MNI US MARKETS ANALYSIS - Takaichi Sweeps Election, JPY Firmer

Highlights:

- Takaichi sweeps election, pledge not to boost bond issuance supports JPY

- UK PM loses another key ally, supporting odds of his departure from office by end of H1

- Busy session for Fedspeak - but frequency of speakers mean we may not learn much

US TSYS: Bear Steeper Following Takaichi Victory

Treasuries are bear steeper with the front-end somewhat pinned ahead of Wednesday’s NFP and Friday’s CPI reports, not to forget retail sales tomorrow as well, but with the long-end slipping on larger moves in JGBs following Japan PM Takaichi’s snap election landslide win.

- Cash yields are 0-3bp higher, with increases led by 20s and 30s.

- 5s30s at 111.4bp (+1.9bp) but still off overnight Friday highs of 113.3bp when crypto pressures peaked.

- TYH6 trades at 111-31 (-04+) on strong cumulative volumes of 495k.

- It’s off an earlier low of 111-26 which pierced support at 111-29 (20-day EMA) after which lies the bear trigger at 111-09 (Jan 20 low). Resistance meanwhile is seen at 112-16+ (Feb 6 high).

- Data: NY consumer survey incl inflation expectations Jan (1100ET)

- Fedspeak: Waller (1330ET), Miran (1430ET), Bostic (1515ET), Miran (1700ET)

- Bill issuance: US Tsy $89B 13W & $77B 26W bill auctions (1130ET)

- Politics: Trump in TV interview (1500ET), Trump in policy meeting (1730ET)

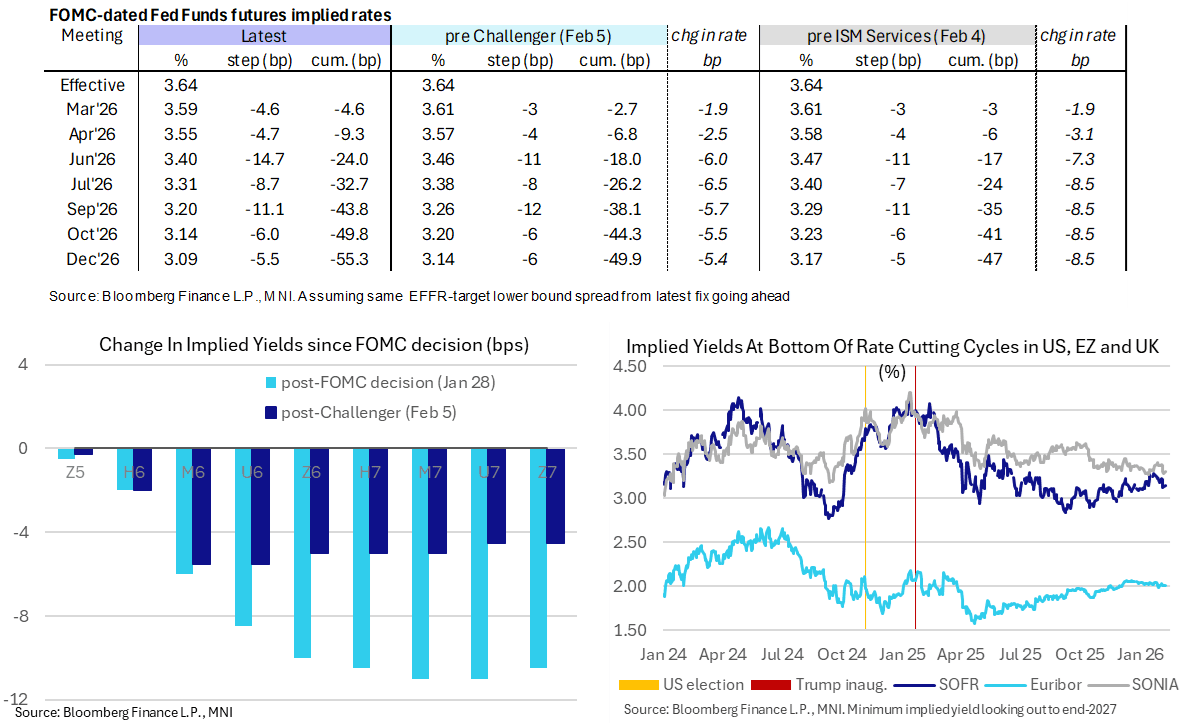

STIR: Last Week’s Weak Labor Data Still Felt Ahead Of Mid-Week NFPs

- US rates sit a touch more hawkish than Friday’s close, extending a slow paring of the dovish reaction to Thursday’s suite of weak labor updates.

