MNI US MARKETS ANALYSIS - Risk Rally Holds... For Now

Highlights:

- Risk rally holding for now, but markets cautious of fragile ceasefire

- Trump sees a closed-press heavy day Thursday, with focus still on terms of any extended Iran deal

- PCE data should show solid inflationary pressure, with some firmer spending pre-Iran

US TSYS: A Lighter Overnight After Prior Ceasefire Fluctuations

Treasuries trade in narrow ranges on light volumes as they consolidate yesterday’s paring of the initially rally seen on the two-week US-Iran ceasefire. TYM6 briefly tested initial support late yesterday although currently sits a little higher. Today sees some notable data updates at 0830ET – to the extent that data can have an impact amidst a still fluid geopolitical backdrop – before 30Y supply offers a test of duration demand.

- Cash yields are 0.2bp higher (2s) to 0.7bp lower (5s) on the day.

- TYM6 trades at 111-09 (+01+) on light cumulative volumes of 250k.

- It’s off yesterday’s late low of 111-04 in a move that briefly probed support at 111-04+ (20-day EMA) after which lies 110-16 (Apr 2 low).

- Yesterday’s high of 111-21 probed latest resistance at the notable 50-day EMA and didn’t push higher, with gains deemed corrective.

- Data: PCE Feb (0830ET), Weekly jobless claims (0830ET), GDP Q4T (0830ET), Wholesale inventories/trade sales Feb/Feb F (1000ET)

- Coupon issuance: US Tsy $22B 30Y bond re-open - 912810UR7 (1300ET). Last month’s re-open stopped through by 0.7bps but the bid-to-cover fell from 2.66 to 2.45.

- Bill issuance: US Tsy $80B 4W bills, $75B 8W bills (1130ET)

- Politics: A “closed press”-heavy schedule today, with Trump in an intelligence briefing (1100ET), four policy meetings (1330ET, 1400ET, 1700ET and 1800ET) plus a MAHA roundtable (1600ET)

- Bloomberg reports that US President Trump vowed to keep US troops in the Persian Gulf ahead of talks with Iran that are planned to firm up a fragile truce, while Tehran warned there may be mines in a strategic waterway Washington wants reopened. Iran's deputy foreign minister Khatibzadeh meanwhile told the BBC that Israeli attacks on Lebanon were a ‘grave violation’ of the US-Iran ceasefire deal.

