MNI US MARKETS ANALYSIS - Tsy Support, Gov Shutdown in Focus

Highlights:

- First phase of votes to end the government shutdown expected to pass, but too late to save data delays

- AUD on front-foot as RBA hike rates and markets expect more to come

- Treasury key support in focus follows Monday's reversal off highs

US: Vote To End US Govt Shutdown Expected Today

The House of Representatives is expected to vote later today on a five-bill government funding package and a two-week Continuing Resolution for the Department of Homeland Security. The measure is expected to pass, ending a short government shutdown triggered at midnight on Friday when funding for six US federal government departments lapsed.

- While there may be some last-minute complications, the most significant roadblocks to the package were cleared yesterday. The House Rules Committee voted to discharge the measure to the floor.

- Conservative Republican Reps Anna Paulina Luna (R-FL) and Tim Burchett (R-TN) dropped a blockade after a White House meeting with President Donald Trump, suggesting the GOP is now positioned to approve the 'rule' to advance the package to a final vote. (The minority party rarely supports the initial rule vote, even if they intend to vote in favour of final passage)

- Trump wrote on Truth Social yesterday, “I hope all Republicans and Democrats will join me in supporting this Bill, and send it to my desk WITHOUT DELAY. There can be NO CHANGES at this time.”

- The most senior House Democratic appropriator, Rosa DeLauro (D-CT), said she will support the package because "it gives us time and gives us leverage to secure the protections that we need for our communities…”

- DeLauro’s comments suggest there is likely to be a sizable contingent of Democrats prepared to back the measure, despite an informal whip from House Minority Leader Hakeem Jeffries (D-NY) against the package.

US: First Procedural Vote On Govt Funding Package Expected At 11:15 ET 16:15 GMT

Politico reports that the House of Representives will vote on the rule for the five-bill government funding package and DHS spending patch at 11:15 ET 16:15 GMT, with a final vote tentatively scheduled for 13:00 ET 18:00 GMT.

- The rule vote is trickiest part of the process for House Speaker Mike Johnson (R-LA) as it is not likely to receive any Democrat support. The Republican majority provides just a single-vote cushion if all members are present and voting, after Johnson yesterday swore-in Deocratic Rep Christian Menefee (D-TX), who won a Special Election on Saturday.

- However, as noted in previous bullet (US: Vote To End US Govt Shutdown Expected Today) two Republican hardliners signalled yesterday they would back the rule, after meeting with President Trump at the White House.

- If the rule passes, and the measure will advances to a final vote, there is likely to be a contingent of Democrat votes to offset any Republican defections.

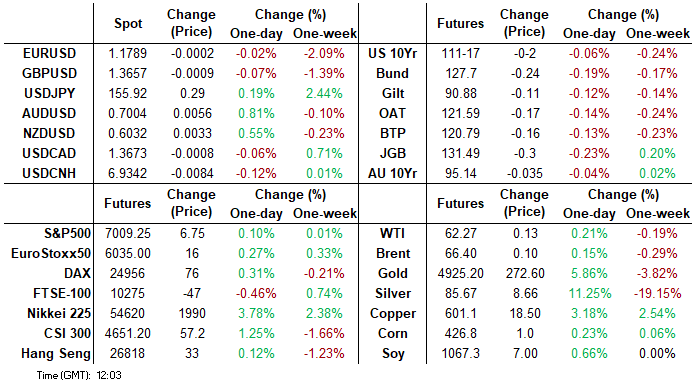

US TSYS: Renewed Attention On TYH6 Bear Trigger, Shutdown-Ending Votes In Focus

Treasuries have extended a little lower overnight after yesterday’s losses seen on a firmer-than-expected ISM mfg report along with 8-part supply from Oracle and block sales. Today should see attention on House votes to end the partial government shutdown, with a likely tight rule vote at 1115ET needing to be cleared first.

- Cash yields are 0.4-0.9bp higher across the curve.

- 10Y yields at 4.283% (+0.6bp) have seen a high of 4.2915%, challenging the January and the September high circa 4.3065%.

- TYH6 trades at 111-17 (-02) as it holds close to earlier lows of 111-15, on reasonable cumulative overnight volumes of 330k.

- Yesterday’s price action helped support the view that prior gains were corrective, whilst today’s earlier low of 111-15 tested brief support at 111-15+ (Jan 28 low). It sees renewed attention on the bear trigger at 111-09 (Jan 20 low) before 111-01+ in what equates to 4.3511% for 10Y yields today if there is clearance of the 4.30% area.

