman, becomes spokesperson for education, skills and equality, while Reform UK Head of Policy Zia Yusuf will serve as 'shadow home secretary', covering the immigration brief.

Chart 1. General Election Opinion Polling, % and 6-Poll Moving Average

Source: YouGov, More in Common, Opinium, Techne, Find Out Now, Freshwater Strategy, BMG, Survation, Lord Ashcroft Polling, Focaldata, JL Partners, Whitestone Insight, Deltapoll, Stonehaven, We Think, MNI

SECURITY: Kremlin Spox-'Do Not Expect News On Ukraine Talks Today'

Reuters reports comments from the Kremlin claiming that the three-way talks between Russia, Ukraine and the US "will continue tomorrow", and that "no news is expected today". It was noted earlier (see RUSSIA: New Round of Peace Talks Start Later Today in Geneva) that talks are likely to start around 06:00ET/11:00GMT/12:00CET.

- Russian state-run Tass reports that, according to a source, the talks will focus on five broad 'tracks', "These are primarily territorial, military, political, and, importantly, economic issues, as well as a wide range of security aspects". In previous rounds of talks, the main sticking point between Kyiv and Moscow has remained territorial issues over control of the occupied Donbas and areas of Zaporizhzhia and Kherson.

- State-run Interfax reports comments from the Russian Defence Ministry stating its forces had carried out a “massive strike” on Ukraine’s military-industrial and energy facilities. Al Jazeera reports "Ukraine’s air force has said Russia launched 396 drones and 29 missiles overnight, adding that it shot down 25 of the missiles and 367 of the drones. It also said four ballistic missiles and 18 drones struck 13 different targets across Ukraine." Russia claims that it shot down 151 Ukrainian drones targeting the Ilsky refinery in Krasnodar. Russian authorities also reported drone attacks in the occupied Crimea.

- The continued mass drone and missile strikes, and apparently intractable differences on territorial control, do not make for a conducive negotiating atmosphere. It remains to be seen what pressure the US can bring to bear, and whether this falls on Russia or Ukraine.

EUROPE ISSUANCE UPDATE

Croatia syndication: Guidance

- EUR Benchmark (MNI expects E1.5-2.0bln) of the new 10-year Feb-37 Croatia Eurobond. Guidance: MS+60 Area, from an earlier MS+80 IPT, Books above E6.7b.

Gilt tender results:

- GBP0.50bln of the 0.125% Jan-28 Gilt. Avg yield 3.336% (bid-to-cover 4.05x, tail 0.7bp).

- GBP0.75bln of the 4.25% Jun-32 Gilt. Avg yield 3.952% (bid-to-cover 4.17x, tail 0.1bp).

Germany auction results:

- E6bln (E4.59bln allotted) of the 2.10% Mar-28 Schatz. Avg yield 2.02% (bid-to-offer 1.36x; bid-to-cover 1.77x).

Finland auction results:

- E956mln of the 3.00% Sep-35 RFGB. Avg yield 2.99% (bid-to-cover 1.72x).

- E545mln of the 3.55% Apr-41 RFGB. Avg yield 3.425% (bid-to-cover 1.66x).

FOREX: GBP Dips to 1.3552 Following Jobs Data, DXY Firms

- A set of softer-than-expected jobs data weighed on GBP early Tuesday, with GBPUSD having a sharp move from around 1.3610 to session lows of 1.3552. Spot subsequently bounced back to 1.36 as we approached the NY crossover before a broader bid for the greenback has reemerged.

- GBPUSD's dip is deemed corrective at this juncture, with moving average studies continuing to highlight a dominant uptrend, and only a break of the 50-day EMA at 1.3531 would undermine the bull theme. Tomorrow's UK CPI print will also be very influential in driving short-term sentiment.

- The Japanese yen was the best performer across the G10 Tuesday, steadily reversing yesterday’s post GDP price action as a sources piece pointed away from a March hike and the softer risk sentiment across global markets also weighs at the margin.

- USDJPY slipped back below 153.00 in sympathy to print a 152.70 low, but remained comfortably shy of the 152.10 yearly lows. Latest dollar strength has brought the pair back to 153.15 ahead of the NY crossover. Elsewhere, a lack of renewed optimism for the Euro has been weighing on EURJPY, prompting fresh two-month lows below 181.00 this morning, meaning the cross is testing key support at 181.22.

