MNI US MARKETS ANALYSIS - GBP/USD Within Range of Cycle Highs

Highlights:

- Anything other than a 25bps rate cut would be a major surprise at the ECB rate decision

- GBP/USD within range of new cycle highs as markets look through inflationary errors in UK CPI

- China-US trade contacts continue, but still few signs of a breakthrough

US TSYS: TYA Rally Consolidated After Yesterday’s Clearances

- Treasuries trade twist flatter, underperforming EGBs after smooth passing of Spanish and French supply ahead of today’s ECB decision.

- Focus is on today’s labor and trade-related data before potential comments from Trump when speaking to Germany’s Merz in the White House. Tomorrow’s nonfarm payrolls report looms on the horizon along with potential talks between Trump and China's Xi at some point.

- Cash yields are 1bp higher (2s and 3s) to 2bp lower (30s).

- Curves continue to row back from recent steeps, with 5s30s at 93.1bps (-2.6bp) vs Monday’s 100bps.

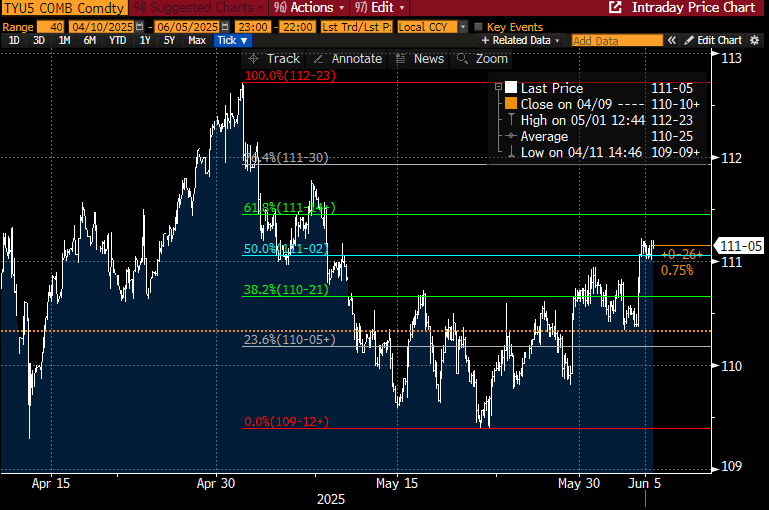

- TYU5 is near unchanged at 111-05 (+ 01+) having just about kept within yesterday’s high of 111-07 on modest cumulative volumes of 290k.

- That high cleared resistance at 111-02 (seen multiple times with May 30, Jun 2/4 highs) and also 111-05+ (May 9 high). It opens 111-14+ (61.8% retrace of May 1-22 downleg) before 111-30 (76.4% retrace), whilst support is seen at a key 110-11 (Jun 3 low).

- Data: Challenger job cuts May (0730ET), Weekly jobless claims (0830ET), Trade balance Apr (0830ET) and ULCs/productivity Q1 f (0830ET)

- Fedspeak: Kugler (1200ET), Schmid (1330ET), Harker (1330ET) – see STIR bullet

- Bill issuance: US Tsy to sell $65bn 4-W, $55bn 8-W bills

- Politics: Trump participates in a Bilateral Meeting With German Chancellor Merz at 1145ET, with some assumed remarks then even if there isn’t an official press conference scheduled.

- The WSJ reports a senior White House official said Trump wasn’t happy about Musk’s decision to lambaste his signature legislation, describing the president as confused as to why the Tesla chief executive decided to ratchet up his criticism after working so closely with the president for four months. The official said senior Trump advisers were caught off guard by Musk’s latest offensive.

- China Vice President Han Zheng is meeting a U.S. delegation for high-level dialogue according to Reuters reporting of state media.