- Data: Weekly Johnson Redbook (0855ET), Wards vehicle sales

- Fedspeak: Barkin on economy (0800ET), VC Supervision Bowman in moderated discussion (0940ET) – see STIR

- Bill issuance: US Tsy $90B 6W bill auction (1130ET)

- Shutdown: House vote on rule for five-bill government funding package and DHS spending patch (1115ET) before final vote tentatively scheduled for 1300ET.

- Politics: Trump meets with President of Colombia (1100ET), Trump in signing time (1400ET)

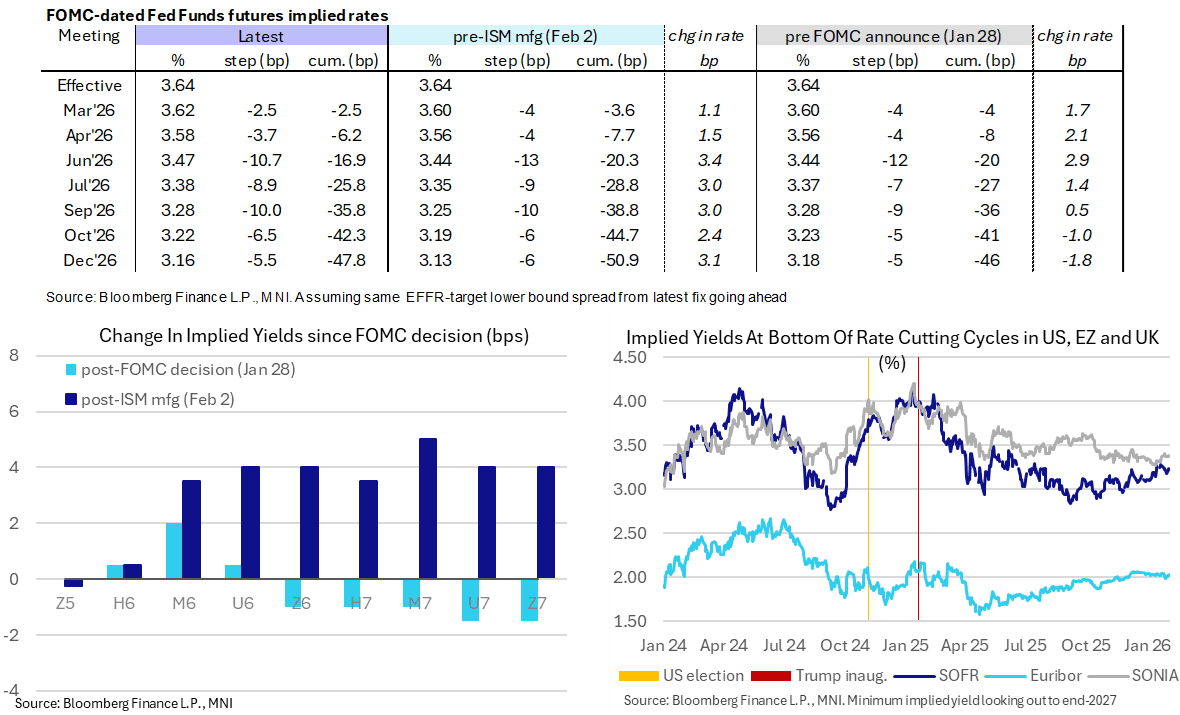

STIR: Next Fed Cut Increasingly Seen In July, No JOLTS Today

- US rates increasingly eye a next Fed cut not until July as they modestly extended yesterday’s hawkish shift with its added tailwind from a surprisingly strong ISM manufacturing report.

- FF cumulative cuts from 3.64% effective: 2.5bp Mar, 6bp Apr, 17bp Jun, 26bp Jul, 36bp Sep, 42.5bp Oct and 48bp Dec.

- SOFR futures are 0.5-2 ticks lower looking out to end-2027, with the terminal implied yield of 3.235% (Z6, +1.5bp) nudging a little closer to Jan 22's 3.285% highest close since July.

- There won’t be a JOLTS report today and the BLS has said it won’t release a NFP report on Friday regardless of how quickly the partial government shutdown is resolved.

- That sees today’s data confined to retail sales indicators with the weekly Johnson Redbook report at 0855ET before Wards vehicle sales.

- Fedspeak from Richmond Fed’s Barkin (’27 voter) on the US economy at 0800ET (text + Q&A), who on Jan 15 described AI and the rich as the two engines for today’s economy whilst saying it’s hard to put weight on data from the past three months. He’s followed by VC Supervision Bowman (voter) in a WSJ moderated discussion at 0940ET (text tbd), with the exact topic unknown but the conference focused on capital markets and the future of global finance.