- The next key event for JPY may be PM Takaichi's general policy speech on Friday, which is reported to include a multi-year special budget for investment into growth initiatives and crisis management.

- NZD is slightly stronger ahead of Wednesday’s RBNZ decision, the first for newly appointed Governor Breman. Any hawkish lean would place the 0.6093 NZDUSD cycle highs back in focus.

- Fed's Barr and Daly will be interesting to watch as they speak on AI today. ECB's Escriva and Makhlouf are also scheduled to appear. In terms of data, Canada CPI for January takes focus, while Japanese trade data is scheduled overnight ahead of the RBNZ.

NZD: RBNZ Decision Due Wednesday, Breman Tone in Focus

- Following the topside break of 0.5850 in late January, NZDUSD has seen solid upside momentum resulting in a 0.6093 cycle high posted on Jan 29. Corrective price action took the pair back below 0.60 momentarily, with 20-day EMA support being very well respected on Feb 06.

- Over the last week, we have been oscillating around 0.6050, keeping spot within touching distance of 0.6120, a break of which would place the pair at the highest point since October 2024.

- The RBNZ is firmly expected to leave the OCR at 2.25% on Wednesday (preview here: https://mni.marketnews.com/4qMgc7r ), leaving initial attention on the details of the central bank’s new OCR path. The focus will then turn to gauging Governor Breman’s tone, as this will be her first rate setting meeting in charge.

- Any hawkish lean to tomorrow’s decision would place the NZDUSD cycle highs back in focus, while bearish momentum for GBPNZD has been dominating since mid-Jan, with the cross slipping back below 2.25 in recent trade and approaching 2.2456 cycle lows.

- On the other hand, should the board opt for a more cautious stance, perhaps pointing to the latest uptick in the unemployment rate, AUDNZD remains the prime candidate to benefit. This follows last week’s extension to 1.1807, fresh highs since July 2013.

AUDUSD Consolidates Near 6% Gains This Year, Employment Data Thursday

- AUDUSD has traded within relatively tight ranges over the past three sessions, with 0.7050/0.7100 broadly capping the price action, allowing the pair to consolidate near-6% gains this year. Fresh cycle highs at 0.7147 last week reinforce the dominant medium-term uptrend, with spot trading to within 11 pips of the 2023 peak at 0.7158.

- CFTC data shows leveraged funds continued to add to their AUD longs, and how risk holds up when the US returns today will be a key factor driving short-term Aussie sentiment. On the downside, initial key support lies at 0.6897, the Feb 6 low.

- In line with most recent rhetoric, the latest release of the RBA minutes showed that board members judged inflation remained too high, with underlying price pressures running above the central projection from six months earlier, a key factor behind the decision to lift the cash rate 25bps to 3.85% in Feb.

- Q4 Wage Cost Index data is scheduled Wednesday in Australia, however, there will be greater focus on employment figures due Thursday where the unemployment rate is expected to tick up to 4.2% in January. The minutes said downside risks to full employment had eased, with resilient jobs growth, only gradual wages moderation and high unit labour costs signalling ongoing labour market tightness.