- Still, the cumulative 24bp of cuts priced for the June FOMC compares with 18bp prior to the Challenger release in what was the first of four separate reports that were all outright soft or at least softer than expected.

- FF cumulative cuts from 3.64% effective: 4.5bp Mar, 9.5bp Apr, 24bp Jun, 32.5bp Jul, 44bp Sep, 50bp Oct and 55.5bp Dec.

- SOFR futures trade from unchanged to 1.5 ticks lower out to end-2027, with a terminal implied yield of 3.145% (Z6) compared to a ytd range of 3.095-3.285% at each close.

- Today sees a very light data schedule and we might not hear much new from Fedspeak either. Waller explained his dovish dissent at the Jan 30 FOMC, Miran's views are well-known and Atlanta Fed's Bostic (non-voter) spoke last week and is retiring this month.

- 1330ET - Gov. Waller (voter, dove) on digital assets (no text)

- 1430ET - Miran (voter, dove) in moderated conversation (no text)

- 1515ET - Bostic (retiring end-Feb) in moderated conversation with editor of Pro Farmer (no text)

- 1700ET - Gov. Miran in podcast interview (no text)

SOFR: Mix Of Short Setting & Long Cover In Futures On Friday

OI data points to net long cover dominating across the white, red and blue SOFR futures packs on Friday, while net short setting was more prominent in the greens as most contracts across that area of the strip softened come settlement.

| 06-Feb-26 | 05-Feb-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,355,583 | 1,347,627 | +7,956 | Whites | -34,316 |

SFRH6 | 1,361,087 | 1,376,862 | -15,775 | Reds | -46,973 |

SFRM6 | 1,437,968 | 1,450,792 | -12,824 | Greens | +16,409 |

SFRU6 | 1,430,402 | 1,444,075 | -13,673 | Blues | -12,256 |

SFRZ6 | 1,411,363 | 1,401,839 | +9,524 |

|

|

SFRH7 | 971,806 | 1,040,483 | -68,677 |

|

|

SFRM7 | 895,254 | 889,602 | +5,652 |

|

|

SFRU7 | 842,602 | 836,074 | +6,528 |

|

|

SFRZ7 | 906,680 | 903,010 | +3,670 |

|

|

SFRH8 | 524,415 | 515,331 | +9,084 |

|

|

SFRM8 | 438,466 | 441,026 | -2,560 |

|

|

SFRU8 | 394,780 | 388,565 | +6,215 |

|

|

SFRZ8 | 373,669 | 378,127 | -4,458 |

|

|

SFRH9 | 218,692 | 217,168 | +1,524 |

|

|

SFRM9 | 206,976 | 213,271 | -6,295 |

|

|

SFRU9 | 173,924 | 176,951 | -3,027 |

|

|

US TSY FUTURES: Cover Dominated On Friday

OI data points to cover dominating as the curve twist flattened on Friday, with net long cover across TU, FV & TY futures outweighing net short cover in UXY and WN futures.

- Modest net long setting was seen in US futures.

- Overall curve-wide net exposure was reduced by nearly $8mln DV01.

| 06-Feb-26 | 05-Feb-26 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,687,640 | 4,761,007 | -73,367 | -2,703,039 |

FV | 6,893,074 | 6,924,501 | -31,427 | -1,345,371 |

TY | 5,437,918 | 5,462,012 | -24,094 | -1,581,159 |

UXY | 2,545,035 | 2,565,226 | -20,191 | -1,792,702 |

US | 1,723,901 | 1,720,252 | +3,649 | +500,969 |

WN | 2,175,643 | 2,181,205 | -5,562 | -1,011,208 |

|

| Total | -150,992 | -7,932,511 |

UK: No. 10 Comms Director Quits In Another Blow To PM's Authority

Tim Allan, Prime Minister Sir Keir Starmer's director of communication, has announced he is standing down. Allan's departure was not expected, and came less than 24 hours since Starmer's chief of staff, Morgan McSweeney, resigned himself amid the ongoing scandal regarding the appointment of Peter Mandelson as ambassador to the United States. Allan said his resignation came in order to allow the PM to set up a new team to run 10 Downing Street. The resignation of two of the seniormost political appointees within the PM's office within a day of one another comes as a major blow to Starmer's already weakened standing.

- The PM is due to speak to the parliamentary Labour Party this evening in what is increasingly looking like a make-or-break event for his continued leadership of the party and the government.

