MNI US MARKETS ANALYSIS - Terminal Fed Yld Highest Since July

Highlights:

- Downdraft in global rates futures holds, US 5y yield close to multi-month high as FOMC meeting begins

- Crucial French parliamentary vote on a knife edge

- AUD trades well on RBA hawkish hold

US TSYS: Twist Flatter; Labor Data & 10Y Supply Ahead As Fed Looms Large

Treasuries are mildly twist flatter in moves that broadly consolidate yesterday’s continued sell-off on global factors. Tomorrow’s FOMC decision looms large, expected to show signs of a divided committee, whilst today sees further labor data updates plus 10Y supply.

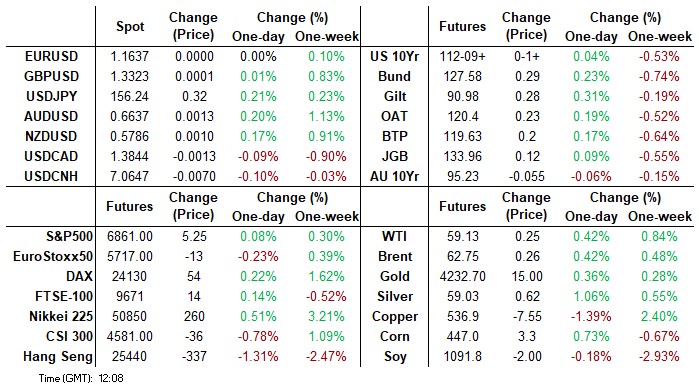

- Cash yields range from 0.6bp lower (30s) to 0.6bp higher (3s).

- TYH6 trades at 112-09+ (+ 01+) on reasonable overnight volumes of 315k, keeping within yesterday’s range which saw a fresh low of 112-02+.

- Having breached the bear trigger at 112-07 (Nov 5 high), sights are set for a move towards 112-00 (Fibo projection) after which would open 111-19. To the upside, initial firm resistance is seen at 112-28 (20-day EMA).

- Data: Weekly ADP (0815ET), Redbook retail sales (0855ET), JOLTS Sep & Oct (1000ET), KC Fed LCMI (1000ET), Conference Board Leading index Sep (1000ET)

- Coupon issuance: US Tsy $39B 10Y Note re-open - 91282CPJ4 (1300ET). Last month’s 10Y tailed by 0.6bp and saw mixed peripheral statistics including its lowest bid-to-cover since August.

- Bill issuance: US Tsy $75B 6W bill auction (1130ET)

- Politics: Trump attends VP Vance’s Christmas reception (1515ET), Trump delivers remarks on economy (1810ET)