SOFR: Short Setting Dominates In Futures On Monday

OI data points to net short setting dominating through the blues on Monday, with only 3 instances of net long cover seen across the front 4 contracts. Firmer-than-expected ISM manufacturing data drove much of the hawkish shift in pricing.

| 02-Feb-26 | 30-Jan-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,403,701 | 1,362,255 | +41,446 | Whites | +125,769 |

SFRH6 | 1,438,688 | 1,424,858 | +13,830 | Reds | +50,480 |

SFRM6 | 1,456,020 | 1,416,993 | +39,027 | Greens | +3,945 |

SFRU6 | 1,482,557 | 1,451,091 | +31,466 | Blues | +10,785 |

SFRZ6 | 1,418,518 | 1,410,227 | +8,291 |

|

|

SFRH7 | 1,060,600 | 1,045,823 | +14,777 |

|

|

SFRM7 | 871,516 | 857,481 | +14,035 |

|

|

SFRU7 | 841,233 | 827,856 | +13,377 |

|

|

SFRZ7 | 860,819 | 861,383 | -564 |

|

|

SFRH8 | 522,731 | 516,715 | +6,016 |

|

|

SFRM8 | 440,425 | 437,241 | +3,184 |

|

|

SFRU8 | 396,491 | 401,182 | -4,691 |

|

|

SFRZ8 | 395,088 | 382,604 | +12,484 |

|

|

SFRH9 | 216,524 | 220,934 | -4,410 |

|

|

SFRM9 | 209,590 | 208,231 | +1,359 |

|

|

SFRU9 | 172,574 | 171,222 | +1,352 |

|

|

US TSY FUTURES: Mix Of Net Short Setting & Long Cover On Monday

OI data points to a mix of net short setting (TU, FV & WN) and long cover (TY, UXY & US) as Tsy futures ticked lower on Monday, with the firmer-than-expected ISM manufacturing survey providing much of the selling pressure seen in NY hours, while the presence of 8-part supply from Oracle and block sales also weighed.

- Net short setting in the extremities of the curve provided the dominant positioning input on the day.

| 02-Feb-26 | 30-Jan-26 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,658,645 | 4,616,039 | +42,606 | +1,580,378 |

FV | 6,876,339 | 6,847,817 | +28,522 | +1,220,960 |

TY | 5,545,576 | 5,559,927 | -14,351 | -939,188 |

UXY | 2,605,214 | 2,612,395 | -7,181 | -634,956 |

US | 1,728,553 | 1,740,277 | -11,724 | -1,597,456 |

WN | 2,194,534 | 2,175,916 | +18,618 | +3,356,013 |

|

| Total | +56,490 | +2,985,750 |

EUROPE ISSUANCE UPDATE:

Belgium syndication: 30-year Jun-56 OLO mandate

- "The Kingdom of Belgium intends to issue a new EURO syndicated benchmark bond maturing 22 June 2056 (OLO 107) in the near future, subject to market conditions."

- We had pencilled this in for next week (post-ECB) rather than this week. A 20/30-year OLO had been expected (see our expectations in the MNI EGB Issuance Deep Dive), so this is not a huge surprise to us.

- We look for a E4-6bln transaction size (probably the bottom half of the range most likely given that this is a 30-year OLO).

Italy Syndication: Final terms

- E14bln (MNI expected E10-13bln, so this is larger than we thought) of the new 15-year Oct-41 BTP. Books in excess of E157bln, spread set at BTPS 3.85 Oct-40 + 8 bps (guidance was 3.85% Oct-40 BTP +10bps area).

- E14bln matches the largest ever single line Italian syndication (although there have been larger dual-tranche deals).

- E157bln is also the largest ever book for a single Italian line.

ESM syndication: Final terms

- E2.5bln (midpoint of MNI's expected range of E2-3bln) of the new 10-year Feb-36 ESM. Books in excess of E23.8bln, spread set at MS+18bps (guidance was MS + 21bps area).

11:39:40

Belgium syndication: 30-year Jun-56 OLO mandate - "The Kingdom of Belgium intends to issue a new EURO syndicated benchmark bond maturing 22 June 2056 (OLO 107) in the near future, subject to market conditions."

- We had pencilled this in for next week (post-ECB) rather than this week. A 20/30-year OLO had been expected (see our expectations in the MNI EGB Issuance Deep Dive), so this is not a huge surprise to us.