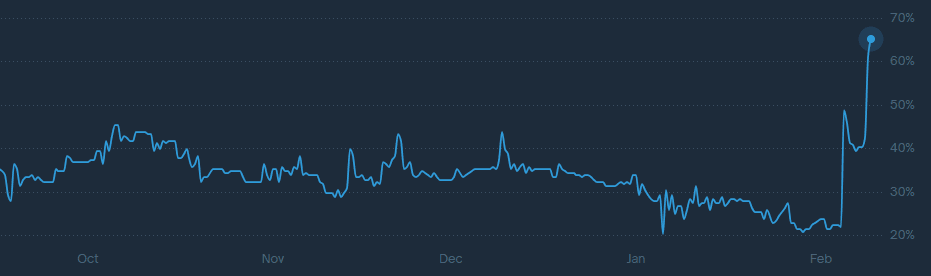

- Data from predictions market Polymarket shows bettors assigning a 67% implied probability that Starmer is out of 10 Downing Street by 30 June, up from 22% on 4 Feb. While not an exact science, predictions markets such as these can give a useful real-time indicator of public sentiment towards a politician or event.

Chart 1. Predictions Market Implied Probability PM Starmer Leaves Office by 30 June, %

Source: Polymarket

EUROPE ISSUANCE UPDATE

EU-BOND SYNDICATION: 2.75% Dec-32 / 3.75% Oct-45 dual-tap mandate

- "The EU (EUROPEAN UNION) has mandated Goldman Sachs Bank Europe SE, J.P. Morgan, Natixis, NatWest and Nordea as Joint Lead Managers for its upcoming EUR Fixed Rate RegS Bearer dual tranche transaction, comprising a TAP of the outstanding 2.750% Dec-2032 (EU000A4ED0K0) and a TAP of the outstanding 3.750% Oct-2045 (EU000A4EA8Y7). No further group. The transaction will be launched tomorrow, subject to market conditions."

- We pencil in E4-5bln of the 2.75% Dec-32 EU-bond and E4-5bln of the 3.75% Oct-45 EU-bond with a total transaction size of E8-10bln.

GBP: EURGBP Narrows Gap To 0.8746 Resistance

- Relative GBP underperformance at the beginning of the week highlights ongoing market caution around political uncertainty surrounding PM Starmer and the BOE outlook also leaning dovish. Sterling price action is in fitting with several analysts raising their conviction on GBP shorts last week, with many expressing this opinion via long EURGBP recommendations.

- Given the broader dollar weakness, EURGBP price action is noteworthy today, with the cross briefly rising above last week's 0.8721 highs. Key short-term resistance to monitor is 0.8746, the Jan 21 high, where a break would signal a potential trend reversal to the upside.

- In domestic politics, Starmer’s future is increasingly in doubt, with prediction market-implied odds raising to 60% for a departure by June 30. This comes after reports have suggested Starmer may look to appoint MPs from the left of the party to his cabinet to appease those who are arguing for him to step aside, following his involvement with former ambassador Mandelson. Market caution has two legs here as the fiscal angle adds to political instability.

- BoE-dated OIS is still pricing roughly 2/3 odds of a cut at the Bank’s March meeting, with MPC member Mann (who seems closer to voting for a cut then she was previously) due to speak at 19:30 GMT today. Note that she will speak on ‘the dollar and continued US exceptionalism’, so we may not get much on UK monetary policy. On the data calendar, preliminary Q4 GDP is due on Thursday.

OPTIONS: Expiries for Feb09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800-10(E1.4bln), $1.1900(E3.0bln)

- USD/JPY: Y155.00($506mln), Y157.10($824mln)

- AUD/USD: $0.6860(A$1.3bln), $0.6900(A$1.6bln)

EQUITIES: Break of Bear Trigger for E-Mini S&P Proves to Be Short-Lived

The medium-term trend condition in EuroStoxx 50 futures remains bullish and for now, the latest pullback appears corrective. Key support lies at the 50-day EMA at 5870.81. It has been pierced, a clear break of this average would undermine the bull theme and signal scope for a deeper retracement. The bull trigger is at 6086.00, the Jan 3 high. A move through this hurdle would resume the primary uptrend. A short-term bearish theme in S&P E-Minis resulted in a break last week of 6814.50, the Jan 21 low and a bear trigger. This proved short-lived, however, with prices rising swiftly back above to begin this week. Note this puts the contract back above the 20- and 50-day EMAs. Any continuation lower would open 6691.56, a Fibonacci retracement point. The contract has recovered today. Initial firm resistance now is 7025.46, the 1.0% 10-dma envelope. A break of this hurdle would be bullish.

