MNI US MARKETS ANALYSIS - Fed Cut Expected, QT in Focus

Highlights:

- Fed decision expected to see rates cut a further 25bps, with QT expected to conclude

- GBP weakness extends as pre-Budget nerves weigh further on spot markets

- Trump seals trade deal with South Korea, Xi meeting confirmed for Thursday

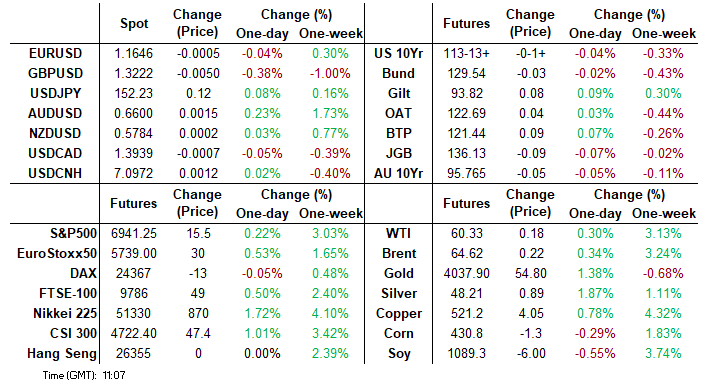

US TSYS: Modestly Lower Pre-Fed, Various Levels Worth Watching

- Treasuries trade modestly lower overnight, more clearly back into yesterday’s range.

- It could be a confluence of factors including pre-FOMC positioning, expectations ahead of tomorrow’s Trump-Xi meeting and supply somewhat underpinning EGB yields.

- Cash yields are ~1bp higher across the curve.

- TYZ5 trades at 113-13+ (-01+) on light cumulative volumes of 210k.

- Support is seen at 113-04 (Oct 27 low) in a move that cleared the 20-day EMA, next opening 112-26 (50-day EMA). Recent weakness appears to be corrective though with a bullish structure still in place, with resistance at 113-24 (post-CPI high) before 114-02 (Oct 17 high).

- Additional levels to watch with today’s FOMC in mind:

- 2Y yield: Having fallen to its lowest level since August 2022 in mid-Oct to 3.374%, some might look to fade off the 50d MA of 3.562% (equating to 104-07) as the 2Y yield recovers (currently 3.500%).

- 10Y yield: Risks look tilted to the downside when looking over the medium term with the 50d MA providing resistance since August. The October low is 3.9342% whilst next support moves back up to circa 3.90% (23.6% retrace of the 2020/2023 range). Currently at 3.987%.

- US 5s/30s at 93.3bp now targets the August low at ~91.92, whilst 2s/10s at 48.9bps is finding some support ahead of 46.96 (Sept low).

- Data: MBA mortgage applications (0700ET), Pending home sales Sep (1000ET)

- Fed: FOMC decision (1400ET), Powell press conference (1430ET)

- FRN issuance: US Tsy $30B 2Y FRN - 91282CPG0 (1130ET)

- Bill issuance: US Tsy $69B 17-wk bills (1130ET)

- Politics: Trump in South Korea, currently at APEC leader’s working dinner, with nothing scheduled for the rest of the day. He meets China’s Xi mid-morning local time tomorrow.