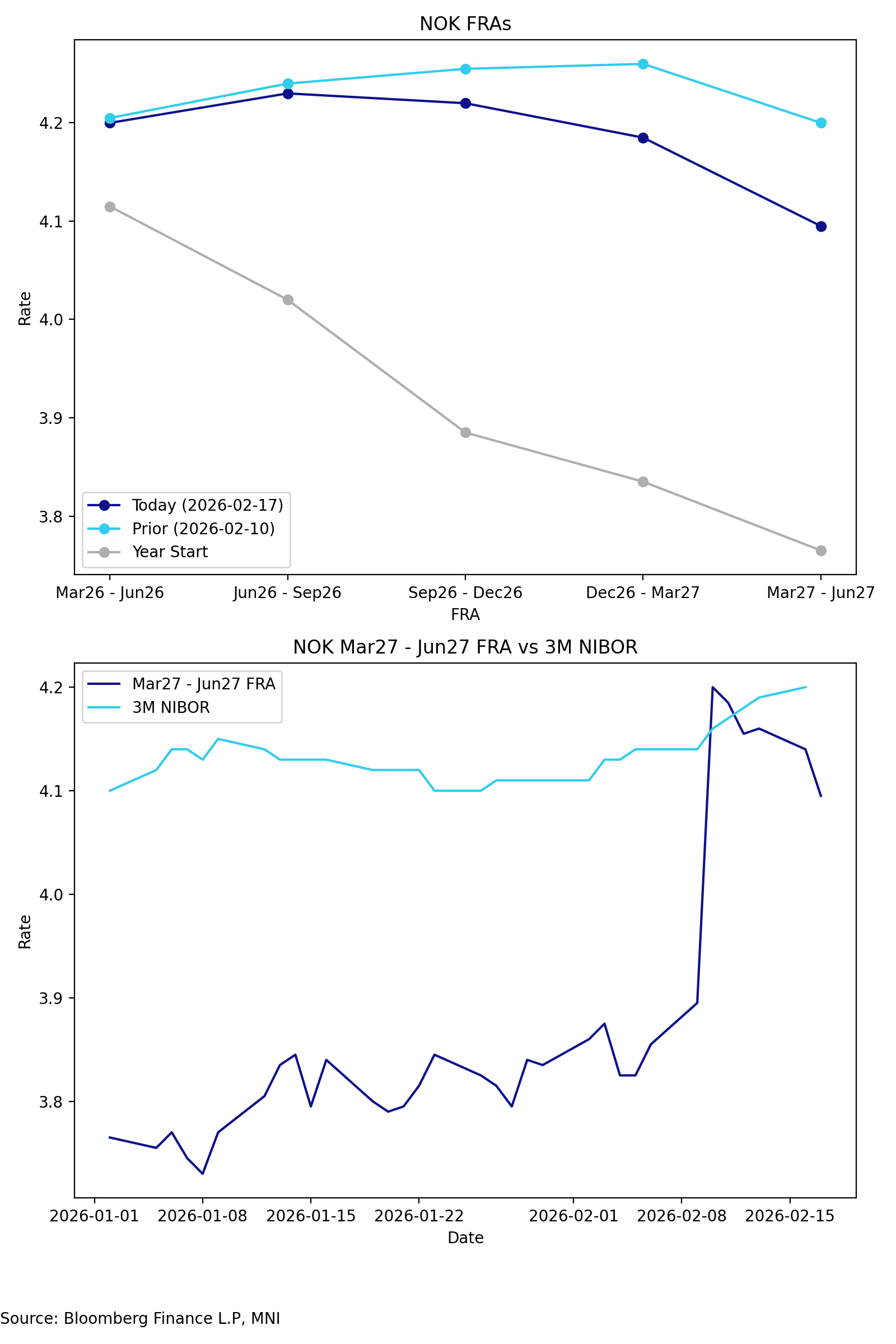

NORWAY: Front-end Rates Moderate From Last Week's Extremes, FX Spillover Limited

NOK rates have moved away from last week’s hawkish extremes, which came in the wake of the firmer-than-expected January inflation report. 2-year swap rates are now back at 4.25%, down from a high of ~4.37% last Wednesday.

- Meanwhile, the Mar27-Jun27 FRA is at 4.095%, off last week’s 4.265% high and down 4.5bps on the session. The contract is now back below yesterday's 4.20% 3M NIBOR fixing.

- Last week, we noted that moves in rates seemed a little excessive. Although a no-cut scenario for 2026 should not be underappreciated, we still think it's reasonable to expect one cut later this year (i.e. in H2), given nominal rates are still restrictive at current levels and the krone is much stronger than previously assumed.

- A reminder that ahead of Norges Bank's March 26 decision, there is still another inflation report, more labour market data, information on wage bargaining negotiations and the Q1 Regional Network Survey to be released. These will be important MPR rate path inputs.

- Despite the dovish moves in NOK rates today, krone resilience has persisted, particularly versus SEK (which underperforms the G10 basket in its own right). Bullish conditions in NOKSEK (+0.43% at 0.9449) remain dominant, with the cross building on the recent piercing of trendline resistance drawn from the 2022 highs. The next main topside target is seen at 0.95.