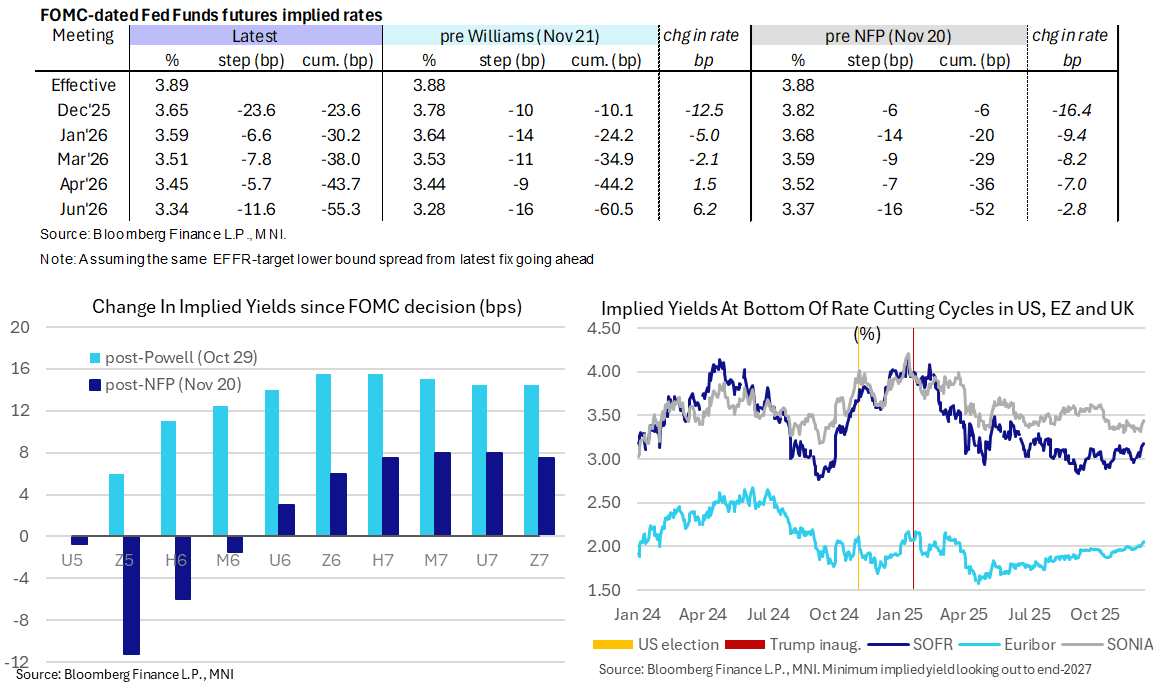

STIR: Terminal Fed Yield Highest Since July Day Out From FOMC Decision

- Fed Funds implied rates are unchanged on the day, broadly set up for a hawkish Fed cut tomorrow with 23.5bp of cuts priced but then a next fully priced cut not seen until June.

- Today labor data in focus, with the return of weekly ADP tracking after the full monthly report last week before two months of JOLTS data later.

- Cumulative cuts from 3.89% effective: 23.5bp Dec, 30bp Jan, 38bp Mar, 43.5bp Apr and 55.5bp Jun.

- SOFR futures have pared earlier losses and are mostly 0.5-1 tick firmer today looking out to end-2027. It consolidates a sizeable hawkish shift further out the curve in the past three working days, with the implied terminal yield at 3.175% (H7) after yesterday’s 3.18% was the highest close since July.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Dec2025_With_Analysts_4d5a318a2b.pdf

SOFR: Short Setting In The Red Futures Pack Most Prominent On Monday

OI data points to a mix of net short setting and long cover as most SOFR futures ticked lower on Monday, largely driven by spillover from the latest round of hawkish repricing in the EUR short end.

- It is hard to make any real inference across the front 3 contracts, as they settled at unchanged levels.

- The most meaningful net positioning swing (based on net pack OI movement) came via net short setting in the reds.

| 08-Dec-25 | 05-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,302,542 | 1,294,451 | +8,091 | Whites | -34,366 |

SFRZ5 | 1,542,700 | 1,599,027 | -56,327 | Reds | +91,006 |

SFRH6 | 1,446,250 | 1,421,074 | +25,176 | Greens | -29,942 |

SFRM6 | 1,136,256 | 1,147,562 | -11,306 | Blues | +11,808 |

SFRU6 | 1,121,979 | 1,081,490 | +40,489 |

|

|

SFRZ6 | 1,124,600 | 1,105,364 | +19,236 |

|

|

SFRH7 | 861,456 | 844,189 | +17,267 |

|

|

SFRM7 | 784,563 | 770,549 | +14,014 |

|

|

SFRU7 | 799,595 | 829,329 | -29,734 |

|

|

SFRZ7 | 846,149 | 850,262 | -4,113 |

|

|

SFRH8 | 445,354 | 446,954 | -1,600 |

|

|

SFRM8 | 409,622 | 404,117 | +5,505 |

|

|

SFRU8 | 379,105 | 380,155 | -1,050 |

|

|

SFRZ8 | 337,752 | 320,365 | +17,387 |

|

|

SFRH9 | 200,276 | 201,582 | -1,306 |

|

|

SFRM9 | 212,106 | 215,329 | -3,223 |

|

|

FRANCE: Today's Crucial National Assembly Vote Remains On A Knife Edge

The French National Assembly will vote on the 2026 Social Security budget today. The Parliamentary session begins at 1400GMT/1500CET, but the exact timing of the vote is uncertain. The outcome of today’s vote is crucial to the progress of overall budget negotiations (the State budget is currently being reviewed by the Senate), and by extension OAT performance. Downside in the 10-year OAT/Bund spread continues to be contained by the 70bp figure for now. If the Social Security bill passes, it will increase hopes that the Government will be able to get a full-budget passed by year-end and reduce immediate-term political uncertainty – likely allowing some more risk premium to be removed from French bonds.

- The revenue section of the Social Security budget was passed on Friday, but this was in part due to several absentees from the far-right RN – who are unambiguously opposed to the bill.

- The far-left La France Insoumise also oppose the bill, while the Socialists are expected to vote in favour following guidance from First Secretary Faure yesterday.