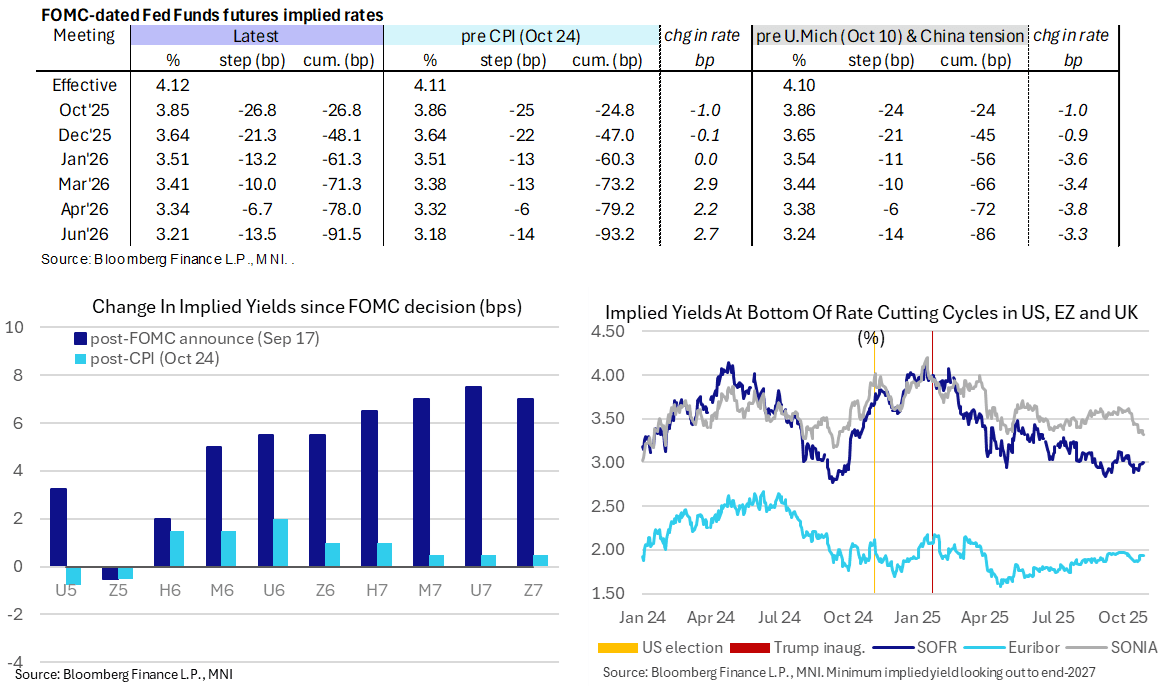

STIR: Fed Rates Marginally More Hawkish Again With FOMC Ahead

- Fed Funds implied rates have extended yesterday’s modest climb in London trading, where, aside from today’s expected 25bp cut, implied rates are 1.5-2.5bp higher on the day out to mid-2026.

- The moves could be a combination of pre-FOMC positioning and headlines on the Trump-Xi meeting going ahead mid-morning tomorrow, later suggested it could last for three hours.

- Cumulative cuts from 4.12% effective (after Monday’s latest push higher): 27bp Oct, 48bp Dec, 61.5bp Jan, 71.5bp Mar, 78bp Apr, 91.5bp Jun.

- SOFR futures are only 0.5-1 tick lower on the day when looking out to end-2027.

- It leaves the terminal implied yield unchanged at 2.995% after yesterday’s close nudged to a fresh high since Oct 9, i.e. prior to the increase in US-China trade tensions on Oct 10.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Oct2025_With_Analysts_2c9e326366.pdf

FED: MNI Fed Preview-October 2025

This update of our October 24 Fed preview includes analyst expectations - starting page 32 - Download Full Report Here

The FOMC is unanimously expected to cut the Fed funds rate by 25bp at the October meeting, per 31 previews seen by MNI.

- Statement: There aren’t many expectations for meaningful changes to the October statement vs September’s, with the characterization of growth seen upgraded somewhat, but few to no changes to the description of inflation / labor market developments. The Statement may add language to acknowledge the limited flow of “official” data, but suggest that trends evident going into the prior meeting remain intact.

- QT: An immediate end to balance sheet runoff is now the consensus expectation for the October meeting. Some analysts expect a December announcement, but acknowledge risks it could happen this week.

BOJ: MNI BoJ Preview-Oct 2025: On Hold, Focus On Dec/Jan Hike Risks

- The BoJ is widely expected to hold rates steady at tomorrow's policy meeting outcome, which is also our bias.

- Focus is likely to rest on hiking risks before year end/early 2026. Whether we see additions to the two dissents from the September policy meeting (who were in favour of a 25bps hike) will be a key focus point, while broader board confidence in achieving the inflation outlook will also be eyed.

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK

NETHERLANDS: MNI Publishes Election Preview

Download Full Report Here

Dutch voters go to the polls on 29 October in a snap general election to elect the 150 members of the lower chamber of the Dutch parliament, the House of Representatives. In this preview, we provide a rundown of the main political parties, an explanation of the electoral system and government formation process, a chart pack of opinion polling and prediction market odds, hypothetical post-election scenarios with assigned probabilities, and sell-side analyst views of the contest.

MNI ECB Preview: Enjoying The Good Place

Download Full Report Here

Executive Summary

- The ECB is fully expected to again leave its three key rates on hold on Thursday, including a 2% deposit rate nicely within the 1.75-2.25% neutral rate range estimated by ECB staff.

- This meeting is likely seen as a stepping stone to December’s updated economic projections, which will include new forecasts for 2028. Any hints here will likely shape market reaction although we see Lagarde opting for a broadly neutral tone to maintain optionality.

BONDS: Supply Underpinning Yields; 10-year Gilt/Bund Close To YTD Low

- Impending sovereign supply is likely underpinning UK and German yields this morning, keeping the 10-year Gilt/Bund spread close to the 2025 low of ~177.5bps.

- The DMO will sell GBP3.75bln of the new 4.125% Mar-33 Gilt at 1000GMT. Meanwhile, Germany will sell E4.5bln of the 10-year 2.60% Aug-35 Bund at 1030GMT.

