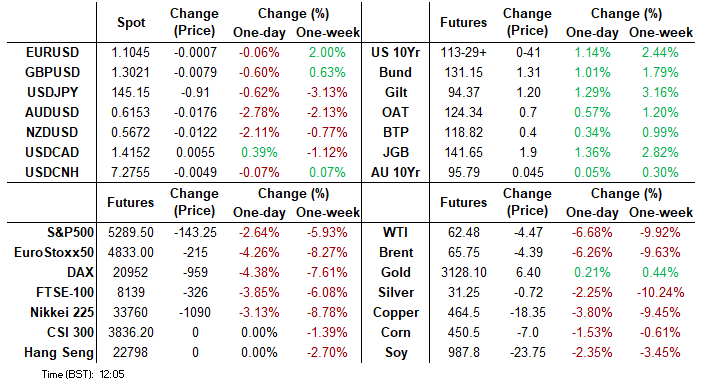

MNI US MARKETS ANALYSIS - Stock Slide Accelerates

Highlights:

- Stocks slide accelerates, with US futures off a further 2.5% ahead of the open

- Payrolls watched for next vol cue ahead of Powell's appearance later today

- AUD/JPY downdraft puts cross to new multi-year lows

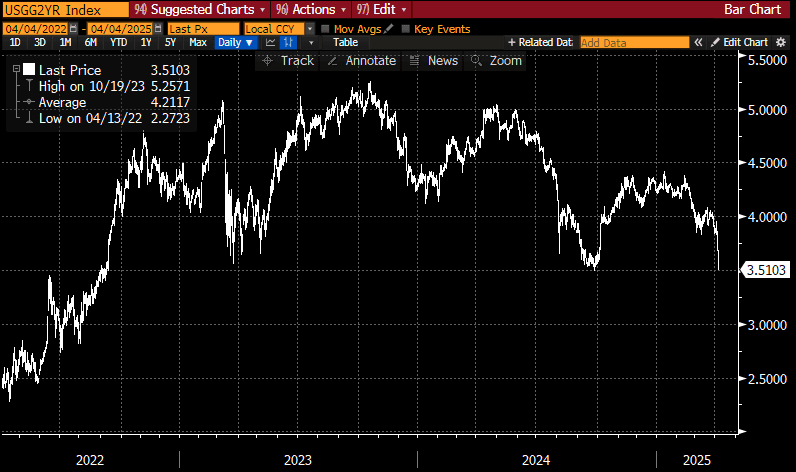

US TSYS: 2YY Yields Probe Significant 3.5% Level

- Treasuries have surged further as China trade retaliation has sparked a sharp risk-off wave on top of already bearish sentiment seen overnight.

- Cash yields are 11.5-17.5bp lower on the day, with declines led by 3s.

- 2Y yields look to test 3.50% (hit 3.5001%). They bottomed out at 3.5000% in Sep 2024 at levels otherwise last seen in Sep 2022.

- 10Y yields cleared 3.8811% (76.4% retrace of Sep/Jan range) with a low of 3.873%, currently within 1bp of that level.

- 2s10s briefly hit new recent highs of 38bps (steepest since Jan 24), currently at 36.9bp (+1.9bp).

- TYM5 trades at 113-29 (+ 1-08+) just off highs of 113-30+ on another overnight session with huge cumulative volumes (over 1.25mln).

- Another firm clearance of resistance sees the round 114-00 as a next level after which lies 114-16 (Fibo projection). Support is seen at 112-01 (Mar 4 high and recent breakout level).