- The intentions of the conservative Les Republicains, the centre-right Horizons and the Ecologists will be key.

- The Ecologists voted against the Revenue section on Friday (in part due to a lack of support for healthcare workers), but the Government has attempted to make concessions in recent days in the hope they will now opt to abstain. This morning, Cyrielle Châtelain, MP for Isère and president of the Ecologists told RMC radio that "abstention is an option", but that "we will not vote for it because this budget is deeply unbalanced".

- The 2026 Social Security budget being voted on today projects a deficit of E19.6bln. That’s above the E17.6bln initially targeted by the Government but below the ~E30bln deficit that would be implied if the current budget is rolled over.

US-CHINA: FT Reports That China May Restrict Access To H200 Chips

The FT reports that China may restrict access to Nvidia’s H200 chips despite approval for shipment from US President Trump yesterday. A brief downtick in equity futures is noted around the timing of the story, but the move lacks traction for now. Some highlights from the story:

- "Beijing is set to limit access to Nvidia’s advanced H200 chips despite Donald Trump’s decision to allow the export of the technology to China as it pushes to achieve self-sufficiency in semiconductor production."

- "According to two people with knowledge of the matter, regulators in Beijing have been discussing ways to permit limited access to the H200, Nvidia’s second-best generation of artificial intelligence chips."

- "Buyers would probably be required to go through an approval process, the people said, submitting requests to purchase the chips and explaining why domestic providers were unable to meet their needs."

- "No final decision had been made yet, the people added."

EUROPE ISSUANCE UPDATE

Ireland NTMA 2026 funding plan

- The NTMA has announced that it plans to issued E10-14bln of bonds with one syndication in 2026. This is a bit higher than expected. We had pencilled in a similar target to this year.

- The NTMA notes that this reflects the E15bln maturities due in the coming year, so this is still a net negative funding target.

- There is no guidance on the syndication but we look for a new 10-year Oct-36 bond to be launch via syndication in Q1.

- One syndication is as expected, but it may be larger and/or there may be more auctions.

- 2025's target was E6-10bln which one syndication. E8.5bln nominal was raised this year with E3bln of that being via a syndicated launch of the 30-year 3.15% Oct-55 IGB.

- As expected, and as has been the case in recent years, there are no plans to issue bills.

UK auction results

- GBP0.75bln of the 4.25% Jun-32 Gilt. Avg yield 4.109% (bid-to-cover 4.35x, tail 0.4bp).

Austria auction results

- E575mln (E500mln allotted) of the 2.80% Sep-32 RAGB. Avg yield 2.807% (bid-to-cover 2.39x; bid-to-issue 2.08x).

FOREX: USDJPY Recovery Extends, AUD Outperforming Post-RBA

- USDJPY extended overnight gains through the European open, briefly printing 156.43, but stalling ahead of 156.58 resistance, the November 28 high. While interest rate correlations have been weaker in recent months, this week's corrective strength has been underpinned by hawkish repricing across core FI markets. A subsequent 30 pip fade off highs coincided with a downtick in the US 10y yield, followed by a Ueda interview which does little to dispel BOJ hiking expectations for December.

- AUD outperforms in the aftermath of the RBA, with the latest downtick for the DXY propelling AUDUSD back towards session highs. 0.6650 has continued to hold across the last three sessions, and a break above would likely prompt some momentum demand. Alongside the RBA’s expected hold at 3.6%, the board sees the balance of risks tilted toward a potential rate hike in 2026 to contain inflation, with cuts firmly off the table, according to Governor Bullock. 0.6707 remains the key AUDUSD resistance, the Sep 17 high.

- It is worth highlighting that NZDUSD has traded all the way back to its medium-term pivot at 0.5800, potentially providing an opportunity to re-establish longs in AUDNZD, which has been in a very strong uptrend across the second half of 2025. The cross has remained well supported by the 50-day EMA, intersecting around the 1.14 mark.

- Ahead of the AUD, the Swedish Krona tops the G10 leaderboard amid the stable risk backdrop Tuesday. Recent domestic data has suggested an economic recovery is taking hold in Sweden, helping EURSEK narrow the gap to support at 10.8815.

- BOE Deputy Governors Lombardelli and Ramsden, and external rate-setters Mann and Dhingra speak at Parliament's Treasury Committee later today. The data calendar sees the US weekly ADP release, NFIB small business index, weekly redbook retail sales, and JOLTS job openings ahead of tomorrow's FOMC.