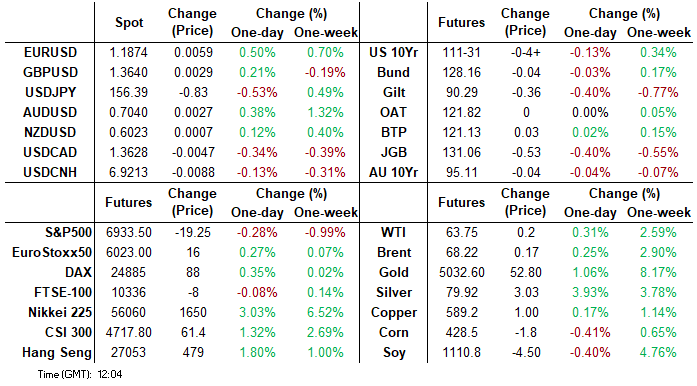

- Japan's NIKKEI closed higher by 2110.26 pts or +3.89% at 56363.94 and the TOPIX ended 84.57 pts higher or +2.29% at 3783.57.

- Elsewhere, in China the SHANGHAI closed higher by 57.507 pts or +1.41% at 4123.09 and the HANG SENG ended 467.21 pts higher or +1.76% at 27027.16.

- Across Europe, Germany's DAX trades higher by 33.07 pts or +0.13% at 24755.31, FTSE 100 higher by 6.82 pts or +0.07% at 10376.25, CAC 40 down 9.02 pts or -0.11% at 8264.48 and Euro Stoxx 50 up 3.32 pts or +0.06% at 6001.49.

- Dow Jones mini down 23 pts or -0.05% at 50187, S&P 500 mini down 16.5 pts or -0.24% at 6937.5, NASDAQ mini down 112 pts or -0.45% at 25060.25.

COMMODITIES: Bull Cycle in WTI Futures Intact, Focus on 20-Day EMA Support

A bull cycle in WTI futures remains intact. However, the reversal from the Jan 29 high continues to highlight a corrective cycle. Attention is on support at the 20-day EMA, at $61.93. The 50-day EMA lies at $60.34. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high. The latest bounce in Gold highlights a retracement of the Jan 29 - Feb 2 sell-off. The next two resistance points to monitor are $5139.9 and $5314.0, Fibonacci retracement levels. Note that the sharp sell-off from the Jan 29 high highlights a potential top in the L/T trend and from a S/T perspective, an unwinding of the recent extreme overbought condition. A resumption of bearish activity would refocus attention on $4403.0, the Feb 2 low.

- WTI Crude down $0.18 or -0.28% at $63.37

- Natural Gas down $0.24 or -7.07% at $3.178

- Gold spot up $25.5 or +0.51% at $4990.4

- Copper down $0.25 or -0.04% at $588

- Silver up $1.83 or +2.34% at $79.696

- Platinum down $45.75 or -2.18% at $2057.19

| Date | GMT/Local | Impact | Country | Event |

| 09/02/2026 | 1200/1300 | ECB's Lane Lecture At Maynooth University | ||

| 09/02/2026 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 09/02/2026 | 1600/1700 | ECB's Lagarde On The State Of Euro Economy and ECB Activities | ||

| 09/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 09/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 09/02/2026 | 1830/1330 | Fed Governor Christopher Waller | ||

| 09/02/2026 | 1930/1930 | BOE's Mann Panel Appearance At Global Interdependence Centre conference | ||

| 09/02/2026 | 1930/1430 | Fed Governor Stephen Miran | ||

| 09/02/2026 | 2015/1515 | Atlanta Fed's Raphael Bostic | ||

| 09/02/2026 | 2200/1700 | Fed Governor Stephen Miran | ||

| 10/02/2026 | 0001/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 10/02/2026 | 0700/0800 | ** | Private Sector Production m/m | |

| 10/02/2026 | 0700/0800 | *** | CPI Norway | |

| 10/02/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 10/02/2026 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 10/02/2026 | 1200/0700 | ** | Brazil Final CPI | |

| 10/02/2026 | - | *** | New Loans | |

| 10/02/2026 | - | *** | Money Supply | |

| 10/02/2026 | - | *** | Social Financing | |

| 10/02/2026 | 1330/0830 | *** | Employment Cost Index | |

| 10/02/2026 | 1330/0830 | ** | Import/Export Price Index | |

| 10/02/2026 | 1330/0830 | *** | Retail Sales | |

| 10/02/2026 | 1330/0830 | *** | Retail Sales | |

| 10/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 10/02/2026 | 1500/1000 | * | Business Inventories | |

| 10/02/2026 | 1500/1000 | * | Business Inventories | |

| 10/02/2026 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 10/02/2026 | 1700/1200 | Cleveland Fed's Beth Hammack | ||

| 10/02/2026 | 1800/1300 | Dallas Fed's Lorie Logan | ||

| 10/02/2026 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result |