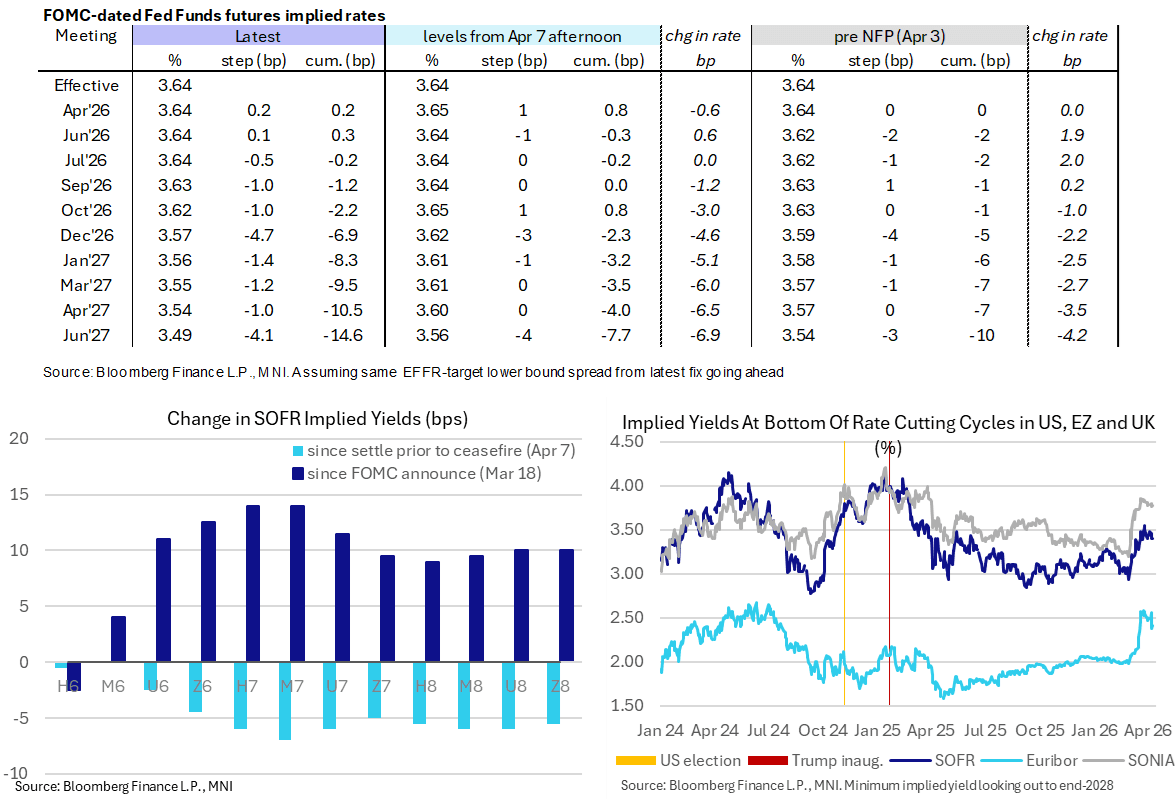

STIR: US Rates Consolidate Yesterday’s Questioning Of Ceasefire

- US rates are little changed overnight, consolidating yesterday’s large paring of the rally seen on the two-week US-Iran ceasefire with its fragility increasingly questioned.

- FF cumulative cuts from 3.64% effective: 0bp Apr, 2bp Jun, 4bp Jul, 6bp Sep, 7.5bp Oct and 12.5bp Dec before building to 20bp of cuts with Jun 2027.

- SOFR futures are within +/-0.5 ticks on the day, with the terminal implied yield at 3.40% (Z7) for still at the higher end of the 3.075% (Mar 2) - 3.55% (Mar 26) closes since initial US-Israel strikes on Iran on Feb 28.

- Today’s data is highlighted by Feb PCE, weekly jobless claims and Q4 GDP revisions.

- There is no Fedspeak scheduled. Yesterday’s FOMC minutes showed slightly more participants in March saw potential for the next move being a hike compared with January's meeting (“some” vs “several” judged strong case for a two-sided description of future interest rate decisions).

US PREVIEW: PCE Report Seen With Solid Inflation & Some Firmer Spending Pre-Iran

The personal income and outlays report for February is released at 0830ET today along with the third Q4 national accounts update and weekly jobless claims data. Whilst ‘stale’, it’s expected to show a continuation of core PCE inflation around 3% Y/Y as it remained stubbornly above target even prior to any potential spillover from the surge in energy prices in March. Real spending growth might have also firmed slightly after a subdued three months.

- Core PCE inflation is expected to have increased 0.4% M/M in February with risk of rounding down to 0.3% M/M to extend a solid run after two months at 0.36% M/M (which could see a small upward revision to Jan and downward revision to Dec).

- Some unrounded estimates include GS 0.32, JPM 0.37, Nomura 0.37, MS 0.38, UBS 0.38 and DB 0.39.

- With the BEA still catching up on the release schedule after 2025 government shutdown disruption, March CPI will follow just a day later on Friday. Early analyst estimates have a median of 0.24% (range 0.23-0.34) for core PCE in March but with adjustments to be made after CPI and then PPI/import prices on Apr 14/15.

- Revisions aside, this tentative profile would see core PCE inflation inch lower to 2.99% Y/Y in Feb after 3.06% Y/Y in Jan before ticking up to 3.13% Y/Y in Mar. It first returned to a rounded 3.0% Y/Y rate in December for the first time since Feb 2025 having bottomed at 2.61% Y/Y in Apr 2025 in the interim.

- On the activity side, nominal spending is expected to have been firm at 0.6% M/M in Feb after 0.4% M/M, seen translating to real spending rising 0.2% M/M after three months averaging a modest 0.1% M/M.

- Firmer nominal retail sales data have played a part in this expected profile, with overall sales up 0.6% M/M (cons at the time 0.5) and control up 0.45% M/M (cons 0.3).