- Data: Payrolls (0830ET) – MNI Preview: https://media.marketnews.com/USNFP_Apr2025_Preview_a7264d37f7.pdf

- Fedspeak: Powell on economic outlook (1125ET, text + Q&A), Barr on AI and banking (1200ET, text + Q&A), Waller on payments (1245ET, Q&A)

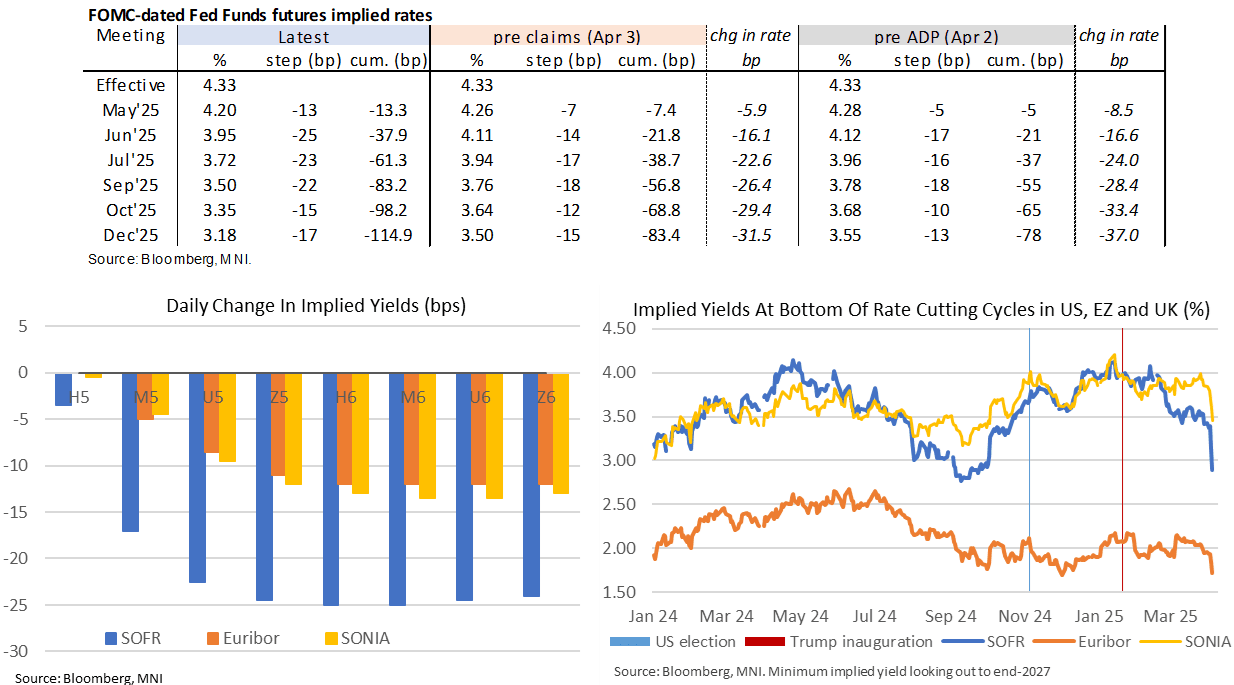

STIR: Fed Rate Path Tumbles Further, 4.5 Cuts Priced For 2025

Fed Funds implied rates have tumbled in recent trading and price more than 50/50 odds of a cut at the next meeting in May and a cumulative 115bp of cuts for 2025 vs 96bp yesterday and 77bp pre-tariffs.

- Cumulative cuts from an assumed 4.33% effective: 13.5bp May, 38bp Jun, 61bp Jul and 115bp Dec.

- This is assuming the same 4.33% effective per yesterday’s fix but some such as WIRP showing an implied 4.31% which would slightly trim those cut expectations.

- SOFR implied terminal yield stands at 2.89% in SFRU6, 24.5bp lower on the day for 51bp lower since tariffs.

- Having already push lower on overnight risk-off, the latest leg came with initial spillover from a dovish reaction in ECB rates to a MNI exclusive before being aggressively compounded by China trade retaliation with extra 34% tariffs on US goods and export controls of some rare earth items.

- The March payrolls report is released in two hours. Preview: https://media.marketnews.com/USNFP_Apr2025_Preview_a7264d37f7.pdf .