- We look for a E4-6bln transaction size (probably the bottom half of the range most likely given that this is a 30-year OLO).

Italy Syndication: Final terms

- E14bln (MNI expected E10-13bln, so this is larger than we thought) of the new 15-year Oct-41 BTP. Books in excess of E157bln, spread set at BTPS 3.85 Oct-40 + 8 bps (guidance was 3.85% Oct-40 BTP +10bps area).

- E14bln matches the largest ever single line Italian syndication (although there have been larger dual-tranche deals).

- E157bln is also the largest ever book for a single Italian line.

ESM syndication: Final terms

- E2.5bln (midpoint of MNI's expected range of E2-3bln) of the new 10-year Feb-36 ESM. Books in excess of E23.8bln, spread set at MS+18bps (guidance was MS + 21bps area).

UK auction results

- Decent gilt auction with solid bid-to-cover and the LAP (lowest accepted price) coming in higher than any time in the last 45 minutes of the bidding window.

- Following the results the 4.75% Oct-35 gilt has hit a new intraday high (currently 101.292 at writing) and helped to pull gilt futures around 7 ticks higher.

- GBP4.25bln of the 4.75% Oct-35 Gilt. Avg yield 4.585% (bid-to-cover 3.63x, tail 0.2bp).

Germany green auction results

- E1.5bln (E1.354bln allotted) of the 2.50% Feb-35 Green Bund. Avg yield 2.79% (bid-to-offer 1.81x; bid-to-cover 2.01x).

CHINA: Fix Behaviour Endorses CNY Appreciation - But Only At Acceptable Pace

USDCNH's 6.9309 print overnight was the lowest since May 2023, with offshore losses matching the pressure seen onshore as the December trend extends well into this year to set up for currency strength into the Lunar New Year holidays.

- The fixing strategy should be watched carefully here - China's Lunar New Year is not set to start until February 17th, but the authorities commonly manage liquidity and market rates well ahead of the extended break - with fix management a key tool to manage conditions.

- Markets had clearly anticipated a slower decline in the USDCNY fix given the USD bounce, but that hasn't been the case. The fix error term (confirmed fix minus expected fix) averaged ~240 pips across December and January, but is now close to zero. This suggests markets are becoming more settled with the view that USDCNY can continue to depreciate, but only at a pace of their choosing.

- On the FX rate, TD Securities write that their year-end forecast of 6.70 in USDCNY could be hit by the end of H1, and as such the PBOC are expected to adjust their "structural FX parameters" should CNY undergo sudden appreciation. They conclude that these tweaks to slow gains may come after the new year.

- In rates markets, pre-issuance liquidity support is already evident in today's announcement of CNY800bln in 3m outright reverse repo - effectively ensuring steady and "ample" banking system liquidity ahead of this week's CNY282bln in bond sales.

FOREX: RBA and Risk Sentiment Providing Key AUD Tailwinds

- AUD is the main outperformer of the day, rising more than 1% against the US dollar after the hawkish hike from the RBA overnight, AUDUSD is also supported by risk sentiment following yesterday's blockbuster ISM Manufacturing, leading to e-mini S&P futures rallying back above the 7000 mark.

- Supply and demand are slightly out of balance and monetary policy is likely a bit loose, driving inflation over the past two quarters, RBA Governor Bullock said on Tuesday after a unanimous decision to raise the cash rate by 25bp to 3.85%.

- Most of the big 4 Australian Banks look for a May hike from the RBA. ANZ are the dovish exception, looking for the cash rate to remain on hold through '26.

- From a risk standpoint, the picture looks quite favourable with NATO turmoil on the backburner for now, Warsh being perceived as a sensible Fed Chair, US fiscal being supportive, growth expectations brightening, and the government shutdown seen to resolve soon. The constructive Aussie backdrop has led AUDJPY to pierce key resistance of the 2024 highs of 109.37, placing the cross at its highest level since 1991.

- Overall for AUDUSD, the pullback between Jan 29 - Feb 2 continues to highlight the start of a corrective phase, which would confirm an unwinding of the recent overbought trend condition. Short-term technical parameters of 0.7094 (cycle highs) and 0.6846 (20-day EMA) appear well defined.

FOREX: AUDJPY Highest Since 1990 on Hawkish RBA / Buoyant Risk

- AUD is the main outperformer of the day following the hawkish hike by the RBA overnight. AUDUSD (+0.8%) price action has been supported by risk sentiment following yesterday's blockbuster ISM Manufacturing, leading to e-mini S&P futures rallying back above the 7000 mark. While AUDUSD has rallied back above 0.70, spot remains well shy of the 0.7094 cycle highs.