- Strong start-of-year disposable income growth saw the savings ratio lift 0.5pts to 4.5% back in January for its highest since July but it's still low historically and set for a further decline judging by consensus for personal income growth of 0.3% M/M in Feb.

MNI US CPI PREVIEW: A Crude Shift Further From Target

Released Friday at 0830ET, headline CPI is expected to have surged in March with a 0.9-1.0% M/M increase due to a historically large energy price increase on the US-Israel-Iran war. Core CPI is seen increasing a more modest 0.27% M/M in March after 0.22% M/M, with much more limited initial spillover from the energy shock. Within core, expect transportation-related categories to be in focus plus broader indications of supply chain pressures which ticked up to a fresh high since early 2023 according to the NY Fed.

CROSS ASSET: Equity Recovery Has Been Notable, But Could Reflect Complacency

- Benchmarking cross-asset returns on the ceasefire bounce this week expose an inconsistency among the major asset classes. Equities are the major beneficiary, while energy complex returns have been considerably more conservative.

- The reported ceasefire agreement between the US and Iran is on fragile footing, but markets across asset classes have moved away from “risk off” extremes. Equities have registered the largest retracement, with the Eurostoxx 50 having retracted ~56% of the Feb 27 – March 20 selloff, and the S&P 500 seeing a more notable 80% retracement of the Feb 27 – March 30 pullback.

- In contrast, crude oil, fixed income and precious metals have seen more contained retracements.

- One rationale for this dynamic is that equities are taking a longer-term forward-looking view: an end to the war would allow markets to refocus on potential tailwinds related to AI productivity enhancements, for example. That said, it could also be considered complacent given still-elevated geopolitical risks.

- Similar dynamics have been observed this morning: Equity markets are lower on the session but have nonetheless held onto the majority of Wednesday night’s ceasefire-fuelled gains.

EUROPE ISSUANCE UPDATE:

Gilt auction result

- Decent gilt auction with the lowest accepted price of 97.740 comfortably above the secondary market price at the end of the auction window (97.708).

- Elsewhere, despite the larger auction size the tail was the same as the previous auctions of this gilt while the bid-to-cover was very in line with the previous auction at 3.30x, once again exceeding 3x.

- Only marginal follow through to the secondary market price, however, and gilt futures largely ignored the result.

- GBP4bln of the 4.125% Mar-33 Gilt. Avg yield 4.507% (bid-to-cover 3.30x, tail 0.2bp).

Spain Bono/Obli/Obli-Ei Auction

- E1.933bln of the 2.35% Mar-29 Bono. Avg yield 2.734% (bid-to-cover 2.03x).

- E2.084bln of the 2.60% May-31 Bono. Avg yield 2.915% (bid-to-cover 1.81x).

- E1.761bln of the 3.30% Apr-36 Obli. Avg yield 3.435% (bid-to-cover 2.04x).

- E676mln of the 1.15% Nov-36 Obli-Ei. Avg yield 1.32% (bid-to-cover 1.87x).

Finland 10-year Syndication

- E4bln of the 10-year Sep-36 RFGB (MNI expected E4bln with risk of E3bln). Books closed in excess of E12.8bln (in E1.6bln). Spread set: at MS + 32bps (guidance was MS + 34 bps area)

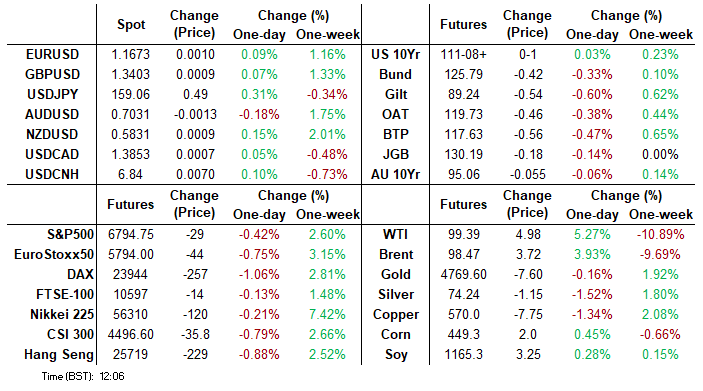

FOREX: USD Weakness Stalls Amid Ceasefire Uncertainty

- Despite Tuesday’s gap lower for the dollar index on the renewed boost to risk sentiment, downside momentum has stalled as market participants grapple with uncertainty surrounding the details of the US/Iran/Israel ceasefire. There has been mixed performance across the G10, with small net adjustments for the major pairs.