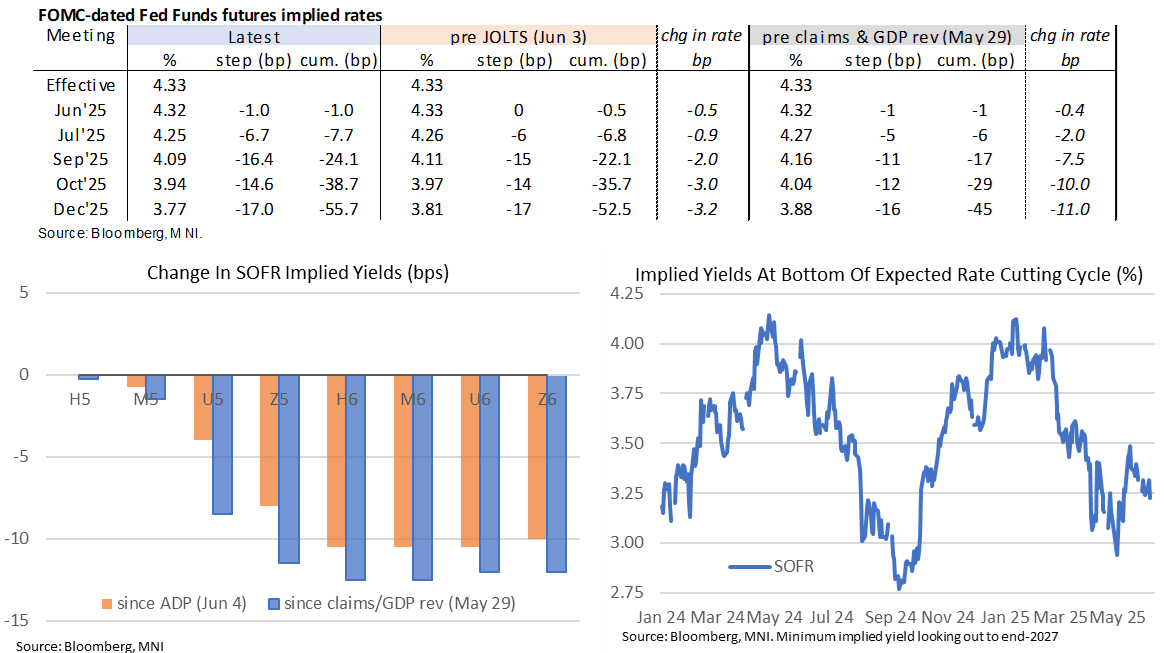

STIR: Fed Rate Path Holds Bulk Of Slide On ADP and ISM Services

- Fed Funds implied rates hold the majority of yesterday’s decline on weak ADP and ISM services reports, albeit with the latter including a further climb in prices paid.

- Cumulative cuts from 4.33% effective: 1bp Jun, 7.5bp Jul, 24bp Sep, 38.5bp Oct and 55.5bp Dec.

- The SOFR implied terminal yield of 3.23% (SFRZ6, +0.5bp) near unchanged on the day having closed at its lowest since May 7 (i.e. pre US-China trade de-escalation).

- Today sees an important update for jobless claims after continuing pushed to a fresh high since late 2021 last week, along with more detailed trade data and Challenger job cuts.

- Gov. Kugler headlines today’s Fedspeak, followed by Schmid on banking policy and then Harker, who holds a role that would next vote in 2026 but who is retiring June 30th.

- 1200ET – Gov. Kugler (permanent voter) on economic outlook & monetary policy (text + Q&A). She last spoke of note on May 12, continuing to promote a patient outlook on rate cuts, saying that "I view our current stance of monetary policy as well positioned for any changes in the macroeconomic environment." She noted re the previous week's rate hold that "given the upside risks to inflation and given that I still view our policy stance as somewhat restrictive, I supported the decision...with inflation and employment potentially moving in opposite directions down the road, I will closely monitor developments as I consider the future path of policy". We watch to see whether she notes an openness to all options including hikes per Gov. Cook earlier this week.

- 1330ET – Kansas City Fed’s Schmid (’25 voter, hawk) on banking policy (text + Q&A). These are Schmid’s first detailed remarks since mid-April, having missed the May FOMC meeting due to the death of his wife.

- 1330ET – Philly Fed’s Harker (’26 voter) on economic outlook (text + Q&A).

ECB: MNI ECB Preview: The Last Consecutive Cut?