- It’s followed by Powell ~three hours later. Thoughts here and here.

- 1125ET – Powell on economic outlook (text + Q&A)

- 1200ET – Barr on AI and banking (text + Q&A)

- 1245ET – Waller on payments (just Q&A)

CHINA: USD/CNH Snaps Higher as China Unveil Counter-Tariffs

China have announced additional tariff measures on US goods, according to a statement from the Xinhua.

- USD/CNH snaps higher on that headline, narrowing gap with 7.2836, the overnight high. These tariffs are levied from April 10th, and equate to 34% tariffs on all US goods as well as 11 US companies being added to the unreliable list, and 16 entities to the export control list.

US TSY FUTURES: Over $20mln Net DV01 Equivalent Added During Thursday’s Rally

OI data points to a huge $20mln+ DV01 equivalent of fresh net longs being set across the curve on Thursday, as feedthrough from the “Liberation Day” tariff announcements dominated.

- The most meaningful net long setting was seen in TY futures.

| 03-Apr-25 | 02-Apr-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,003,775 | 3,931,635 | +72,140 | +2,780,485 |

FV | 6,638,905 | 6,556,075 | +82,830 | +3,665,486 |

TY | 5,024,819 | 4,922,495 | +102,324 | +6,747,847 |

UXY | 2,342,712 | 2,324,280 | +18,432 | +1,697,638 |

US | 1,857,834 | 1,838,388 | +19,446 | +2,658,069 |

WN | 1,835,199 | 1,822,152 | +13,047 | +2,653,448 |

|

| Total | +308,219 | +20,202,974 |

STIR: Net Long Setting Seen In Most SOFR Futures On Thursday

OI data suggests long setting provided the most prominent positioning input during Thursday’s rally in SOFR futures, with only fairly isolated pockets of net short cover seen.

| 03-Apr-25 | 02-Apr-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,114,081 | 1,137,904 | -23,823 | Whites | +27,862 |

SFRM5 | 1,278,656 | 1,283,489 | -4,833 | Reds | +7,738 |

SFRU5 | 944,119 | 933,534 | +10,585 | Greens | +12,312 |

SFRZ5 | 1,132,979 | 1,087,046 | +45,933 | Blues | +8,772 |

SFRH6 | 643,803 | 652,663 | -8,860 |

|

|

SFRM6 | 684,605 | 681,944 | +2,661 |

|

|

SFRU6 | 638,215 | 633,449 | +4,766 |

|

|

SFRZ6 | 821,313 | 812,142 | +9,171 |

|

|

SFRH7 | 511,744 | 513,942 | -2,198 |

|

|

SFRM7 | 501,849 | 492,426 | +9,423 |

|

|

SFRU7 | 318,096 | 318,437 | -341 |

|

|

SFRZ7 | 437,576 | 432,148 | +5,428 |

|

|

SFRH8 | 235,355 | 231,997 | +3,358 |

|

|

SFRM8 | 191,407 | 191,931 | -524 |

|

|

SFRU8 | 138,298 | 135,400 | +2,898 |

|

|

SFRZ8 | 157,820 | 154,780 | +3,040 |

|

|

GBP: Case for GBP Underperformance Through Tariff Vol is Building

GBP/USD's reversal off yesterday's highs has been fierce: having rallied over 200 pips intraday Thursday, the price has reversed to drop near 250 pips off 1.3207, while EUR/GBP has rallied over 1% on the week.

- The case for GBP underperformance through tariff uncertainty is building: EUR rallied on recent reports that both France and Germany are heavily in favour of sharp countermeasures to protect the domestic economy and businesses against US tariffs. The 20% tariff detailed on Wednesday is likely sufficient to trigger the most sizeable EU response - something the market will likely take at face value given the surprisingly activist German debt brake reform and EU ReARM proposals this year.

- GBP does not stand to benefit from equivalent action given they face the lowest 10% levy. Starmer's government see retaliatory actions as a "last resort", suggesting inflationary pressure from UK countermeasures is low relative to the EU, and the argument for greater government support for businesses is more contained.