- With that said, USDJPY has had the most notable jump this morning, extending the recovery from yesterday’s lows to around 115pips to trade back above 159.00. We flagged yesterday that the JPY had relatively underperformed the move on Wednesday as traders gravitated towards higher-beta plays. Today’s move higher places the pair just 40pips shy of pre-ceasefire levels, with bullish conditions very much intact. The psychological 160.00 mark and cycle highs at 160.46 remain the key resistance points.

- The Australian dollar has exhibited similar price action, falling around 0.25% to 0.7025. This is perhaps the best reflection of the waning risk sentiment, as crude prices rise over 3% and equities see some renewed selling pressure, however, the impact on FX markets remains contained in comparison.

- Conversely, NZD remains 1.5% above pre-ceasefire levels, as the kiwi continues to benefit from yesterday’s hawkish tilt to the April RBNZ meeting. As a reminder, this has prompted several analysts to bring forward their call for rate hikes this year, with September emerging as a popular candidate to begin tightening policy.

- In EM, the likes of ZAR and HUF have reversed around 0.5% of their punchy rallies yesterday, while USDMXN remains close to unchanged on the session at 17.45.

- US final reading of Q4 GDP is scheduled today, alongside PCE, personal income and weekly jobless claims. US CPI on Friday highlights the calendar this week.

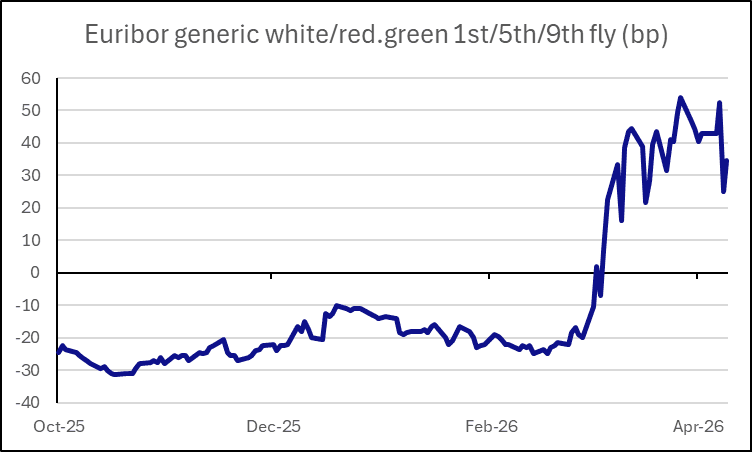

STIR: Correction in late white/early red Euribor should be limited

- ECB pricing is edging in a more hawkish direction this morning. With a permanent ceasefire still lacking and little clarity on oil flows, rates markets should continue to be cautious. OIS reflects this: over 60bps of tightening are priced by year-end versus 50bps yesterday. Late white and early red contracts are leading the correction.

- That said, at 36bps, the generic 1st/5th/9th white/red/green Euribor fly is less than 20bps from its late March peak which suggests that the correction in the late white/early red area of the Euribor strip should be limited from here.

- Meanwhile, yesterday’s move on ceasefire optimism has left markets vulnerable to any deterioration in talks - which could re-trigger bear-flattening flow in Euribor. The latter has clearly been evident overnight with negative headlines focussing on violations of the agreement and a lack of progress on unblocking the Strait of Hormuz.

Source: MNI / Bloomberg Finance L.P.

STIR: SFIM6/Z6/M7 Fly Could Be USed To Hedge Iran Reescalation

SONIA futures have moved to indicate both a flatter BoE hiking cycle through the end of ’26 and less pronounced cutting cycle in ‘27 in recent sessions, as pricing surrounding Iran conflict escalation moderated.

- However, high level conviction for a positive outcome at the impending U.S.-Iran talks is lacking as both sides continue to hold differing stances on the ceasefire agreement and post-conflict demands. This has factored into bearish repricing today.