- We have published and e-mailed to subscribers the MNI ECB Preview, including MNI analysis plus views from 30 analysts on what to expect at this month's meeting.

- Please find the full report here: https://media.marketnews.com/ECB_Preview_Jun2025_237e09f59f.pdf

US LABOR MARKET: MNI U.S. Payrolls Preview: A Test Of Two Cuts Eyed For 2025

- We have published and e-mailed to subscribers the MNI US Payrolls Preview.

- Please find the full report including MNI analysis and pertinent views from analysts here.

Executive Summary

- Nonfarm payrolls are seen increasing a seasonally adjusted 126k in May in the Bloomberg survey after a stronger than expected 177k in April (albeit one that was more than offset by negative revisions).

- Primary dealer analysts also see 125k whilst the Bloomberg whisper is weaker again, currently at 119k after Wednesday’s weak ADP release continued a clearly moderating trend.

- More analysts than not expect limited impact from the weather but that’s not a unanimous view.

- The industry breakdown will be watched for any weakness in trade & transportation after a strong April - likely on rapid inventory builds on tariff front-running - plus broader implications for discretionary demand.

- The unemployment rate is widely expected to round to 4.2% again after continuing to inch up to 4.19% in April. It would continue a broad plateau seen since last summer although there is mild dovish skew.

- Average hourly earnings are seen rising 0.3% M/M after a softer than expected 0.17% M/M in April, with the workweek watched after a recent recovery from January’s adverse weather lows.

- We expect greater sensitivity to a soft print in the event of a large surprise, although longer-term reaction would likely be capped by the FOMC not wanting a repeat of September’s (with hindsight) overreaction to a sharp but short-lived uplift in the u/e rate.

- A next Fed rate cut is almost fully priced for September before a second in December, both SEP meetings.

STIR: Long Setting Dominated In Most SOFR Futures On Wednesday

OI data points to net long setting dominating in most of white, red and green SOFR futures during Wednesday’s rally, with net short cover seemingly only apparent in SFRH5, M5 & Z7.

- A reminder that a soft round of ADP employment data, a stagflationary ISM services survey and weaker oil prices accounted for much of the rally.

| 04-Jun-25 | 03-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,069,423 | 1,070,120 | -697 | Whites | +14,328 |

SFRM5 | 1,407,828 | 1,428,377 | -20,549 | Reds | +79,664 |

SFRU5 | 1,130,027 | 1,121,423 | +8,604 | Greens | +22,868 |

SFRZ5 | 1,118,429 | 1,091,459 | +26,970 | Blues | -461 |

SFRH6 | 818,362 | 796,257 | +22,105 |

|

|

SFRM6 | 784,612 | 756,922 | +27,690 |

|

|

SFRU6 | 720,267 | 717,166 | +3,101 |

|

|

SFRZ6 | 864,511 | 837,743 | +26,768 |

|

|

SFRH7 | 685,120 | 671,828 | +13,292 |

|

|

SFRM7 | 595,907 | 585,423 | +10,484 |

|

|

SFRU7 | 416,220 | 414,903 | +1,317 |

|

|

SFRZ7 | 409,931 | 412,156 | -2,225 |

|

|

SFRH8 | 293,155 | 291,362 | +1,793 |

|

|

SFRM8 | 214,337 | 214,547 | -210 |

|

|

SFRU8 | 162,490 | 164,228 | -1,738 |

|

|

SFRZ8 | 172,906 | 173,212 | -306 |

|

|

STIR: SONIA/Euribor Dec ’25 Spread Back Towards 200bp

The SONIA/Euribor Dec ’25 futures spread has moved back towards 200bp, after the recent round of widening stalled around 210bp.

- SONIA’s higher sensitivity to U.S. short-end pricing has fed into the narrowing seen over the past few sessions, with this week’s U.S. data providing dovish readthrough on net.

- UK news flow has been relatively limited this week, with BoE Deputy Governor Breeden positioning herself as slightly more dovish than Governor Bailey probably providing the highlight.

- Elsewhere, this morning’s BoE DMP survey was marginally dovish on both inflation and wages, however, progress on these fronts remains comfortably shy of levels that would equate to the BoE attaining its inflation goal

- Immediate focus is on today’s ECB decision, with a 25bp cut essentially fully discounted and ~32bp of further cuts showing through year-end.