- This leaves BoE pricing less exposed vs. the ECB to a correction off this week's lows (3x25bps cuts are now fully priced) - which should in turn favour EUR/GBP.

FOREX: Markets Wary of Potential Triggers for Further Volatility

- Another day of outsized volatility for asset markets, as the ramifications of Trump's tariff regime continue to reverberate through prices. Asia-Pac equities slipped sharply after the negative Wall Street close, with Japan's Nikkei 225 shedding near 3% and spilling over into the European open. Continental equities are off another 1.5 - 3.0%, with Spanish and Italian equities bearing the brunt.

- For currencies, this is dragging growth-proxies and pressing AUD/USD to new pullback lows. The pair is now within range of 0.6187 support, clearance below which opens the bear trigger at 0.6088.

- There remain two key risks to currency markets at this juncture: a further leg lower for global equity sentiment, or a rebounding dollar.

- Firstly, the Russell 2000 Index closed over 20% below the late '24 high yesterday, thereby entering a bear market - the Stoxx 600 is only 9% off the recent high - meaning a catch-lower in European stocks could further undermine sentiment.

- Secondly, the USD Index is bouncing, recovering over 1% off the lows. The drivers for a potential extension of the rally could lie in both today's NFP report as well as the appearance from Fed's Powell. Should the Fed Chair stress the importance of the inflation mandate over-and-above unpredictable near-term growth pressures, the USD could be squeezed higher still, and provide the next trigger for intraday vols.

- Markets expect gains of 140k for headline payrolls today, with the unemployment rate unchanged at 4.1%. Average hourly earnings are expected to keep pace with last month, raising the focus on unrounded figures.

FOREX: USDJPY Remains Under Pressure, Approaches Thursday's Low

- USDJPY remains under pressure following the latest China retaliation, as the dollar index gives back most of it’s gains and the yen is boosted by safe haven flows. The pair did print a new session low of 145.24, just 4 pips shy of yesterday’s low. Below here, the following supports are worth noting:

- 145.00 Round number support

- 144.13 76.4% retracement of the Sep 16 ‘24 - Jan 10 bull leg

- 142.95 1.00 projection of the Feb 12 - Mar 11 - 28 price swing

FOREX: AUDJPY Dips Further on Latest China Headlines

- Latest China news providing some renewed optimism for the Japanese yen, as USDJPY dips back below 146.00, although remains well off the overnight and yesterday’s lows at 145.20/30.

- China proxies coming under additional pressure, as AUDUSD slides below 0.6200 and AUDJPY makes new lows on the session below 90.50. It is worth highlighting that this had been the take profit level from a recent Goldman Sachs short recommendation.

- Just below here, we have the carry unwind lows ~90.15 from August. The next meaningful target for the move would not be until 87.87, the April 2023 low.

OPTIONS: Expiries for Apr04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0700(E2.0bln), $1.0750-60(E2.1bln), $1.0800(E2.4bln), $1.1050(E628mln), $1.1115-25(E548mln)

- USD/JPY: Y147.00($956mln), Y150.00($978mln)

- AUD/USD: $0.6200(A$1.5bln), $0.6350(A$1.3bln)

- USD/CAD: C$1.4050-60($525mln), C$1.4125-35($525mln) C$1.4350($1.2bln), C$1.4400($1.4bln)

| Date | GMT/Local | Impact | Country | Event |

| 04/04/2025 | 1230/0830 | *** | Employment Report | |

| 04/04/2025 | 1525/1125 | Fed Chair Jerome Powell | ||

| 04/04/2025 | 1600/1200 | Fed Governor Michael Barr | ||

| 04/04/2025 | 1645/1245 | Fed Governor Chris Waller | ||

| 04/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 04/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/04/2025 | 0915/1115 | ECB's Schnabel At Economy and Finance Workshop |