- Israeli strikes on Hezbollah/Lebanon are ongoing, which has prolonged difficulties when it comes to energy product flow through the Strait of Hormuz, maintaining some degree of stagflationary risk.

- Those looking for reescalation/an adverse scenario come the end of the U.S.-Iran talks could look to pay the wings of the SFIM6/Z6/H7 fly, which trades a little over 30bp below its March peak.

EQUITIES: EuroStoxx 50 Futures Softer But Holding Onto Bulk Wednesday's Gains

A gap higher yesterday in EuroStoxx 50 futures strengthens a short–term bullish theme and highlights an extension of the reversal from the Mar 23 low. The contract has traded through both the 20- and 50-day EMAs, paving the way for a climb towards 5945.47, a Fibonacci retracement point. Note that a break of 5945.47 would expose the key resistance at 6143.00, the Feb 26 high. First key support to watch lies at 5525.00, the Apr 2 low.

A strong rally in S&P E-Minis on Wednesday highlights an extension of the reversal that started Mar 31. Note that trend signals remain bearish and for now, gains are considered corrective. A continuation higher would open 6921.09 next, a Fibonacci retracement point. Key medium-term resistance and the bull trigger is far off at 7096.50, the Jan 28 high. Initial firm support to watch lies at 6567.00, the Apr 6 low.

COMMODITIES: Sharp Pullback in WTI Corrective From a Technical Standpoint

- A sharp pullback in WTI futures is for now, considered corrective. The contract has traded through the 20-day EMA and this exposes a key support around the 50-day EMA, at $85.38. A clear break of the 50-day average is required to signal a stronger short-term reversal. On the upside key resistance and the bull trigger has been defined at $117.63, the Apr 7 high. Clearance of this hurdle would confirm a resumption of the uptrend.

- Recent gains in Gold appear to be corrective, however for now, the short-term bull cycle remains intact. The metal has pierced the 50-day EMA, at $4783.1. This signals scope for an extension towards $4914.9, a Fibonacci retracement point. Clearance of this level would open the $5000.0 handle. Initial firm support to watch lies at $4554.2, the Apr 2 low. A break of this level would be bearish.

| Date | GMT/Local | Impact | Country | Event |

| 09/04/2026 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 09/04/2026 | 1230/0830 | *** | Jobless Claims | |

| 09/04/2026 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 09/04/2026 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 09/04/2026 | 1230/0830 | *** | Personal Income and Consumption | |

| 09/04/2026 | 1400/1000 | ** | Wholesale Trade | |

| 09/04/2026 | 1400/1000 | ** | Wholesale Trade | |

| 09/04/2026 | 1430/1030 | ** | Natural Gas Stocks | |

| 09/04/2026 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 09/04/2026 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 09/04/2026 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 09/04/2026 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 10/04/2026 | 0130/0930 | *** | CPI | |

| 10/04/2026 | 0130/0930 | *** | Producer Price Index | |

| 10/04/2026 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/04/2026 | 0600/0800 | *** | CPI Norway | |

| 10/04/2026 | 0600/0800 | *** | Germany CPI (f) | |

| 10/04/2026 | 0600/0800 | *** | Germany CPI (f) | |

| 10/04/2026 | 0800/1000 | * | Industrial Production | |

| 10/04/2026 | 1000/1200 | ECB de Guindos Remarks at Development Event | ||

| 10/04/2026 | - | *** | New Loans | |

| 10/04/2026 | - | *** | Money Supply | |

| 10/04/2026 | - | *** | Social Financing | |

| 10/04/2026 | 1200/0800 | ** | Brazil Final CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | CPI | |

| 10/04/2026 | 1230/0830 | *** | Labour Force Survey | |

| 10/04/2026 | 1230/0830 | *** | Labour Force Survey | |

| 10/04/2026 | 1400/1000 | *** | UMich Surveys of Consumers | |

| 10/04/2026 | 1400/1000 | *** | UMich Surveys of Consumers | |

| 10/04/2026 | 1400/1000 | ** | Factory New Orders | |

| 10/04/2026 | 1400/1000 | ** | Factory New Orders | |

| 10/04/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/04/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/04/2026 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/04/2026 | 1800/1400 | ** | Treasury Budget |