- The Bank’s updated inflation forecasts are expected to read dovishly over the medium-term, with downside risks to the growth outlook also heightened.

- Out full ECB preview is here.

- The scope of any downside revisions here and degree of dovishness deployed in the accompanying rhetoric are set to steer market reaction.

- A dovish surprise would trigger fresh SONIA/Euribor Dec ’25 spread widening back towards 210bp. A break there would expose the year-to-date closing high at 217.5bp.

- Meanwhile, a hawkish outcome could help re-focus attention on year-to-date closing lows at 178bp, particularly if BoE matters evolve in a dovish fashion over a multi-week horizon.

Fig. 1: SONIA/Euribor December ’25 Futures Spread

Source: MNI - Market News/Bloomberg

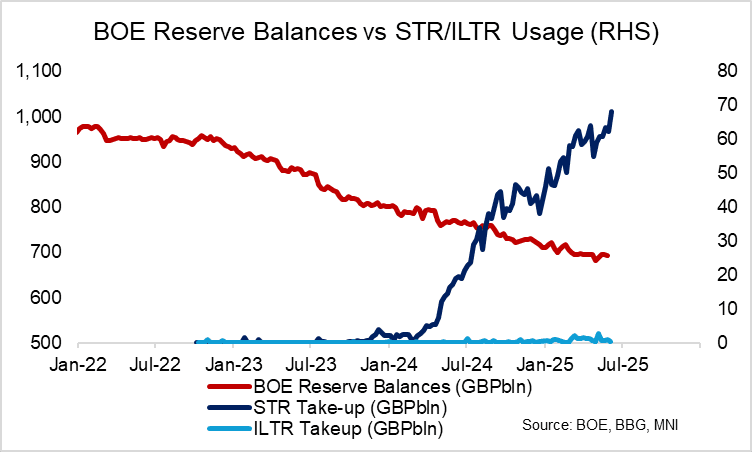

BOE: STR Usage Rises To Fresh Record High; Focus On Saporta Next Week

BOE STR usage rose to a fresh record high of GBP68.1bln at today’s weekly operation. Take-up has been increasing steadily since the start of 2024, with BOE QT progressing and reserve balances steadily declining.

- Reserve balances were GBP693bln as of May 28.

- In her speech earlier this week, BoE MPC member Mann noted that “the estimated range for minimum demand for reserves lies between £385 billion and £530 billion”.

- The lower and upper bound of this range is higher than the GBP345-490bln range provided by Vicky Saporta – the BOE’s Executive Director for Markets – in July last year.

- Saporta is due to speak on “Approaches to QT – How to transition to the steady state?” next Wednesday. It will be interesting to see whether Mann’s PMRR (Preferred Minimum Reserve Range) is re-iterated here, or if the BOE's “house view” remains the previously-stated lower range of GBP345-490bln.

- An upward revision to the range would imply the equilibrium level of reserves is closer than previously thought, indicating a faster transition from an abundant to ample reserve regime.

- These speeches should be viewed in the context of the September BOE decision, where the Bank will decide the target reduction in the stock of gilts within the APF (current pace GBP100bln per year, with active sales of GBP13bln). Recent turmoil at the long-end of global bond markets including gilts adds an additional factor to consider, especially after the BOE made an operational decision to replace a long-maturity bucket sale with a short-maturity back in April.

EUROPE ISSUANCE UPDATE:

Spain auction results

- Decent Spanish auction, which has been well digested by markets:

- Middle of the E5.0-6.0bln range sold.

- Low prices in excess of the pre-auction mid prices across lines, most notably for the off-the-run 0.70% Apr-32 Obli. Secondary market prices for all the nominal bonds on offer have rallied since the results were published.

- The 1.69x bid-to-cover ratio for the on-the-run 2.70% Jan-30 Bono was below the previous auction’s 1.78x and the 1.79x average across the last five outings. However, the secondary price of the bond has since rallied towards session highs (101.366 vs 101.340 low price, 101.282 pre-auction mid).