FOREX: AUDUSD Resilience Persisting, Probing 0.6650

- In the aftermath of the RBA, AUD remains among the strongest in G10, with the latest downtick for the DXY propelling AUDUSD back towards session highs. 0.6650 has continued to hold across the last three sessions, and a break above would likely prompt some momentum demand.

- Alongside the RBA’s expected hold at 3.6%, the board sees the balance of risks tilted toward a potential rate hike in 2026 to contain inflation, with cuts firmly off the table, according to Governor Bullock. She added that policymakers will reassess the restrictiveness of the current cash rate in the new year. Westpac noted that AUDUSD “dips are likely to remain shallow and well supported against this backdrop.”

- For AUDUSD, a strong impulsive bull wave remains intact, bolstered by moving average studies recently crossing into a bull-mode position. Above here, there is a small level at 0.6660, however, 0.6707 remains a key resistance, the Sep 17 high.

- With both the RBA and RBNZ decisions out of the way, and NZDUSD trading all the way back to its medium-term pivot at 0.5800, this could be an opportunity to re-establish longs in AUDNZD, which has been in a very strong uptrend across the second half of the year. The 50-day EMA provided firm support around the 1.1400 handle last week, bolstering the chances of a return to 12-year highs above the 1.16 handle.

OPTIONS: Expiries for Dec09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1585-90(E1.7bln), $1.1600(E755mln), $1.1675(E784mln), $1.1760(E1.3bln)

- EUR/GBP: Gbp0.8785-92(E530mln)

- AUD/USD: $0.6330-35(A$1.2bln)

EQUITIES: Eurostoxx Futures Holding Onto Gains, Targets Key Resistance at 5825

- A bull cycle in Eurostoxx 50 futures remains intact and the contract is holding on to its recent gains. Price has recently cleared the 20- and 50-day EMAs, signalling scope for a stronger recovery. Sights are on 5742.40 next (pierced), 76.4% of the Nov 13 - 21 bear leg. Clearance of this price point would pave the way for an extension towards 5825.00, the Nov 13 high and a key resistance. First key support lies at 5626.00, the 50-day EMA.

- A bull cycle in S&P E-Minis remains intact and price is trading above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support is at 6802.68, the 20-day EMA.

COMMODITIES: Trend Set-Up in Gold Unchanged and Bullish

- Short-term gains in WTI futures appear corrective - for now. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction.

- The trend condition in Gold is unchanged, the set-up remains bullish. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch lies at the 50-day EMA, at $4037.3. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 09/12/2025 | - | FOMC Meetings with S.E.P. | ||

| 09/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 09/12/2025 | 1415/1415 | BOE Lombardelli, Ramsden, Dhingra, Mann at TSC | ||

| 09/12/2025 | 1500/1000 | *** | JOLTS jobs opening level | |

| 09/12/2025 | 1500/1000 | *** | JOLTS quits Rate | |

| 09/12/2025 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 09/12/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/12/2025 | - | Bank of Canada Meeting | ||

| 10/12/2025 | 0130/0930 | *** | CPI | |

| 10/12/2025 | 0130/0930 | *** | Producer Price Index | |

| 10/12/2025 | 0700/0800 | *** | CPI Norway | |

| 10/12/2025 | 0700/0800 | ** | Private Sector Production m/m | |

| 10/12/2025 | 0900/1000 | * | Industrial Production | |

| 10/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 10/12/2025 | 1000/1000 | Chancellor Reeves Testifies at TSC on Budget | ||

| 10/12/2025 | 1045/1045 | BOE Bailey Pre-recorded Chat on Financial Stability | ||

| 10/12/2025 | 1055/1155 | ECB Lagarde Interview on Currencies/Digital Euro | ||

| 10/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 10/12/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 10/12/2025 | - | *** | Money Supply | |

| 10/12/2025 | - | *** | Social Financing | |

| 10/12/2025 | - | *** | New Loans | |

| 10/12/2025 | 1330/0830 | *** | Employment Cost Index | |

| 10/12/2025 | 1445/0945 | *** | Bank of Canada Policy Decision | |

| 10/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 10/12/2025 | 1530/1030 | BOC press conference | ||

| 10/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 10/12/2025 | 1900/1400 | ** | Treasury Budget | |

| 10/12/2025 | 1900/1400 | *** | FOMC Statement | |

| 10/12/2025 | 1930/1430 | Fed Chair Powell Press Conference |