- From a fundamental perspective, the picture looks quite favourable with NATO turmoil on the backburner for now, Warsh being perceived as a sensible Fed Chair, US fiscal being supportive, growth expectations brightening, and the government shutdown seen to resolve soon. This supports the current strength in high-beta currencies, supportive for the likes of AUD, NZD and EMFX.

- The recent sharp USDJPY selloff continues to be eroded, with the pair now recovering more than 50% of the January pullback. Price action has led USDJPY to breach the 50-day EMA intersecting at 155.75. AUDJPY meanwhile pierced key resistance of the 2024 highs of 109.37, placing the cross at its highest level since 1990.

- Opinion polls suggest PM Takaichi may be successful in securing her power in the February 23 snap elections, which would enable her to proceed with fiscal easing, while Finance Minister Katayama reiterated the MoF will keep close communication with the US about the currency markets.

- While the US is expected to vote later today on a bill ending the government shutdown, BLS data releases are on hold, including today's JOLTS release and Friday’s payrolls report. This may allow markets to soon focus on BoE and ECB decisions scheduled on Thursday.

OPTIONS: Expiries for Feb03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1850(E3.5bln), $1.1935-40(E2.5bln)

- USD/JPY: Y155.75($877mln)

- GBP/USD: $1.3200(Gbp835mln)

- USD/CAD: C$1.3590-00($913mln)

EQUITIES: This Week's Gains Reinforce Bullish E-Mini S&P Theme

- A bull cycle in Eurostoxx 50 futures remains intact and Monday’s rally reinforces this theme. Key support to monitor lies at the 50-day EMA at 5857.60. A clear breach of this average would signal scope for a deeper retracement. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on the key resistance and bull trigger at 6072.00, the Jan 14 / 15 high.

- The trend in S&P E-Minis is bullish and Monday’s strong gains reinforce this theme. The move higher also suggests that the recent bear threat merely resulted in a short lived correction. Attention is on key resistance and the bull trigger at 7043.00, the Jan 28 high. A break of this level would confirm a resumption of the primary uptrend and open 7080.92, a Fibonacci projection. Key support and a bear trigger has been defined at 6814.50, the Jan 21 low.

COMMODITIES: Gold Extends Recovery From Monday's Low to Over 10%

- A bull cycle in WTI futures remains intact. However, Monday’s impulsive sell-off highlights the beginning of a corrective phase. Attention is on support at the 20-day EMA, at $61.01. The 50-day EMA lies at $59.74. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high.

- Gold has recovered from Monday’s low. However, the sharp sell-off from last week’s high still highlights a potential top in the L/T trend and from a S/T perspective, marks an unwinding of the recent extreme overbought condition. The metal has pierced the 50-day EMA, at $4551.2. A clear break of this average would signal scope for a deeper retracement and open $4274.7, the Dec 31 ‘25 low. Initial resistance is 4999.2, a Fibonacci retracement.

| Date | GMT/Local | Impact | Country | Event |

| 03/02/2026 | 1300/0800 | Richmond Fed's Tom Barkin | ||

| 03/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 04/02/2026 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 04/02/2026 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 04/02/2026 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 04/02/2026 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 04/02/2026 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 04/02/2026 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 04/02/2026 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 04/02/2026 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 04/02/2026 | 0830/0930 | Riksbank Minutes | ||

| 04/02/2026 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 04/02/2026 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 04/02/2026 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 04/02/2026 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 04/02/2026 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 04/02/2026 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 04/02/2026 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 04/02/2026 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 04/02/2026 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 04/02/2026 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 04/02/2026 | 1000/1100 | ** | EZ PPI | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash (2dp) | |

| 04/02/2026 | 1000/1100 | *** | Italy Flash Inflation | |

| 04/02/2026 | 1000/1100 | *** | HICP (p) | |

| 04/02/2026 | 1000/1100 | *** | Italy Flash Inflation | |

| 04/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 04/02/2026 | 1315/0815 | *** | ADP Employment Report | |

| 04/02/2026 | 1330/0830 | *** | Treasury Quarterly Refunding | |

| 04/02/2026 | 1445/0945 | *** | S&P Global Services Index (final) | |

| 04/02/2026 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 04/02/2026 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 04/02/2026 | 1500/1000 | Treasury Secretary Scott Bessent | ||

| 04/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 04/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 04/02/2026 | 1700/1200 | Richmond Fed's Tom Barkin | ||

| 04/02/2026 | 2330/1830 | Fed Governor Lisa Cook |