- Cover ratios for the May-28 and Apr-32 lines were above previous outings and recent averages.

- E2bln of the 2.40% May-28 Bono. Avg yield 2.118% (bid-to-cover 1.94x).

- E2.045bln of the 2.70% Jan-30 Bono. Avg yield 2.386% (bid-to-cover 1.69x).

- E1.443bln of the 0.70% Apr-32 Obli. Avg yield 2.72% (bid-to-cover 2.37x).

- E536mln of the 2.05% Nov-39 Obli-Ei. Avg yield 1.678% (bid-to-cover 2.00x).

France auction results

- Another well digested auction, with the top of the E10-12bln range sold and low prices once again exceeding the pre-auction mid prices across lines. Secondary market prices have consolidated the rally seen in the lead-up to the auction cut-off.

- There’s still some evidence of softening long-end demand here though. The 3.75% May-56 OAT bid-to-cover ratio was quite a bit below the April re-opening (2.29x vs 2.82x prior), despite a smaller amount being sold.

- The 1.25% May-36 OAT bid-to-cover of 3.15x was much softer than the 5.73x seen in February, but is broadly in line with prior average levels.

- The 3.20% May-35 OAT cover of 2.83x was above May’s 2.80x.

- E6.734bln of the 3.20% May-35 OAT. Avg yield 3.17% (bid-to-cover 2.83x).

- E2.476bln of the 1.25% May-36 OAT. Avg yield 3.27% (bid-to-cover 3.15x).

- E2.789bln of the 3.75% May-56 OAT. Avg yield 3.95% (bid-to-cover 2.29x).

GBPUSD: EUR Downside Could Form Next Trigger for GBP/USD Rally

- The low vol backdrop continues to favour GBP/USD at the margins, with markets looking well through both the more dovish turnout from BoE's Breeden earlier this week as well as the admission this morning from the ONS that CPI was overstated by errors in calculating Vehicle Excise Duty for April CPI.

- This keeps GBP/USD in focus, particularly as the rate closes the gap with key resistance - mentioned just above - and the bull trigger at 1.3593, the May 26 high and best level since early 2022.

- In contrast with the GBP rally over late April/early May, this GBP/USD is not allied with EUR/GBP downside. As such, any manifestation of EUR downside on the back of the ECB today (via a stronger signal for another back-to-back rate cut, or particularly pessimistic inflation & growth forecasts) could trigger a further phase of GBP/USD strength to new highs.

- The 15-minute candle chart shows a firm, well-tested support at an uptrendline drawn off the May 12 low (at 1.3530 last, but trending higher). A break through this mark on the daily chart would stall the recent spell of strength, and could signal a correction and clear out of positioning back down to the late May lows of 1.3416.

FOREX: EUR Trades the Range Headed into ECB

- The single currency is rangebound ahead of the ECB meeting, with EUR/USD holding the late rally Wednesday to consolidate above 1.1400. For EUR/GBP, the price remains inside the broad downtrend drawn off the mid-April highs, however S/T momentum has stalled slightly, with the price gravitating toward the 100-dma.

- The JPY is softer against all others in G10 as the USD/JPY rate mean reverts. EUR/JPY continues to trade just above the 50-dma of 162.63, a key level of support that should remain in focus into the ECB decision. Meanwhile, the trend structure in GBPUSD is unchanged, it remains bullish and the pair continues to trade closer to its recent highs. Initial support to watch lies at 1.3431, the 20-day EMA.

- The carry profile across G10 remains a key driver as low levels of vol pervade across spot markets. This continues to favour the relative high yielders in G10 FX, namely AUD and NZD which are higher intraday, and aiding AUD/USD toward recent cycle highs at 0.6537.

- The ECB rate decision takes focus going forward, and anything other than a 25bps rate cut to all three major rates would be a surprise for markets. Focus for the press conference will be on the unanimity (or lack thereof) of the governing council toward their decision on rates, particularly as the benchmark deposit heads toward the midpoint of the bank's assessment of 'neutral'.