OPTIONS: Expiries for Feb17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E614mln), $1.1850(E614mln), $1.1900(E1.2bln), $1.1920-25(E779mln), $1.2000(E769mln), $1.2025(E615mln)

- USD/JPY: Y152.50($717mln), Y156.00($1.9bln)

- USD/CAD: C$1.3600($1.1bln), C$1.3625($911mln)

EQUITIES: Bearish Threat for E-Mini S&P Remains Present, Key Support at 6751.50

- The medium-term trend condition in EuroStoxx 50 futures is unchanged, it remains bullish and the latest pullback appears corrective - for now. The contract has pierced the 6100.00 handle. A clear breach of this hurdle would open 6134.00, a Fibonacci projection point. Key support to watch lies at the 50-day EMA, at 5908.77. Clearance of this average would highlight a short-term top.

- A sharp sell-off on Feb 12 in S&P E-Minis reinstates a potential bearish threat leaving key resistance at 7043.00, the Jan 28 high and bull trigger, intact for now. Attention turns to the key support at 6751.50, the Feb 6 low, where a break would highlight a top and a stronger short-term reversal. This would open 6691.56, a Fibonacci retracement point. Initial resistance to watch is at 6919.38, the 50-day EMA.

COMMODITIES: WTI Futures Test 20-Day EMA Support Again, Bull Cycle Intact

- A bull cycle in WTI futures remains intact. However, the move lower from the Jan 29 high continues to highlight a corrective phase. Attention is on support at the 20-day EMA, at $62.61 (pierced). The 50-day EMA lies at $60.95. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high. Clearance of it would resume the uptrend.

- Recent gains in Gold highlight a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sell from the Jan 29 high continues to highlight a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent overbought condition. A resumption of bearish activity would refocus attention on $4403.0, Feb 2 low.

| Date | GMT/Local | Impact | Country | Event |

| 17/02/2026 | - | ECB de Guindos at ECOFIN Meeting | ||

| 17/02/2026 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/02/2026 | 1330/0830 | ** | Wholesale Trade | |

| 17/02/2026 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 17/02/2026 | 1330/0830 | *** | CPI | |

| 17/02/2026 | 1500/1000 | ** | NAHB Home Builder Index | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 17/02/2026 | 1745/1245 | Fed Governor Michael Barr | ||

| 17/02/2026 | 1800/1300 | ** | US Treasury Auction Result for 52 Week Bill | |

| 17/02/2026 | 1930/1430 | San Francisco Fed's Mary Daly | ||

| 18/02/2026 | - | Reserve Bank of New Zealand Meeting | ||

| 18/02/2026 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 18/02/2026 | 0030/1130 | *** | Quarterly wage price index | |

| 18/02/2026 | 0100/1400 | *** | RBNZ official cash rate decision | |

| 18/02/2026 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 18/02/2026 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 18/02/2026 | 0700/0700 | *** | Producer Prices | |

| 18/02/2026 | 0745/0845 | *** | HICP (f) | |

| 18/02/2026 | 0900/1000 | ECB Cipollone at ABI's Executive Committee Meeting | ||

| 18/02/2026 | 1000/0500 | * | CREA Existing Home Sales | |

| 18/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 18/02/2026 | 1330/0830 | *** | Housing Starts | |

| 18/02/2026 | 1330/0830 | *** | Housing Starts | |

| 18/02/2026 | 1330/0830 | ** | Durable Goods New Orders | |

| 18/02/2026 | 1330/0830 | ** | Durable Goods New Orders | |

| 18/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 18/02/2026 | 1415/0915 | *** | Industrial Production | |

| 18/02/2026 | 1700/1800 | ECB Schnabel Panel at Berlin-Brandenburg Academy of Sciences and Humanities | ||

| 18/02/2026 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 18/02/2026 | 1800/1300 | Fed's Michelle Bowman | ||

| 18/02/2026 | 1900/1400 | *** | FOMC Minutes | |

| 18/02/2026 | 2100/1600 | ** | TICS | |

| 19/02/2026 | 2350/0850 | * | Machinery orders |