- The April low continues to contain downside in 10-year Gilts, which are currently little changed at 4.40%.

- Spanish Q3 flash GDP confirmed expectations at 0.6% Q/Q (vs 0.8% prior), but domestic demand signals were solid. UK September consumer credit was in line with expectations.

- The EFSF has sent an RFP for an upcoming transaction, which will likely be held early next week.

- In the Eurozone, focus remains on the ECB decision (Thurs), Eurozone Q3 flash GDP (Thurs) and October flash inflation (Fri). In the UK, spillover from US Treasuries amid today’s FOMC decision will be eyed alongside ongoing budget headline flow.

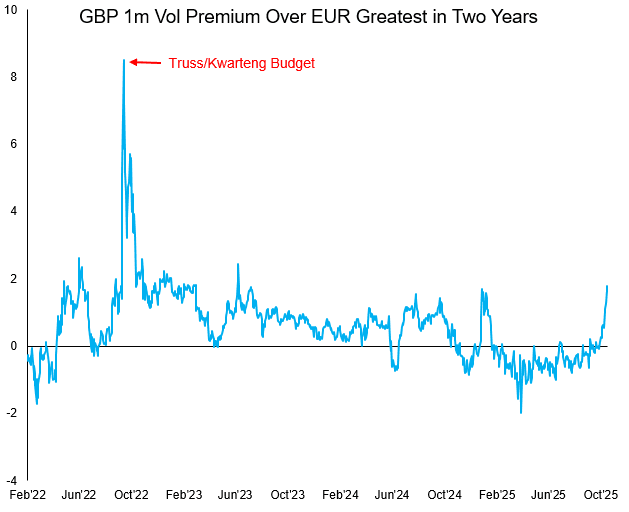

GBP: Vol Markets Signalling Significant GBP Vol Premium Into Budget

The pick-up in spot volatility this week has helped support implied at the margins, with the 1m contract (capturing the UK Autumn Budget on November 26th) rising back above 7 points to provide a decent premium over shorter-dated contracts that expire before the Budget.

While vols above 7 points look unimpressive in isolation, relative to EURUSD the move is extreme. The GBP 1m vol premium over EUR is now near 2 points and the widest since 2023 - signalling markets assigning a greater risk premium to GBP despite the background low vol regime.

We write on the latest expectations for the UK Budget in the Gilt Week Ahead here: https://media.marketnews.com/Gilt_Week_Ahead20251027_14ac41803e.pdf

And summarise the key drivers of GBP spot weakness here:

- Speculation that Reeves will break a manifesto pledge and raise income tax has been bolstered by the FT's reporting on a sizeable productivity estimate cut triggering a broader financing need.

- Higher income taxes would contain consumption, helping smooth the path for faster BoE rate cuts across 2026 (and potentially by the end of 2025).

- Food inflation remains a key driver of inflation expectations (e.g. Just this week: The Times: '‘Shrinkflation’ of supermarket staples rife on British high streets', BBC: 'Businesses face 'rising costs and staffing pressures''), however Tuesday's BRC-NIQ shop price data suggests we have passed the peak in food price gains.

- Food price inflation is particularly important given how well supported it has been this year via both higher employer's NIC contributions as well as incoming packaging taxes, but today's numbers endorse the step lower in ONS food inflation and may suggest inflation expectations will follow.

FOREX: GBPUSD Breaches Bear Trigger, Hitting 2-Month Low Pre-Fed

- Renewed sterling weakness and a slightly stronger dollar has pressured GBPUSD to a fresh 2-month low on Wednesday as pessimism for GBP continues its prevalence amid increasing signs that UK Chancellor Reeves will have to raise income tax at the November 26 budget to fill a widening fiscal hole. The pair has breached the 1.3249 bear trigger and Oct 14 low, confirming a resumption of the downtrend and exposing key support at 1.3142, Aug 1 low.

- Australian CPI beating expectations has materially curbed RBA easing expectations, with the first cut now not fully priced until May next year. While current levels around the 0.6600 handle would lead AUDUSD to extend its winning streak to six consecutive sessions, price action for now has stopped short of the 0.6629 Sep 30 and Oct 1 highs. Clearance of this level would strengthen bullish conditions.

- JPY saw another volatile overnight session, with USDJPY already seeing a near 100 pip range Wednesday. Earlier strength driven by US Tsy Secretary Bessent encouraging the Japanese government to let the BoJ deal with higher inflation was later countered by positive risk sentiment amid further encouraging headlines on US-China trade ahead of tomorrow's Trump-Xi meeting. Drivers for USDJPY remain plentiful with the BoJ meeting due before tomorrow's European open, focus is on hiking risks into year end/early 2026 assuming the consensus view of a hold at the meeting will be realized.