OPTIONS: Expiries for Jun05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1050(E5.9bln), $1.1300(E2.3bln), $1.1325-30(E1.0bln), $1.1375-85(E1.7bln), $1.1400(E2.4bln), $1.1415-25(E1.7bln), $1.1500(E1.5bln)

- USD/JPY: Y142.00($1.2bln), Y143.00-05($1.1bln), Y145.00-20($1.6bln)

- EUR/JPY: Y162.00(E571mln), Y167.00(E540mln)

- EUR/GBP: Gbp0.8345-60(E612mln)

- AUD/USD: $0.6490-95(A$1.8bln)

- NZD/USD: $0.5990-15(N$755mln)

- USD/CAD: C$1.3600($560mln)

EQUITIES: Trend Cycle in Eurostoxx 50 Futures Unchanged and Bullish

The trend cycle in Eurostoxx 50 futures is unchanged, it remains bullish and a recent pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen a bull theme. Key support to watch lies at 5268.58, the 50-day EMA. A clear break of this average is required to signal a possible reversal. The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract is trading just ahead of its recent high. A print above 5993.50 last week, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. An extension would open 6057.00 next, the Mar 3 high. Key support lies at 5774.07, the 50-day EMA.

- Japan's NIKKEI closed lower by 192.96 pts or -0.51% at 37554.49 and the TOPIX ended 28.66 pts lower or -1.03% at 2756.47.

- Elsewhere, in China the SHANGHAI closed higher by 7.895 pts or +0.23% at 3384.098 and the HANG SENG ended 252.94 pts higher or +1.07% at 23906.97.

- Across Europe, Germany's DAX trades higher by 97.12 pts or +0.4% at 24373.43, FTSE 100 higher by 7.56 pts or +0.09% at 8808.85, CAC 40 up 25.43 pts or +0.33% at 7830.1 and Euro Stoxx 50 up 20.37 pts or +0.38% at 5425.52.

- Dow Jones mini up 90 pts or +0.21% at 42590, S&P 500 mini up 11 pts or +0.18% at 5992, NASDAQ mini up 52.25 pts or +0.24% at 21818.75.

COMMODITIES: WTI Futures Bear Threat Remains Present

WTI futures continue to trade closer to their recent highs. A bear threat remains present and the recovery since Apr 9 still appears corrective. A key resistance area to monitor is $62.52, the 50-day EMA. It has again been pierced. A clear break of it would highlight a stronger reversal and open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. A bullish theme in Gold remains intact and recent gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Sights are on $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, key support and the bear trigger to watch has been defined at $3121.0, the May 15 low.

- WTI Crude up $0.19 or +0.3% at $63.05

- Natural Gas down $0.03 or -0.81% at $3.686

- Gold spot up $3.84 or +0.11% at $3376.14

- Copper up $4.55 or +0.93% at $493.2

- Silver up $0.33 or +0.97% at $34.8194

- Platinum up $29.24 or +2.67% at $1123.08

| Date | GMT/Local | Impact | Country | Event |

| 05/06/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 05/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 05/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 05/06/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1245/1445 | ECB Press Conference | ||

| 05/06/2025 | 1400/1000 | * | Ivey PMI | |

| 05/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 05/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/06/2025 | 1600/1200 | Fed Governor Adriana Kugler | ||

| 05/06/2025 | 1620/1220 | BOC Deputy Kozicki speech | ||

| 06/06/2025 | 2330/0830 | ** | Household spending | |

| 06/06/2025 | 0600/0800 | ** | Trade Balance | |

| 06/06/2025 | 0600/0800 | ** | Industrial Production | |

| 06/06/2025 | 0645/0845 | * | Industrial Production | |

| 06/06/2025 | 0645/0845 | * | Foreign Trade | |

| 06/06/2025 | 0830/1030 | ECB Lagarde Video Message For CIBP Anniv | ||

| 06/06/2025 | 0900/1100 | ** | Retail Sales | |

| 06/06/2025 | 0900/1100 | *** | GDP (final) | |

| 06/06/2025 | 0900/1100 | * | Employment | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1230/0830 | *** | Employment Report | |

| 06/06/2025 | 1230/0830 | *** | Labour Force Survey | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/06/2025 | 1900/1500 | * | Consumer Credit |