- Bank of Canada and FOMC decisions are the highlight today, with both being expected to result in 25bps cuts. With limited new developments and official data to opine on, Chair Powell’s press conference will be eyed for affirmation that a December cut remains on track, as signalled by the most recent Dot Plot. Focus is also on the balance sheet, with the Fed likely to announce an end to quantitative tightening amid diminishing reserve levels and nascent evidence of funding market pressures.

EQUITIES: Trend Structure Remains Constructive for EStoxx50

- The trend condition in S&P E-Minis remains bullish and price has traded higher this week. The fresh cycle high confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. The 6900.00 handle has been cleared, opening 6953.25 next, a Fibonacci projection. Initial firm support to watch lies at 6748.48, the 20-day EMA.

- The trend structure in Eurostoxx 50 futures is unchanged and remains bullish. Monday’s fresh cycle high reinforces a bull theme and maintains the rising price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. Sights are on 5727.18, a Fibonacci projection. First support lies at 5633.28, the 20-day EMA.

COMMODITIES: Gains for Crude Look Corrective For Now

- Gold traded lower Tuesday as it extends the bear cycle that started Oct 20. Note that the trend is overbought and the deeper retracement is allowing this condition to unwind. Support at the 20-day EMA, at $4037.0, has been breached, signalling scope for a deeper retracement, towards the 50-day EMA, at $3842.8. Key resistance and the bull trigger has been defined at $4381.5, the Oct 20 high. Initial resistance is at $4161.4, the Oct 22 high.

- Recent gains in WTI futures appear corrective for now, however, note that price has traded through the 50-day EMA, at $61.10 The breach of this average signals scope for a stronger recovery. A resistance at $62.34, the Oct 8 high, has also been pierced. A clear break of it would expose key resistance at $65.77, the Sep 26 high. Key support and the bear trigger has been defined at $55.96, the Low Oct 20.

| Date | GMT/Local | Impact | Country | Event |

| 29/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 29/10/2025 | 1100/1200 | ** | PPI | |

| 29/10/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/10/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 29/10/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 29/10/2025 | 1430/1030 | BOC press conference | ||

| 29/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 29/10/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 29/10/2025 | 1800/1400 | *** | FOMC Statement | |

| 30/10/2025 | - | European Central Bank Meeting | ||

| 30/10/2025 | 0030/1130 | ** | Trade price indexes | |

| 30/10/2025 | 0300/1200 | *** | BOJ Policy Rate Announcement | |

| 30/10/2025 | 0630/0730 | *** | GDP (p) | |

| 30/10/2025 | 0630/0730 | ** | Consumer Spending | |

| 30/10/2025 | 0700/0800 | ** | Retail Sales | |

| 30/10/2025 | 0800/0900 | *** | HICP (p) | |

| 30/10/2025 | 0800/0900 | ** | KOF Economic Barometer | |

| 30/10/2025 | 0800/0900 | ** | Economic Tendency Indicator | |

| 30/10/2025 | 0855/0955 | ** | Unemployment | |

| 30/10/2025 | 0900/1000 | *** | GDP (p) | |

| 30/10/2025 | 0900/1000 | *** | GDP (p) | |

| 30/10/2025 | 0900/1000 | *** | Bavaria CPI | |

| 30/10/2025 | 0900/1000 | *** | North Rhine Westphalia CPI | |

| 30/10/2025 | 0900/1000 | *** | Baden Wuerttemberg CPI | |

| 30/10/2025 | 1000/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 30/10/2025 | 1000/1100 | ** | EZ Unemployment | |

| 30/10/2025 | 1000/1100 | *** | EZ GDP 1st (Prelim Flash) | |

| 30/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 30/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 30/10/2025 | 1230/0830 | * | Payroll employment | |

| 30/10/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/10/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/10/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 30/10/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 30/10/2025 | 1315/1415 | *** | ECB Deposit Rate | |

| 30/10/2025 | 1315/1415 | *** | ECB Main Refi Rate | |

| 30/10/2025 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 30/10/2025 | 1345/1445 | ECB Press Conference | ||

| 30/10/2025 | 1355/0955 | Fed's Michelle Bowman | ||

| 30/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 30/10/2025 | 1515/1615 | ECB Lagarde Presents Rate Decision on ECB Podcast | ||

| 30/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 30/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 31/10/2025 | 2330/0830 | ** | Tokyo CPI | |

| 31/10/2025 | 2330/0830 | * | Labor Force Survey | |

| 31/10/2025 | 2350/0850 | * | Retail Sales (p) | |

| 31/10/2025 | 2350/0850 | ** | Industrial Production |